Big-Tech Weekly | NVDA Preview:What's Buyside Estimate?

Big-Tech’s Performance

Macro Headlines This Week: Market in divergence while techs in correction

The three major US stock indexes experienced a sustained decline this week, with the $S&P 500(.SPX)$ recording a "five-day losing streak." technology stocks were broadly under pressure, and the consumer sector was significantly dragged down by $Wal-Mart(WMT)$ (the first time in three years that profits fell short of expectations, reflecting the pressure of tariffs pushing up costs), while

U.S. Treasury yields rose across the board. Market concerns over the Fed's hawkish stance intensified, with the bond market reacting based on the logic of "stagflation trading" — conflicting economic data (strong manufacturing PMI vs. rising unemployment) coupled with tariff inflation pressures forced investors to shift to defensive assets ahead of Powell's speech. Meanwhile, Federal Reserve officials have been sending out hawkish signals in rapid succession, with the Fed's independence facing unprecedented challenges. Trump is attempting to influence the interest rate cut agenda through personnel interventions (seeking to appoint his confidant Milan to the Board of Governors), but the unexpected rise in the Producer Price Index (PPI) and the stickiness of service sector inflation may force Powell to maintain a "hawkish wait-and-see stance" in his Jackson Hole speech, with the probability of a rate cut in September dropping from 95% to 75%. The US and EU have reached a trade framework agreement: the EU will eliminate all tariffs on US industrial goods, while the US will impose a 15% tariff cap on EU automobiles, chips, and other goods. $US10Y(US10Y.BOND)$ $iShares 20+ Year Treasury Bond ETF(TLT)$

The tech sector saw a correction trend this week. $Tesla Motors(TSLA)$ is under investigation by the NHTSA for delayed reporting of FSD accidents; $Meta Platforms, Inc.(META)$ has been accused of circumventing $Apple(AAPL)$ privacy restrictions to boost ad revenue. MIT report highlights that 99.5% of AI pilot projects fail to deliver significant financial returns, with only 5% achieving rapid revenue growth. The report found that over 50% of AI budgets are allocated to sales and marketing, yet the highest returns come from backend automation.

The tech sector saw a broad pullback this week. As of the close on August 22, over the past week, $Apple (AAPL)$ fell by 3.91%, $Microsoft(MSFT)$ -3.51%, $NVIDIA(NVDA)$ -2.65%, $Amazon.com(AMZN)$ -2.4%, $Alphabet(GOOG)$ $Alphabet(GOOGL)$ -0.87%, $Meta Platforms, Inc.(META)$ -4.99%, $Tesla Motors(TSLA)$ -4.66%.

Big-Tech’s Key Strategy

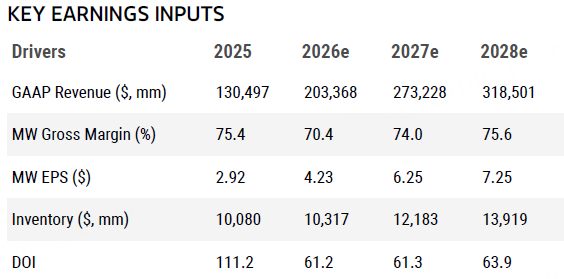

NVDA Q2 Preveiw: Can it exceed buy sides' expectations?

Supply is improving, demand remains strong, and Blackwell's increased production will drive growth by 2026.

On the optimistic side: Hyperscalers and secondary cloud companies (such as CoreWeave) are significantly accelerating the expansion of their DL/inference production capacity. Public statements by management and cloud providers (such as "insatiable," "remarkable," and "massive") are being used as empirical evidence, and cloud providers' CapEx expectations are rising significantly.

In the April quarter, the company disclosed separate revenue figures for H20, Blackwell, and Hopper (e.g., 4.6 billion for H20; approximately 23 billion for Blackwell; approximately 6 billion for Hopper). Currently, the Hopper production line has been suspended, and short-term revenue will be affected by the mix (the mix of B200/B300 and whole machine racks will affect ASP and gross profit).

Key points of the conference call:

October quarter revenue guidance (whether management is conservative about ex-China) — most likely to surprise/impact EPS the most

Blackwell unit shipments and system (rack) vs. B200/B300 mix (impacting ASP and gross margin).

Gross margin guidance and product mix (an increase in the proportion of complete machines should drive an upward revision of gross margin).

The latest status of market licensing/market access in China and the company's shipping arrangements in China.

Customer CapEx signals (which hyperscalers are buying and which are waiting), as well as the company's description of its customer structure (top 4 vs. tier-2 cloud service companies).

Inventory and delivery rhythm (including changes in ODM/test factory lead time)

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.

- dimpy·2025-08-22Incredible insights, truly appreciate it! [Wow]LikeReport

- zingzy·2025-08-22Sounds like tech stocks are in for a rough ride.LikeReport

- Brando741319·2025-08-24Good1Report

- YueShan·2025-08-24Good ⭐⭐⭐LikeReport