Dell Ups AI Target to $20B: Betting Big on GPUs

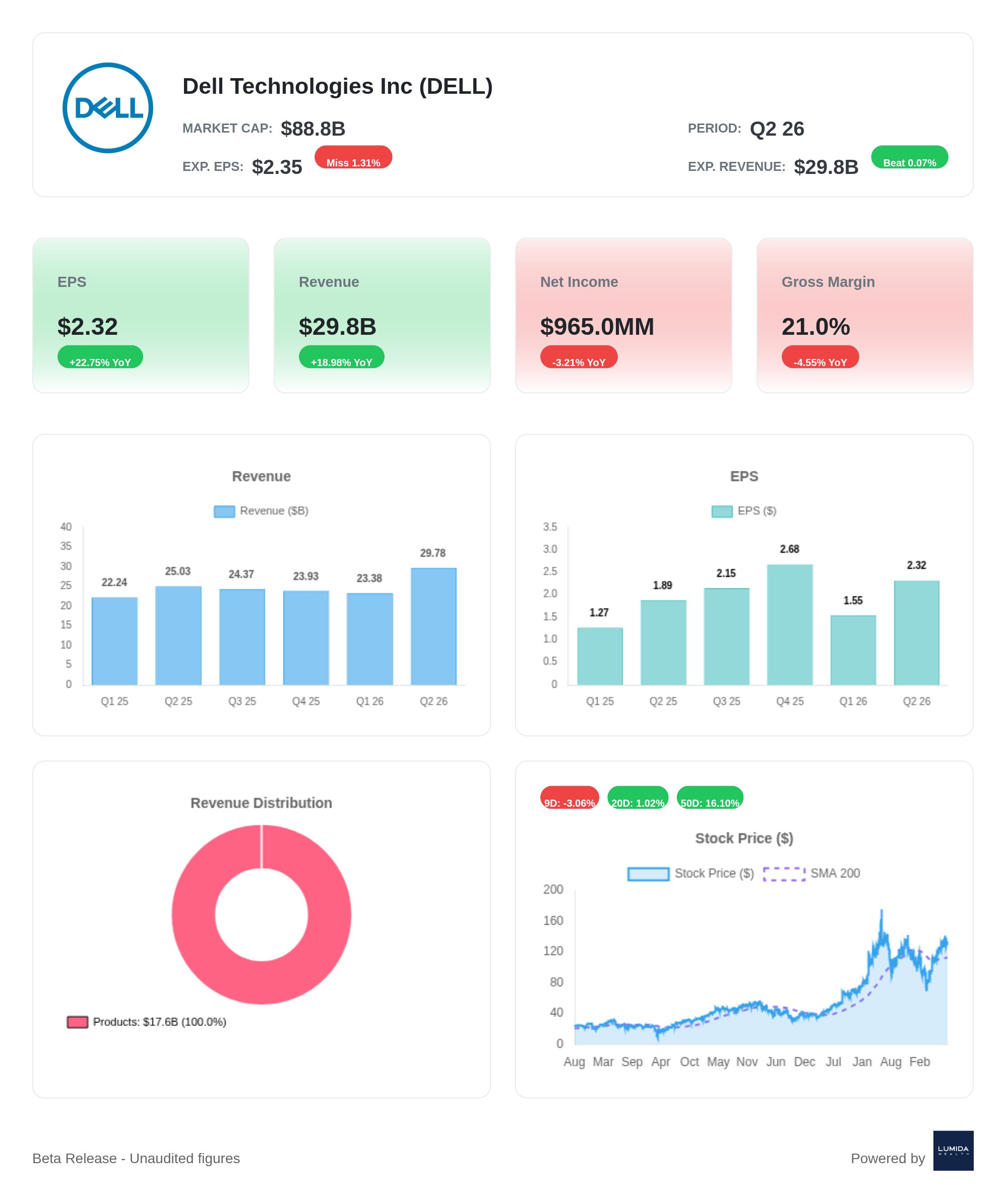

$Dell Technologies Inc.(DELL)$ delivered record revenue for its second fiscal quarter of 2026 (ending July 2025), with total revenue reaching $29.8 billion—a 19% year-over-year increase that exceeded market expectations. However, underlying concerns lurk behind the impressive figures: gross margin declined to 18.3% (down 2.9 percentage points year-over-year), traditional business growth remained sluggish, and explosive AI server deliveries squeezed profit margins. Despite exceeding expectations in AI order fulfillment, market skepticism persists regarding the company's sustained growth momentum and profitability quality.

Performance: AI servers drive revenue growth, but structural challenges become more apparent.

1. Explosive growth in AI infrastructure puts pressure on profit margins

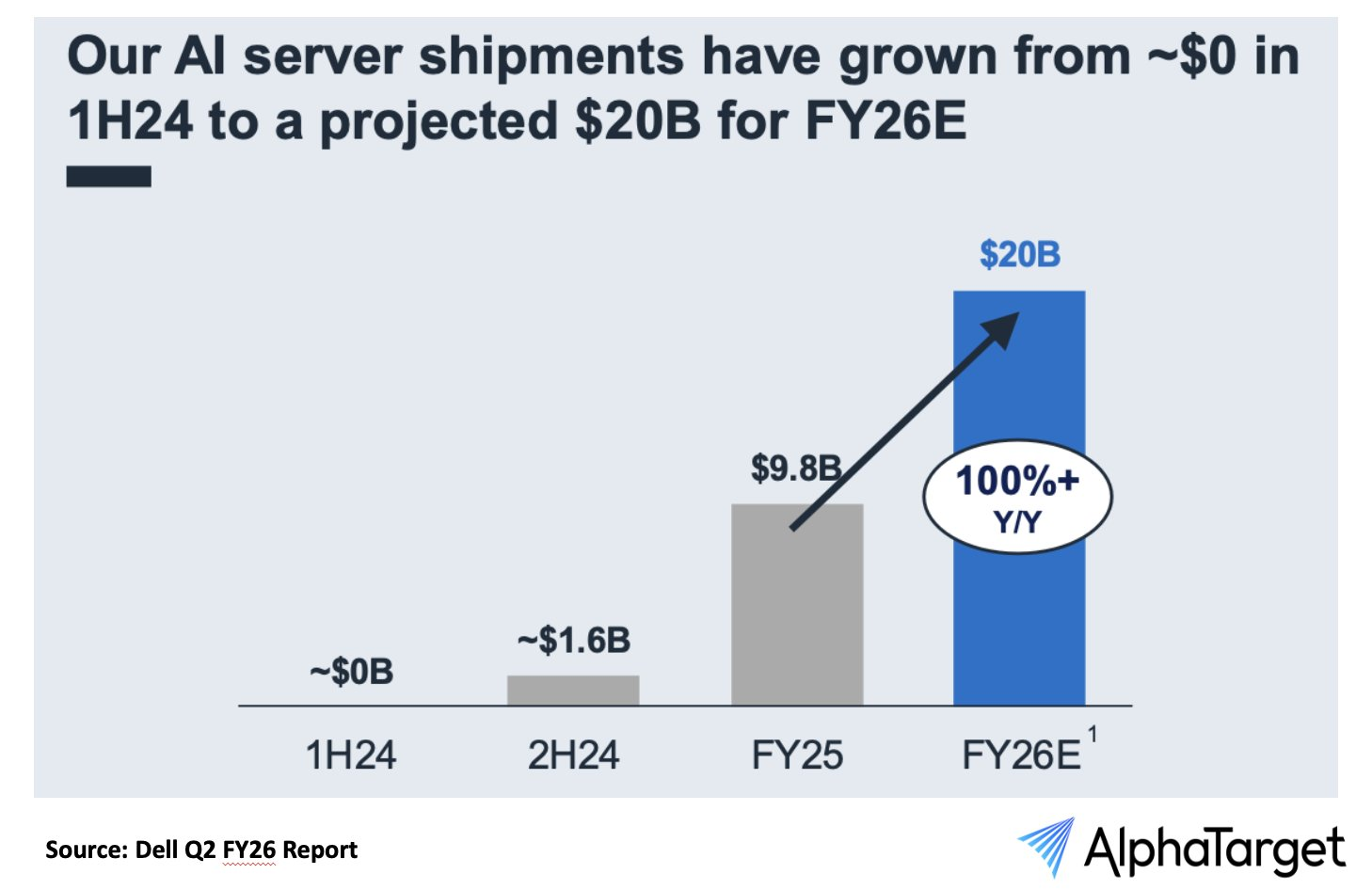

The Infrastructure Solutions Group (ISG) emerged as the standout performer this quarter, with revenue surging 44% year-over-year to $16.8 billion. Within this segment, the server and networking business contributed $12.9 billion, soaring 69% year-over-year. This growth primarily stemmed from concentrated deliveries of AI-optimized servers—AI solution shipments reached $10 billion in the first half of the fiscal year, surpassing the full-year total for FY2025. However, the increased proportion of low-margin AI hardware, coupled with a 3% year-over-year decline in storage revenue to $3.9 billion, caused ISG's operating margin to drop to 8.8%, a 2.2 percentage point decrease year-over-year. This reflects the company's balancing act between scaling operations and maintaining profitability.

The Client Solutions Group (CSG) reported revenue of $12.5 billion, marking a modest 1% year-over-year increase that fell short of market expectations. By segment, commercial PC revenue reached $10.8 billion (up 2%), while consumer PC revenue stood at $1.7 billion (down 7%), highlighting weak global PC demand. Despite the company emphasizing the long-term potential of AI PCs, their current penetration rate remains below 5%. This makes it challenging to reverse the near-zero growth of traditional business, which accounts for over 80% of revenue, in the short term.

3. Cash Flow Improvement and Profit Quality Differentiation

Operating cash flow for the quarter reached $2.5 billion, surging 90% year-over-year, primarily driven by accelerated inventory turnover and advance payments on orders. However, excluding the one-time impact of AI-related orders, underlying profitability actually weakened—the GAAP net profit margin stood at just 3.9%. Although this represents a marginal 0.4 percentage point increase year-over-year, it remains significantly below the profitability levels of non-AI businesses.

Growth Drivers: Can AI-Driven Orders Sustain Momentum?

1. Short-term order fluctuations and upward revisions to long-term guidance

Management disclosed that AI server backlog orders reached $14.4 billion this quarter, prompting the company to raise its fiscal 2026 AI server shipment target to $20 billion (previously $15 billion). However, the next quarter's guidance reflects caution: Q3 revenue is projected at $26.5 billion to $27.5 billion (a 9% sequential decline at the midpoint), primarily due to the AI backlog having been reduced to $11.7 billion. AI revenue is expected to fall to $6 billion in Q3. This fluctuation has sparked market concerns about the sustainability of growth.

2. Lagging Ecological Development and Differentiation Challenges

Dell's AI strategy relies excessively on its hardware manufacturing model, lacking the cloud-plus-software ecosystem support seen in companies like Microsoft or Amazon. Despite partnering with Nvidia to launch generative AI solutions, software/subscription revenue is not disclosed separately, and service revenue declined 4% year-over-year, indicating slow progress in its platform transformation. Furthermore, AI server gross margins remain in the low to mid single digits (compared to around 20% for traditional servers), and the company is highly dependent on Nvidia chip supply. This lack of differentiation intensifies profitability pressures.

Challenges and Outlook: Balancing Short-Term Performance with Long-Term Transformation

Valuation Discrepancies and Market Expectations

Dell's current market capitalization corresponds to a 13x P/E ratio (based on projected FY2026 net income of $6.7 billion), lower than $SUPER MICRO COMPUTER INC(SMCI)$ (25x) but higher than $HP Inc(HPQ)$ (8x). The market assigns a premium to AI servers, but if AI growth slows to 20% in 2027 (from an estimated +100% in 2026), the valuation's margin of safety will face scrutiny.

The key tracking variables include the following:

Order Stability: Whether Q3 backlog can remain above $10 billion will determine near-term growth expectations;

Gross Margin Recovery: Can the scale effect of AI servers drive gross margin back to 20%?

Storage Business Rebounds: If corporate IT spending recovery drives storage revenue back into positive territory (current quarter down 3% year-on-year), it will ease growth concerns.

AI PC Penetration Rate: If the AI replacement wave materializes in the commercial PC sector during the second half of 2025, it could emerge as a new growth driver.

Dell's quarterly earnings report exhibits classic "pulse-like growth" characteristics: concentrated AI orders drove record revenue, yet masked underlying weaknesses in core operations and an unproven profit model. Moving forward, the company must guard against the risk of intensifying competition in the hardware manufacturing segment. It should accelerate its transformation into a solutions provider by integrating VMware $Broadcom(AVGO)$ technologies and expanding subscription services. Should Q3 stabilize AI order volumes and improve gross margins, valuation may see room for recovery; otherwise, concerns about this being a "flash in the pan" could intensify.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.

- CareyDunlop·2025-09-01Impressive strategy and analysis! 🌟😄LikeReport