Big-Tech Weekly | Dojo Ditched, FSD Turbocharged! Tesla’s AI Pivot

Big-Tech’s Performance

Macro Headlines This Week: High Rate Cut Expectations, but Uncertainty Emerges

Data Divergence Increases Policy Difficulty. July CPI (+2.9% YoY) and Core CPI (+3.2% YoY) both undershot expectations, strengthening market bets on a Fed rate cut within the year, pushing the probability of a September cut above 80%. However, a subsequent surge in PPI reignited inflation concerns, suggesting tariffs are shifting from a short-term to a structural impact. The Fed must now balance growth and inflation risks. $Cboe Volatility Index(VIX)$

Fed Independence Remains in Focus. Fed officials expressed divergent views: Bowman cited weak jobs data as supporting three more cuts this year; Schmid advocated holding rates at 4.25%–4.50%; Goolsbee emphasized the Fed is assessing whether tariff-induced inflation is transitory or structural. The Fed faces dual challenges from murky data and potential political intervention. While Bessent pushed for rate cuts, it didn't fully undermine policy independence. $US30Y(US30Y.BOND)$ $US10Y(US10Y.BOND)$ $iShares 20+ Year Treasury Bond ETF(TLT)$

Earnings Week Highlights & Trends for Tech. The $S&P 500(.SPX)$ and $NASDAQ(.IXIC)$ posted similar gains. Previously weak small-caps $iShares Russell 2000 ETF(IWM)$ rebounded significantly this week (due to interest rate sensitivity), but pulled back again after Thursday's PPI data. Tech giants held firm, with the Nasdaq Golden Dragon China Index ( $KraneShares CSI China Internet ETF(KWEB)$ Index) hovering near highs. AI-driven tech earnings supported the market upside, but high valuations imply risk: a cooling AI fervor could trigger a significant market correction.

Mega-Cap Tech stocks showed steady upward movement this week. As of the Aug 14th close:

$Apple(AAPL)$ : +5.79%; $Microsoft(MSFT)$ : +0.31%; $NVIDIA(NVDA)$ : +0.69%; $Amazon.com(AMZN)$ : +3.52%; $Alphabet(GOOG)$ $Alphabet(GOOGL)$ : +3.27%; $Meta Platforms, Inc.(META)$ : +2.66%; $Tesla Motors(TSLA)$ : +4.13%

Big-Tech’s Key Strategy

Tesla: "Weak Cars, Strong AI" Narrative Cools? Market Bets on FSD's 6-Month Countdown!

The "Weak Cars / Strong AI & Robotics Expectations" narrative was forced to quieten in the weeks post-earnings: Real-world pressure on North American EV demand and pricing persists. However, a shift in AI resources away from self-developed computing power (Dojo) towards more focused FSD product iteration has shifted market focus from "visionary premium" to "delivery validation." In other words, capital now prefers paying for visible FSD subscription and energy storage cash flows over Optimus/full autonomy timelines, maintaining a "show me the proof" cautious optimism.

Core auto business volume and pricing remain pressured; "Conservatism on Cash Flow" is the theme.

Post-earnings, sell-side analysts lowered Tesla's FY25/FY26 delivery, revenue, and margin assumptions, warning of "greater challenges" in upcoming quarters, with FCF closer to breakeven. This aligns with the secondary market's "low-growth / low-premium" pricing approach.

While cost improvements (manufacturing efficiency, platform reuse) continue, high price sensitivity and lack of significant industry capacity rationalization have reduced market willingness to assign a high multiple to the auto business alone. Reduced contribution from carbon credits and other one-time items also hinders margin stability.

Post-earnings, capital focus shifted to preserving cash, controlling capital intensity, and optimizing product mix, rather than volume-at-all-cost tactics. This aligns with concerns over cash flow and earnings quality.

Dojo Wind Shift: Resource Reallocation from "Self-Built Compute" to "FSD Deployment". Recent reports indicate Tesla has dissolved/reorganized the Dojo supercomputing team, reassigning engineers to FSD and AI5 development. The market interprets this as reducing near-term uncertainty and capex on self-built training infrastructure, focusing resources on FSD productization and in-car experience closer to monetization.

From an investor perspective, valuation impact is two-sided:

Positive: Faster FSD version cycles, potentially higher subscription adoption/ASP could transition "AI premium" from story to visible recurring revenue.

Negative: Weakening of the self-built compute "moat" narrative increases focus on reliance on third-party GPU supply chains and training cost flexibility, warranting a long-term discount to the "AI platform company" premium.

FSD commercialization will further shift focus from "narrative premium" to "data & subscription metrics":

Subscription vs. one-time purchase structure (monthly fee penetration & retention rates).

City availability and functional boundaries (NoA/city Navigate on Autopilot, handling complex scenarios like rain, night, construction zones).

Safety and regulatory milestones (accident rates, regulatory communication progress) to support higher SaaS-like multiples.

The core disagreement between Tesla bulls and bears centers on FSD delivery speed. Bulls bet subscription adoption and widespread map-free city deployment can deliver visible KPIs within 6-12 months. Bears believe regulatory hurdles and solving long-tail edge cases will prolong the timeline.

Other Relative Bright Spot: Energy Storage's Role as a Cash Flow "Ballast" Amplifies. Contrasting sharply with autos, the growth and margin improvement in Tesla's Energy Storage business (Megapack etc.) is viewed by the market as a more "verifiable" source of cash flow, fulfilling a valuation "stabilizer" function.

Other Risk Factor: Elon Musk-Related Headlines. A court ruled Musk must face OpenAI's allegations of a "long-running harassment campaign" (procedural development), coupled with his public comments on potential Apple antitrust lawsuits, creates headline and governance noise. The secondary market is responding with a higher "execution risk discount," though direct near-term impact on operating cash flow appears limited.

Big Tech Options Strategy

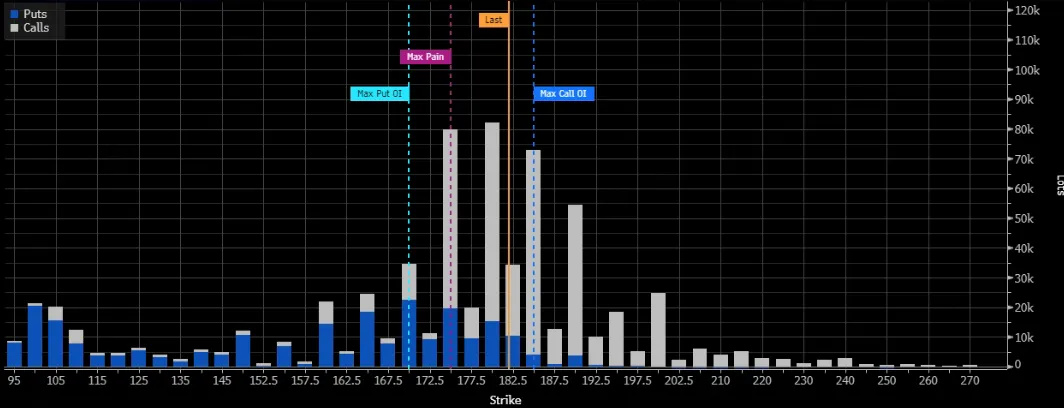

This Week We're Watching: NVDA Likely to Stay Range-Bound Ahead of Earnings

Nvidia already provided Q2 (FY2026) revenue guidance of ~45B(±28B hit from the China H20 export ban; this is essentially the current Street consensus. The real market divergence isn't about Q2 itself, but the pace and "smoothness" of the H2 Blackwell (GB200/NVL72) scale ramp: confirmed delays/production bottlenecks would lead to downgrades in full-year growth and margin expectations; conversely, confirmation of "on-time + acceleration" solidifies the "overweight AI infrastructure" thesis.

The stock has traded in a range over the past two weeks, with institutions continuing to "buy the dips." Options implied volatility has risen, with calls holding a slight edge. There's not much large block trading at the current level. Heavy OI Call concentration sits at the 185strikeforlateJulyexpiry.Abouncewithinthe175-185rangeislikelynextweek,consistentwithnotabletradeslikethe175 Bull PUT and $185+ Bear CALL spreads.

(See chart below for NVDANVDA OI visualization)

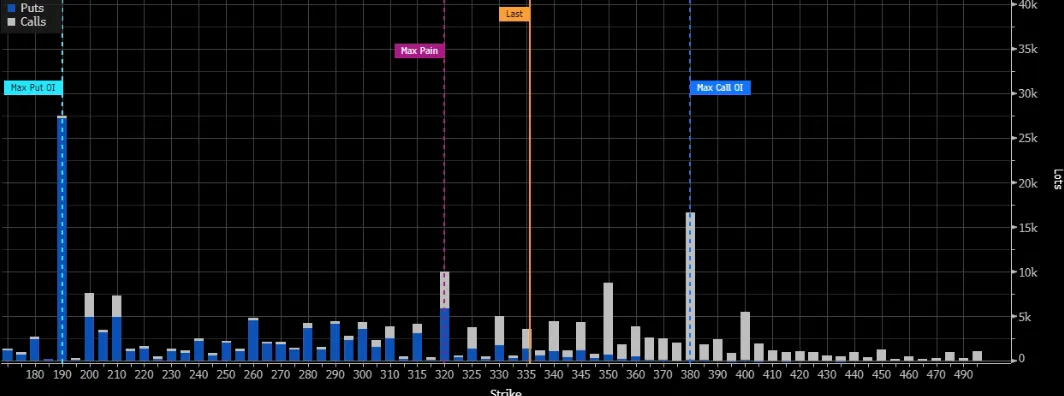

Looking at the TSLA OI structure, the $380 level stands out as a key barrier.

(See chart below for TSLA OI visualization - text description insufficient)

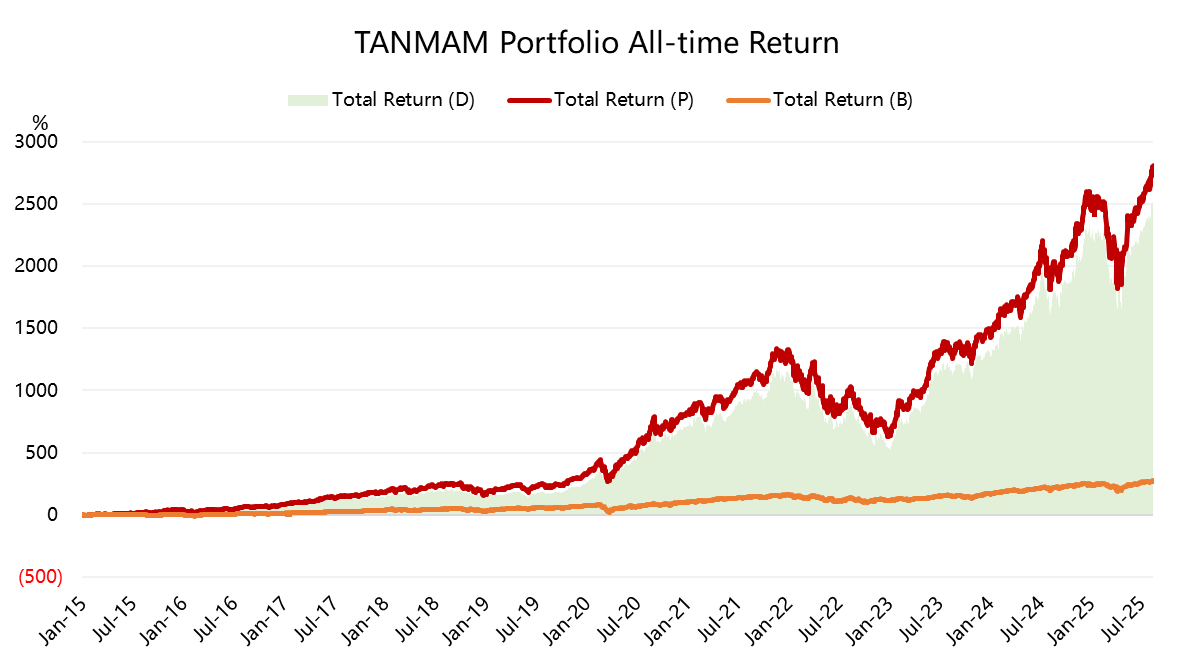

Big-tech Portfolio

A portfolio tracking the "Magnificent Seven" ("TANMAMG" for TSLA, AMZN, NVDA, MSFT, AAPL, META, GOOG), equally weighted and rebalanced quarterly, has dramatically outperformed the $SPDR S&P 500 ETF Trust(SPY)$ since 2015. Backtested results show a staggering 2,804.25% total return for the "TANMAMG" portfolio, compared to 276.25% for SPY – delivering an excess return of 2,528.00% and reaching new highs.

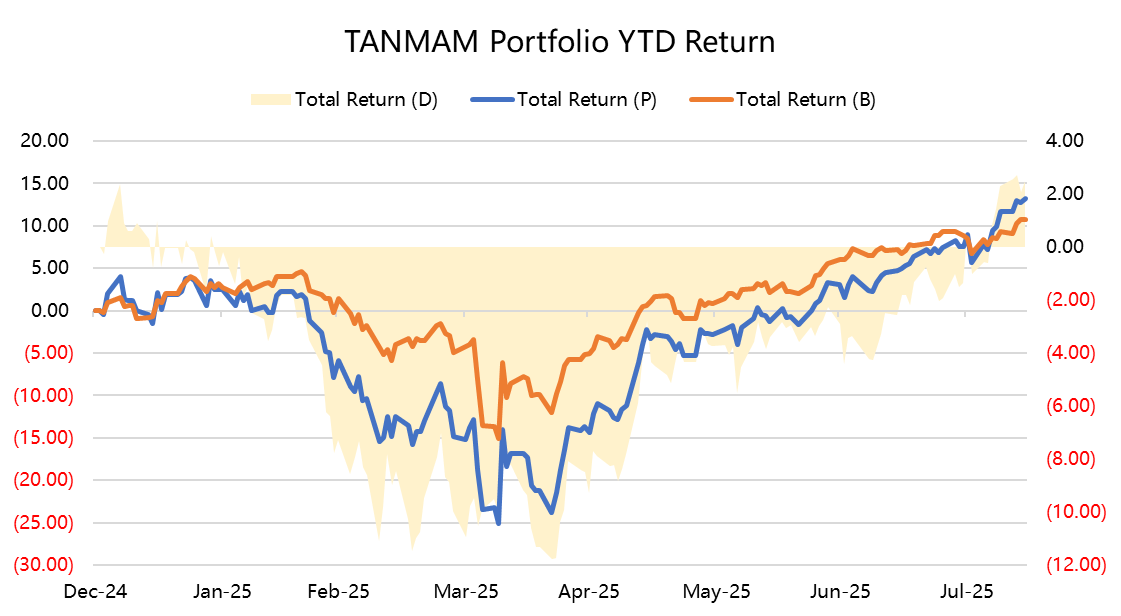

Year-to-date, mega-cap tech has generated strong positive returns of 13.20%, outperforming SPY's 10.70% return.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.