Big-Tech Weekly: Cloud Growth Soared But Investors Yawning? What's Tesla's Next Target?

Big-Tech’s Performance

Macro Headlines This Week: Tariff Escalation? Fed Division; Structural Divergence in US Stocks

Tariff Tug-of-War: Mixed signals emerged on the tariff front. The US-Japan trade framework was finalized, featuring mutual 15% tariffs, $550 billion in Japanese corporate investment in the US, the launch of a US-Japan LNG joint venture in Alaska, and the opening of Japan's agricultural market. External parties raised concerns about the agreement's funding mechanism and return structure, suggesting it appears more like a political gesture than a concrete investment plan. Concurrently, Japan faces domestic political shifts, contributing to the Yen's position as the weakest major non-US currency recently.

Can the Fed Resist Pressure in July? On July 22nd, President Trump called Powell a "clueless person" during a press conference, predicting his departure in eight months (though Powell's term runs until May 2026), despite Powell affirming his intent to serve the full term. Trump then visited the Fed headquarters – the first official presidential visit in nearly two decades – where he criticized building renovations as unnecessarily expensive. He used the occasion to reiterate his calls for rate cuts, drawing significant attention. Scholars expressed concern about Trump pushing for cuts, noting that current inflation and consumer data remain resilient, cautioning against premature easing and stressing that markets cannot "fight the Fed."

Earnings Season Hits Wall Street: AI and tech stocks surged, propelling the Nasdaq to new highs. Market optimism surrounding Q2 corporate earnings broadly supported the market uptrend. Despite positive sentiment, investors remain focused on trade policy, inflation data, and upcoming PMI and durable goods orders releases.

Major Tech Stocks Mostly Rose This Week: As of the July 24th close, past week performance: $Apple(AAPL)$ +1.78%, $Microsoft(MSFT)$ -0.16%, $NVIDIA(NVDA)$ +0.43%, $Amazon.com(AMZN)$ +3.73%, $Alphabet(GOOG)$ $Alphabet(GOOGL)$ +4.68%, $Meta Platforms, Inc.(META)$ +1.91%, $Tesla Motors(TSLA)$ -4.22%。

Big-Tech’s Key Strategy

Will Software Companies Show Their Hand First? (On AI's impact on software firms and why strong earnings aren't translating to stock gains?)

Is AI Disrupting the Search Business?

Early market fears centered on AI models replacing traditional search engines, potentially reducing search ad impressions and click-through rates ("Asking AI instead of Google"). However, Alphabet's (GOOG) Q2 results suggest potential for turning disruption into opportunity. Initiatives integrating GenAI into search (like AI Overviews used by over 2B monthly users and Circle to Search on 300M+ devices) blend AI generation with traditional search paths. Crucially, search ad revenue grew 12% YoY – showing no significant cannibalization by AI; instead, it saw initial benefits from AI-assisted querying and exploration.

The market is increasingly acknowledging that AI may not replace search but redefine the search experience itself. Google's ad products (e.g., Performance Max) now leverage AI for creative generation, improving ROI.

Overall: Alphabet is pivoting towards an "AI-centric ad platform." Perceived AI disruption of search is being transformed into an upgrade path rather than an existential threat, tempering prior market anxieties.

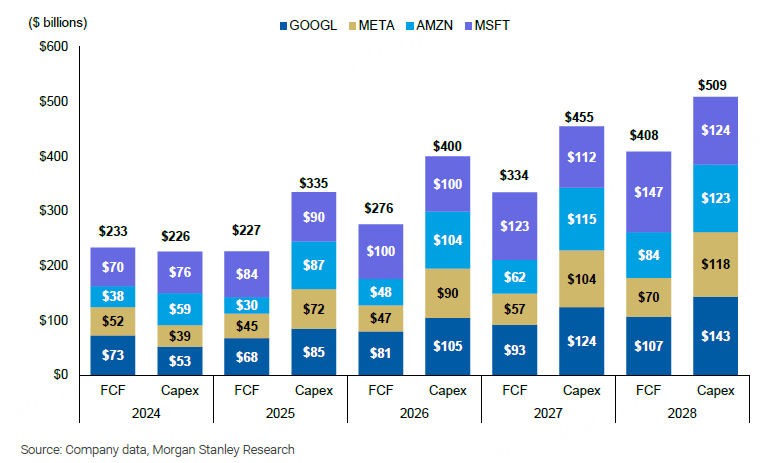

The Capex Surge and Misaligned Expectations

Alphabet dramatically raised its full-year Capex guidance to 85BinitsQ2report,farexceedingpriorforecasts(50-60B). AI servers and datacenters are the primary drivers, especially for Gemini and Google Cloud Platform (GCP).

While high Capex pressures near-term Free Cash Flow (FCF), long-term, if AI ads and GCP scale successfully, Return on Invested Capital (ROIC) could recover by 2026-2028. Morgan Stanley estimates that every 10% increase in AI ad monetization efficiency boosts EBITDA by over 5%.

The OBBBA tax break provides a "cash flow buffer," mitigating short-term investor anxiety regarding massive spending.

Market Reaction: The Capex surge directly benefits AI hardware players (e.g., AVGO reacted more strongly post-earnings than GOOG's +1%).

Cloud Growth Rebounds, Yet Market Apathy?

GCP grew 32% YoY this quarter, outperforming AWS recently. Backlog increased +38% YoY, and large deals (>$1M) doubled. GCP excels as an "AI Infrastructure + Open-Source Services" platform (e.g., model training, API integration), though it still trails Azure in migrating traditional enterprise IT workloads.

Coinciding Data Point: Cloud leader $ServiceNow(NOW)$ reported strong Q2 results (cc cRPO +21.5% YoY, beating guidance by 200bps; Subscription Revenue +22.5% YoY; Operating Margin 29.5%; FCF $535M, 20% above estimates), but signaled slowdown concerns:

Q3 guidance foresees a 100bps cRPO headwind from shorter federal contract cycles.

Full-year subscription revenue guidance raised only modestly (+$25M ex-FX), implying weaker Q4 expectations.

AI Monetization Challenge: While AI product transactions (e.g., Now Assist, Pro Plus) are growing, channel feedback indicates customer skepticism about AI solution maturity and demonstrable ROI, leading some to delay upgrades. Similar "reality checks" on AI hype are emerging at Snowflake, Datadog, and Palantir.

Key Takeaway this Earnings Season: This season favors hardware players (like NVDA, AVGO) whose stocks rallied on AI benefit anticipation, even without results. The market demands clearer monetization pathways from AI software companies. The message for software firms is clear: AI is a core growth engine, but its ability to generate sustainable profits faces skepticism. For cloud software players, key differentiators moving forward are:

Scalability: Driving adoption from pilots to enterprise-wide deployment.

Clear Monetization: Defining pricing, demonstrable ROI, and driving usage volume.

Resilience: Navigating macro uncertainty, particularly government and large enterprise budget pressures.

Valuation: Avoiding "delivery pressure" caused by excessive valuations.

Big Tech Options Strategy

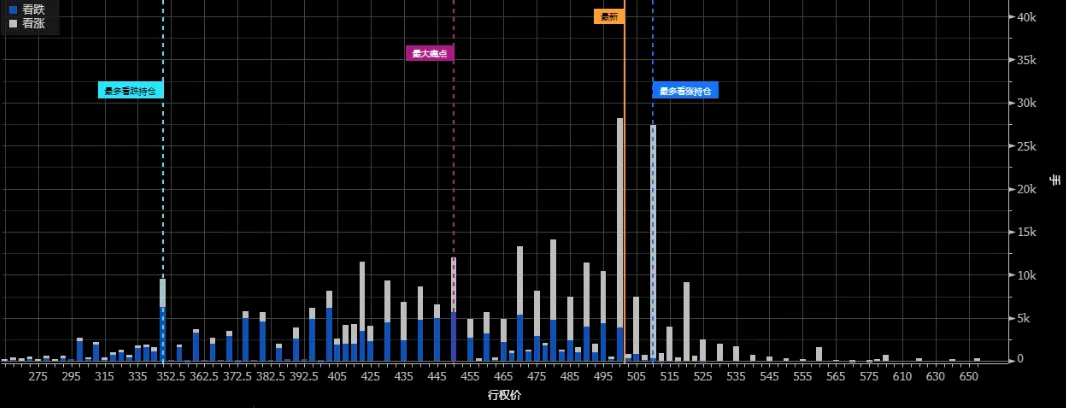

This Week's Focus: TSLA’s boring time comes?

Tesla reported Q2 results on the 24th. Revenue was 22.5B(beat),AutoRevenue16.7B. Auto Gross Margin (ex-regulatory credits & leases) rebounded to 15% (+2.5pp QoQ). However, core auto fundamentals remain under pressure:

US Inflation Reduction Act (IRA) subsidy reduction and Model 2.5 mass production delayed to Q4 are expected to pressure volumes and margins.

Robotaxi/FSD v12 and Optimus progress is on track. FSD v13 update expected late Q4/'25; First Optimus Gen 3 mass production anticipated late '25/'26.

Current $330 share price seems elevated, reflecting lingering concerns about auto operations and geopolitics.

Options Activity: After the earnings report, the company's stock price plummeted by 8%, which is also a retracement of its strong performance in the previous period. Looking at the options, there are a large number of outstanding call option contracts at the 350 and 400 levels. The hedging cover demand will cause resistance at these levels for a long time.

Big-tech Portfolio

The "Magnificent Seven" portfolio ("TANMAMG" – Equal Weighted, rebalanced quarterly) has significantly outperformed the $SPDR S&P 500 ETF Trust(SPY)$ $S&P 500(.SPX)$ since 2015:

Total Return: 2641.29% vs. SPY: 264.90% → Excess Return: 2371.18%

Year-to-date, the portfolio is still positive at +4.14%, though trailing SPY (+7.42%).

Over the past year, the portfolio's Sharpe Ratio has normalized to 0.52 (identical to SPY's 0.52), with an Information Ratio of 0.34.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.

- JimmyHua·2025-07-25Is AI Disrupting the Search Business?- I see the reports of Google, the answer is no, double-digit growth.1Report

- IrmaBurke·2025-07-25Interesting take on Big-Tech1Report

- LisaEffie·2025-07-25This analysis provides great insights1Report