Tech Weekly Review: No "Slacking Off" in Summer, Triple Games Hidden in the Covert Battle of TMT

Behind the index's new high: High beta "plunge" exposes market "false prosperity"

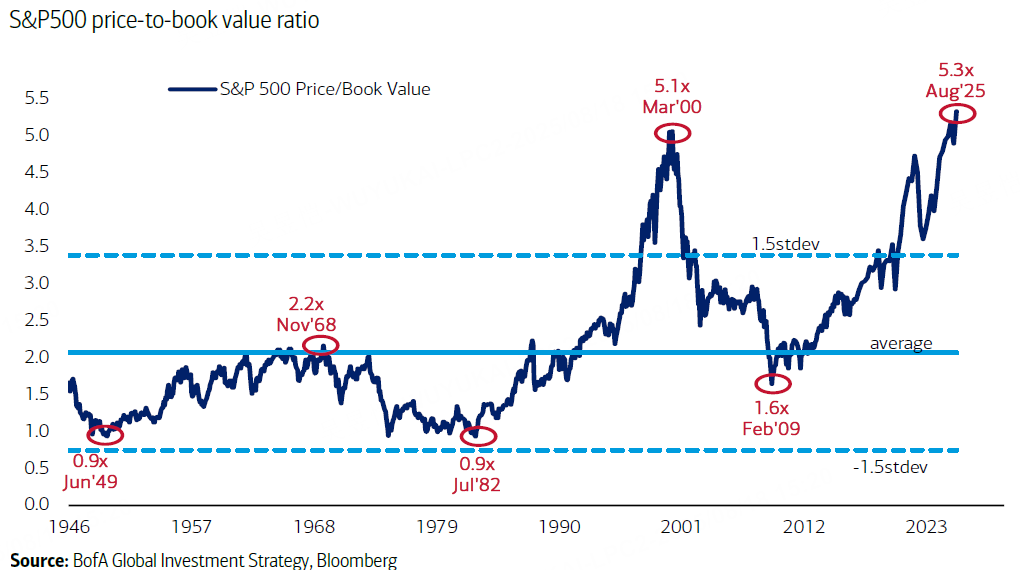

$S&P 500 (.SPX)$ hit a record high, with forward P/E ratios also approaching record highs, but $Nasdaq (.IXIC)$ underperformed for three consecutive weeks, with high-beta portfolios plummeting 7% over five days (the worst since March), while the healthcare sector bucked the trend with a 4% gain (the best since October 2022) — such contrasts further highlight the market's "surface prosperity."

Financial report divergence: From "easy wins" to "battlefield"

$Amazon (AMZN)$ Online sales, $Apple (AAPL)$ iPhone growth exceeds expectations (due to government subsidies), $Meta Platforms, Inc. (META)$ Advertising revenue rebounds— —but Adyen is being held back by Asia-Pacific retail, $Applied Materials (AMAT)$ growth slows due to declining traffic in China, consumer companies collectively "tone down" their rhetoric, algorithmic changes reveal the AI "reaper"… Earnings reports are no longer a sure bet, but rather an amplifier of divergence.

$Palo Alto Networks (PANW)$ , $Workday (WDAY)$ and other "non-quarterly earnings reports" are piling up, and the market's tolerance for "growth flaws" is decreasing (e.g., $Home Depot (HD)$ / $Lowe's (LOW)$ would be snapped up even with a slight decline, but $Adyen N.V. (ADYYF)$'s weakness directly triggered a sell-off). Conclusion: The premium for "beating expectations" is narrowing, and the distinction between genuine growth and fabricated narratives will soon become clear.

AI goes from "bull run" to "breathing space" as the market searches for the next "anchor point"

NVIDIA's weekly correction has reignited talk of an "AI bubble," but the essence of the issue is short-term overvaluation + summer cooling-off period, rather than a collapse in logic. In recent surveys, institutional discussions have shifted from "Can AI succeed?" to more detailed debates:

How to calculate the "incremental value" of large models? (LLM debate)

How will Sino-US technological competition affect supply chains? (H20 controversy)

Should the 2026 profit forecast be realized ahead of schedule? (NVIDIA's 2026 expense guide becomes the focus)

The money hasn't left the market; it's just waiting for a "new story"—such as whether the Jackson Hole meeting will pour more cold water on AI computing power, or whether Nvidia's financial report will paint a rosier picture for 2026.

The "confidence crisis" in the software sector: recovery depends on "cooling down + stabilization"

Recently, when discussing software with institutions, the most common sentiment expressed was "confusion": despite strong financial reports ( $Dynatrace Holdings LLC(DT)$ , $Datadog(DDOG)$ ), while those with poor financial reports (such as $Monday.com Ltd.(MNDY)$ and $Twilio Inc(TWLO)$ ) don't drop much either, $Salesforce(CRM)$ with a 25x P/E ratio is still called "expensive"… On the surface, it's a valuation dispute, but in reality, it's a double anxiety of "AI stealing the spotlight + unclear recovery in the enterprise sector."

To reverse the trend, at least two signals must be observed: ① The AI boom cools down, and capital flows back into software; ② Enterprises showing "marginal improvement" (e.g., AI monetization data from $Salesforce (CRM)$ and the growth rate of INTU's cloud revenue). Before that, the software sector resembles a "bottom-forming market." Those who can endure will profit from time, while those who cannot will only follow AI fluctuations.

Key events this week: Powell sets the tone + earnings reports mark the end of the quarter

Jackson Hole Meeting: The market is pricing in an 85% probability of a 25bp rate hike in September. Powell's "hawkish-dovish" stance directly affects the valuation of tech stocks (the logic that high interest rates kill the valuation of growth stocks still holds).

Intense barrage of financial reports:

Consumer end: $Walmart (WMT)$ People are bearish on consumption, but its performance remains strong (refer to McDonald's trend—when it drops, there are buyers).

Technology sector: $Intuitive Surgical (INTU)$ and $Workday (WDAY)$ will release non-quarterly financial reports, testing the strength of growth stocks during the off-season.

Hardware: $Google (GOOG)$ Pixel launch event, gaming expo: Can hardware innovation steal the spotlight from AI?

Strategically, don't chase high volatility; instead, look for targets with both defensive and growth attributes.

In today's market, "high beta = high risk," and "strong themes + stable valuations" are the safe havens: for example, $Netflix (NFLX)$ (content + AI cost reduction), $Roblox Corporation (RBLX)$ (metaverse + user stickiness), which have both long-term growth logic and the ability to withstand volatility.

The summer off-season is never a time to relax, but rather a litmus test for financial battles. After all, stocks that survive the shakeout will have greater potential for growth in the fall.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.