⚠️82x P/S vs 48% Growth: NATO Orders Resurface: Can Global Growth Save Palantir?

$Palantir Technologies Inc.(PLTR)$ Q2 continues the myth of high growth, while also solidifying the concept of "AI+Data Platform", with a healthy operating profile that is underpinned by a sustained rebound in international orders and an increase in the revenue share of the AI product line, as well as near-term growth.

The core factors driving the repricing of its valuation are total contracted orders (TCV), market capacity expansion, AI ramp-up rate and customer retention rate.Of course, its stock price is reacting to very overvalued market sentiment and will be one of the biggest focuses of market attention going forward.

Performance and market feedback

Palantir's Q2 2025 results were strong overall, with key metrics beating expectations:

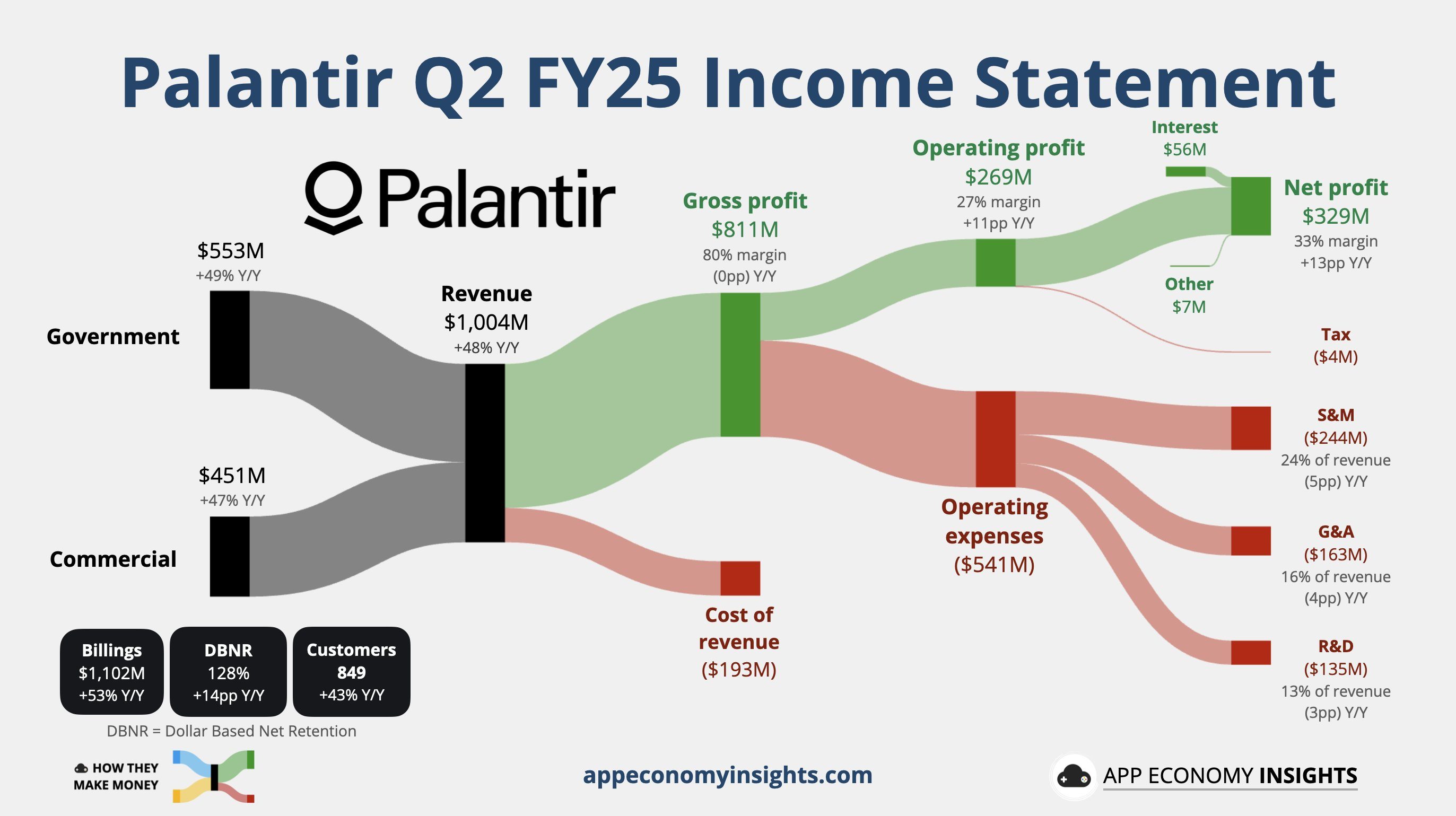

Revenue performance: Q2 revenues of $1.0 billion, up 48% year-over-year and ~13% sequentially from Q1, exceeding market expectations by 6.4% ($940 million vs. actual $1.0 billion).

Earnings performance: Adjusted EPS of $0.16 exceeded estimates of $0.14, while net income of $326.7 million was up 144% year-over-year, demonstrating significant improvement in cost control and operational efficiency.

Regional breakdown: US revenue of $733m, including commercial revenue of $306m, up nearly 100% YoY, and government revenue of $426m, +53% YoY.

Contract value: TCV of $2.27 billion, up 140% YoY, reflecting future revenue potential.

Guidance raised: FY2025 revenue guidance raised to US$4.142-4.150bn, implying 44.5% YoY growth; Q3 guidance of US$1.083-1.087bn, ahead of market expectation of US$983m.

Market reaction

Shares rose 4% after the earnings release, reflecting improved investor sentiment, but high valuation (TTM P/E ~93x) still triggered some caution on guidance is not very high, relative to Q1 due to international revenue miss led to post-earnings plunge -12%, Q2 sentiment stabilized but valuation concerns have not yet disappeared.The core conflict lies in the game of high growth expectations (current PS NTM 60x) and potential slowdown signals.

Key investment points

Strong ToB business drives valuation, international demand inflection point emerging

Commercial revenue exceeded expectations due to the digital transformation of U.S. enterprises and the explosion of AI demand (+92% yoy), confirming the irreplaceability of Palantir's Foundry platform in the complex data analysis market.Q1 international revenue decline has converged (new orders rebounded), mainly due to NATO, the UK Ministry of Defense and other large orders landed (TCV international contribution surged).If the international recovery continues (especially in Europe and Asia-Pacific), it will mitigate the risk of geographic concentration of growth and provide marginal support for valuation.The current order conversion rate (TCV +140% y/y) indicates that there is still beat potential in the next 2-3 quarters, but we need to be wary of geopolitical disruptions to the pace of contract execution.

Government business resilience as cornerstone, AI strategy to deepen moat

Government revenue +43% yoy, YoY fluctuations are normal (uneven execution cycle of defense contracts).Against the backdrop of the Biden administration's increased AI and defense budgets (defense spending +4% yoy in FY2025), Palantir's Gotham platform is deeply tied to government customers with high demand visibility.The key variable is AI product penetration (e.g., AIP solutions) to enhance customer stickiness, with NDR 128% (up YoY) validating the willingness of existing customers to increase purchases.If AI commercialization accelerates (e.g., healthcare, financial industry sign-ups), it could break through the conservatives' 100B definition of its TAM (Gartner Data Tools Market) and move closer to the optimists' 1T software market, triggering valuation upward revisions.

Healthy operating metrics offset guidance concerns, but high valuations have low tolerance for error

Forward-looking metrics were positive across the board:

TCV of $2.27 billion, +140% YoY, reflecting Palantir winning more large, long-term contracts (e.g., 66 deals above $5 million and 42 above $10 million), providing strong support for future revenues.;

Billings: +54% yoy (beat expectations), contract liabilities up $100M YoY, strong cash flow;

Customer growth: net new customers accelerated (dominated by US corporates), government sector & international customers improved YoY. However, management guidance implicitly signals Q4 growth slowdown YoY, which, coupled with decelerating earnings improvement expectations (slower operating leverage release), exposes vulnerability of current 60x PS.

Repricing risk: If Q3 order conversion is not as good as expected or international business is repeated, it may trigger a downward revision of growth rate expectation to below 30%, making it difficult to maintain the high premium.However, the core logic remains unchanged - product competitiveness (AI + low-code deployment) and TAM expansion capability (e.g., new verticals in energy and healthcare) are still long-term supports.

Operational efficiency optimization: Net margins improved significantly from a lower base in the same period last year, and adjusted EPS of $0.16 exceeded expectations, showing a combination of cost control and scale effects.Based on Q1's Rule of 40 score of 83%, Q2 is expected to maintain a high score (48% revenue growth + margin improvement), in line with the software industry's high-growth and high-margin characteristics.

Market expectation revision: from "growth scarcity" to "sustainability verification".

Previously, sellers focused on 1) international revenue volatility (Q2 improvement), 2) valuation bubble (PS NTM 60x vs software sector average 20x); 3) AI commercialization progress (AIP customer number undisclosed but NDR confirms), government contract sustainability. Earnings response: international orders rebound to partially mitigate the risk, but the guidance does not clarify the details of AI revenue contribution, the market is still divided on the "sustainability of high growth".

If TCV maintains triple-digit growth in subsequent quarters or new industry orders (e.g., Indonesia's energy companies mentioned in the report), the consensus may shift from "wait-and-see" to "optimism", while the opposite will strengthen the valuation downward pressure.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.

- Valerie Archibald·08-06Palantir is going to keep going up until there is a disappointing earnings report or until there is a stock split. The logical thing to do then is to keep buying because the price is not going to drop until the above scenario plays out.LikeReport

- Mortimer Arthur·08-06Institutions hate high P/E ratio stocks.. soon we will see 150’s1Report