NetEase Q2 Earnings: Profit Beat Can’t Save Stock From 6% Plunge On Weak Games!

$NetEase(NTES)$ 's Q2 2025 financial report shows steady growth but hides hidden concerns. Revenue was slightly lower than market expectations, mainly due to differences in revenue from its main business, gaming. Net profit was 9.5 billion yuan (up 12.3% year-on-year), exceeding the expected 9.2 billion yuan. $NTES-S(09999)$

The gaming business also had its flaws this quarter. Although several new games performed well on global charts, they failed to deliver on the promise of sustained high revenue growth of 15%+. On the other hand, innovative businesses continued to drag down performance, with Cloud Music revenue declining for two consecutive quarters (down 3.5% year-on-year), raising concerns among users.

Therefore, the market is not excited, falling more than 6% before trading began.

In simple terms, it's a matter of "expectation gap." Due to its strong performance in Q1, NetEase's gaming business set high growth expectations for everyone. Therefore, once it fails to exceed expectations, it becomes an easy target for short-term capital to exploit and suppress.

The company's revenue is highly concentrated in gaming. If the product release schedule for a single quarter is not well-timed, performance fluctuations become evident. This uncertainty must be factored into market pricing.

Key information from the financial report

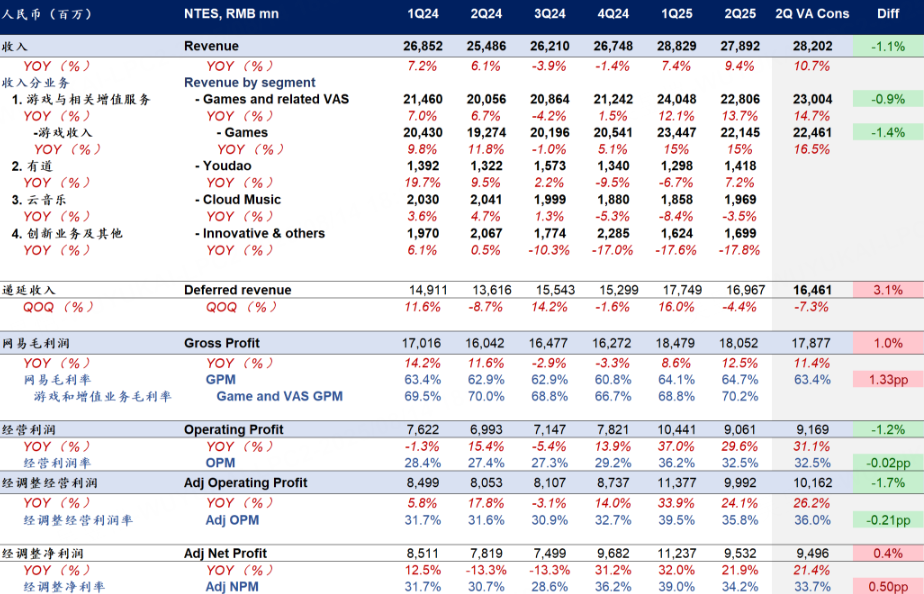

Operating revenue was 27.9 billion yuan (+9.4% YoY), lower than the expected 28.4 billion yuan.

Overseas revenue rose to 35% (30% in the previous quarter). In terms of the realization of its globalization strategy, it still lags behind Tencent Holdings (00700).

Gross margin increased against the trend, while marketing expenses rose, putting pressure on costs. Gross margin was 64.9% (up 1.8 percentage points year-on-year), benefiting from an increase in the proportion of high-margin game revenue. Operating expenses were 9 billion yuan (flat year-on-year, up 12.4% quarter-on-quarter), with sales expenses surging (3.6 billion yuan, up 26% year-on-year), mainly due to new game promotion investments.

Net profit attributable to shareholders of the parent company: RMB 860 million; non-GAAP net profit: RMB 950 million. Basic earnings per share/ADS (company basis): US$0.38 / US$1.88 (ADS).

The company's net cash is 14.21 billion yuan, and it has repurchased approximately 22.1 million ADSs at a total cost of approximately US$2 billion.

Management Expectations for Performance Guidance

Management maintains its target of double-digit growth in game revenue for 2025, emphasizing "original IP incubation" and "global distribution" as core strategies, but has not provided specific numerical guidance.

Cautiously optimistic: "Focus on building a long-term player community" (avoiding short-term revenue fluctuations), CFO emphasizes "prudent investment in new businesses" (implying a reduction in non-core investments). "Game innovation is the engine of growth, and globalization allows us to withstand regional risks." — Implies a defensive stance against weak domestic consumption.

Key Investment Points

Game business breakdown: growth continues, but falls short of expectations

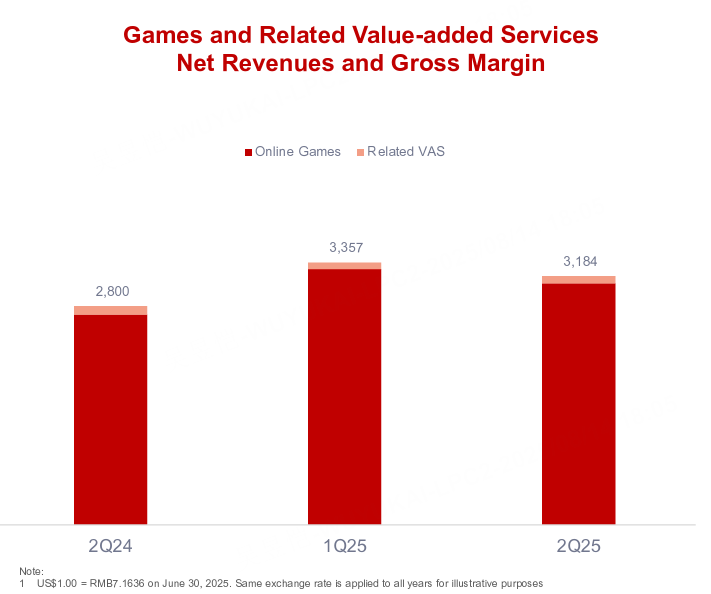

Game and related value-added service revenue: 22.802 billion, up 13.7% year-on-year, down 1.4% quarter-on-quarter, and 0.9% below market expectations (23.004 billion). Online game revenue: 22.146 billion yuan, up 14.6% year-on-year, down 1.4% quarter-on-quarter, also 1.4% below expectations; gross margin (Game & VAS GPM): 72.4%, up 1.33 percentage points year-on-year, indicating an increase in the proportion of high-margin games and further optimization of the cost structure.

Deferred revenue was 16.461 billion, down 7.3% quarter-on-quarter and up 3.1% year-on-year, possibly reflecting that new advance payments in Q2 were lower than in Q1, which may be related to the launch timing of new products and payment patterns. Although new products in Q2 saw a surge in download rankings, payment habits and spending patterns typically lag by 1–2 quarters, meaning that Q3–Q4 may see the true peak in revenue.

Reasons for falling short of expectations may include

Delayed contribution from new products. Although the new products launched in Q2, "All-Star Streetball Party" and "Marvel Secret Magic Frenzy," performed well upon release, the true peak in paid revenue may not be evident until Q3. The overall performance of deferred data is better than revenue.

Console games take longer to monetize. Although Beyond the Boundary topped overseas charts, the monetization pace on console platforms is relatively slow, and their lifecycle differs from that of mobile games.

Seasonal fluctuations in revenue from older games. Games such as "Nishuihan" and "Fantasy Westward Journey" remain strong, but some games have entered a stable phase, and a decline in revenue compared to the previous quarter is a normal seasonal occurrence (especially in the second quarter, which lacks the Spring Festival effect).

Fluctuations in overseas revenue. Although the return of Blizzard games has generated buzz, the commercialization process is still in its early stages and has not yet fully translated into sustained revenue.

In addition, sales and marketing expenses for Q2 totaled 3.799 billion, exceeding market expectations of 3.5 billion, representing a year-on-year increase of 38.5% and rising to 13.7% of revenue (compared to 10.4% in the same period last year). This was mainly due to a significant increase in global promotional spending for new products, particularly overseas user acquisition and brand marketing. This may have left investors with the impression that ROI was low and user acquisition results were below expectations.

Currently, NetEase's mobile game ARPU stands at 163 yuan (up 8% year-on-year), surpassing $TENCENT(00700)$ 142 yuan. However, NetEase's ecosystem lacks the breadth of Tencent's cross-platform strategy. NetEase's revenue remains heavily reliant on a few top-tier products. If new releases underperform or existing games experience a decline in paid user spending, performance volatility could intensify. The current strategy is to accelerate international expansion and diversify across multiple platforms to mitigate reliance on individual products.

Additionally, from a long-term perspective, self-developed game IPs such as Marvel Clash and Yan Yun Shiliu Sheng have proven their development capabilities through global releases, with long-term monetization potential. Meanwhile, the AI applications mentioned in Tencent's latest financial report, such as NPC interaction and level generation, may also offer potential for cost reduction and efficiency improvements.

Non-gaming businesses remain a weak point.

NetEase's diversification efforts are still underway, but the pace is not particularly fast. 1. Cloud Music -3.5%: The online music segment is performing well, but social entertainment revenue is lagging behind, relying heavily on copyright purchases, with user churn reflecting a weak content ecosystem; 2. E-commerce: Yanxuan is facing pressure from Pinduoduo and Douyin, necessitating a shift toward differentiated product categories (such as health-related consumption); 3. Youdao +7.2%: Online education and marketing businesses remain stable, but hardware continues to underperform.

The decline is due to valuation implying high growth expectations, with a focus on expectation gaps.

Net operating cash flow for Q2 was 10.9 billion, with net cash on hand of 142.1 billion RMB. Quarterly dividends and large-scale buybacks were conducted simultaneously:

Repurchased 22.1 million ADSs at a total cost of approximately US$2 billion.

Quarterly dividend of $0.114 per share ($0.57 per ADS).

Compared with the current share price, a shareholder return rate of 4% is a plus for medium- to long-term investors.

The current valuation is 15 times forward PE (vs. Tencent's 18 times), implying a 15% growth expectation for 2026.

There may be some disagreement regarding market pricing. If game revenue rebounds in Q3 and Q4, it may drive upward revisions to valuations. However, if new game revenue falls short of expectations (e.g., Blood Tears), valuations may be adjusted downward.

Core Tracking Indicators:

Games: Q3 global revenue for "Sixteen Sounds of Yan Yun" and its share of the Steam platform; Q4 Blizzard returns to China, and "World of Warcraft" exclusive servers will go live, potentially creating a closed loop for the PC gaming ecosystem.

Technology: AI-driven user engagement rate increase (current +10%)

Positive: TGA award wins or sparks new IP; NetEase's self-developed AI engine opens source;

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.