Salesforce Q2: 10% Revenue Growth, Yet AI Contributes Only 3%: The Harsh Reality Behind CRM's Number

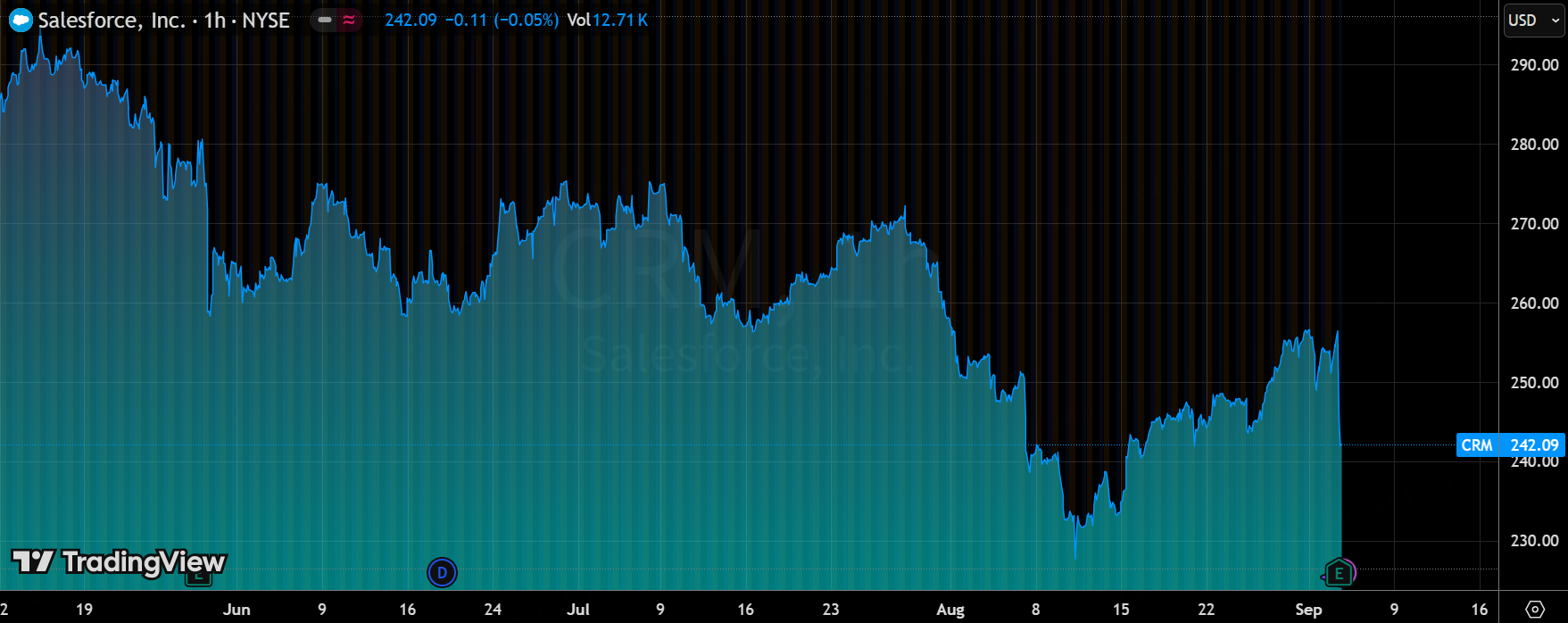

$Salesforce.com(CRM)$ released its Q2 earnings report, showing steady overall performance with revenue and profits slightly exceeding market expectations. This reflects the company's resilience in the SaaS sector and improved operational efficiency. However, the weak guidance highlights macroeconomic uncertainties and the slow monetization of its AI business, potentially signaling insufficient near-term growth momentum. Investors should be cautious about heightened stock price volatility.

Key Financial Highlights

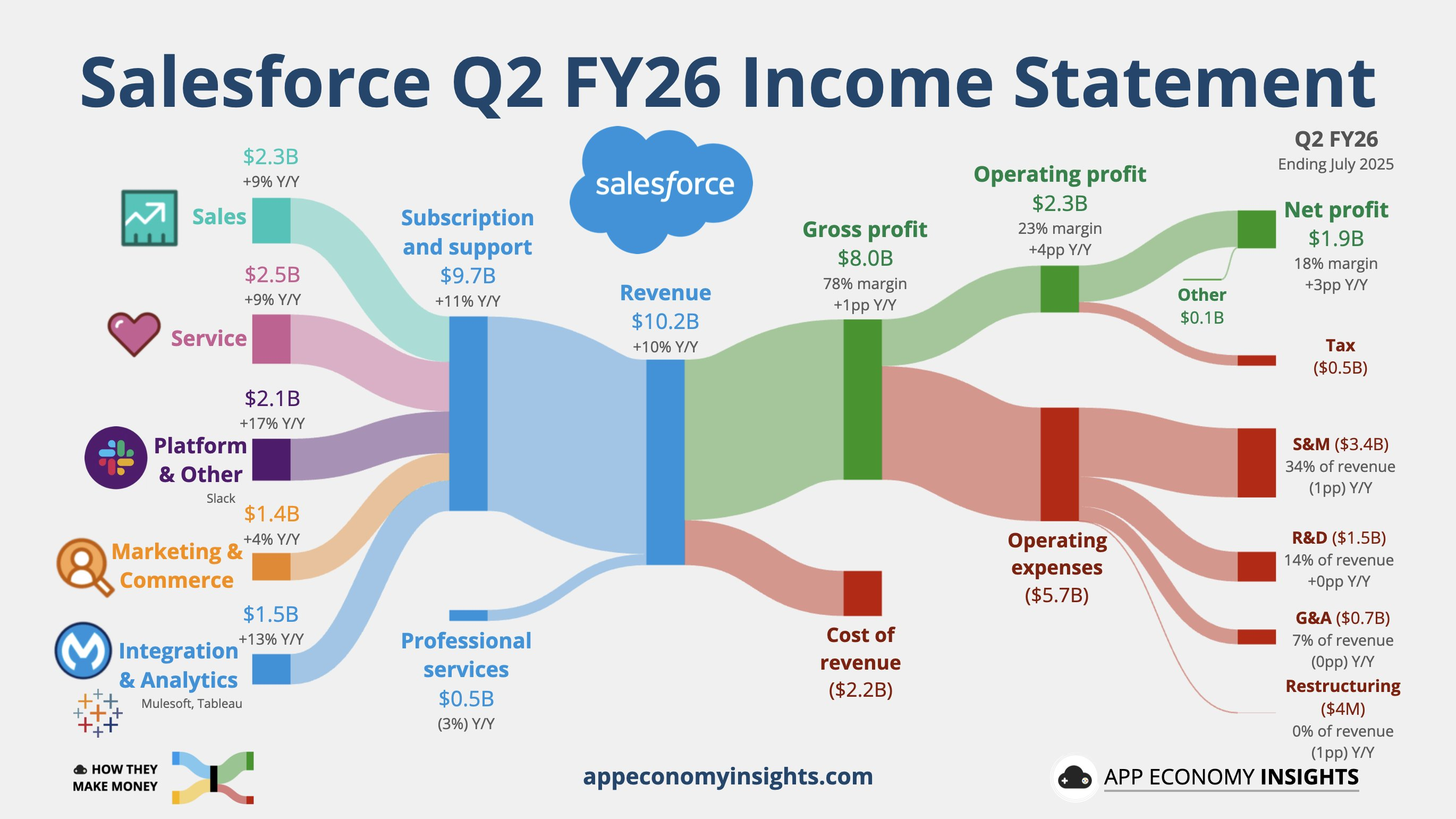

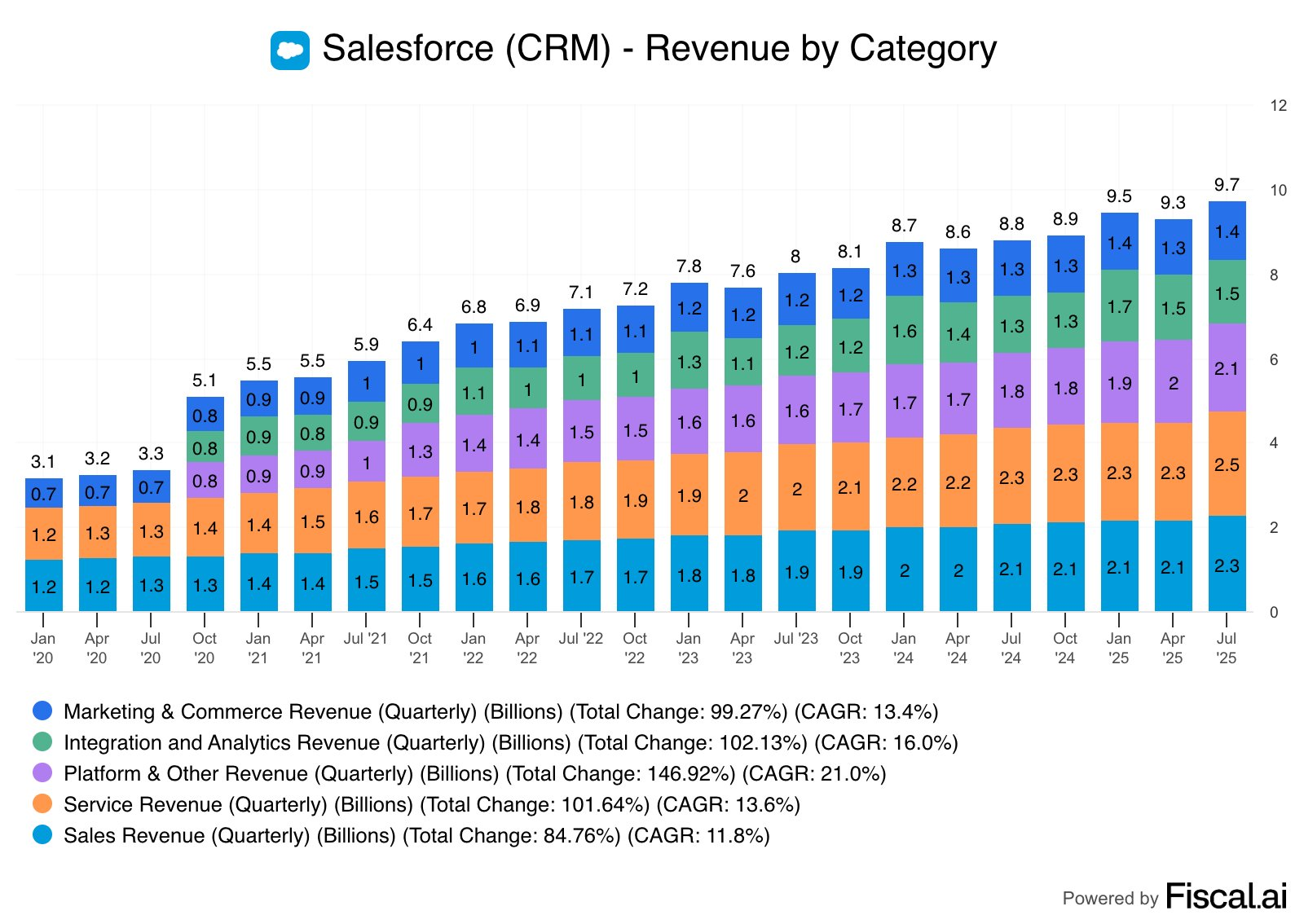

Total Revenue: $1.024 billion, up 10% year-over-year (improving by approximately 2.4 percentage points quarter-over-quarter). This growth rate slightly exceeded analysts' expectations of $1.014 billion, benefiting from positive currency effects and stable contributions from subscription businesses; however, at constant exchange rates, growth remained around 9%, indicating no significant breakthrough in core growth drivers. The outperformance primarily stemmed from cost control rather than a surge in demand. In terms of business structure, subscription and support revenue accounted for a substantial 95% of total revenue. However, the deceleration in Marketing and Commerce Cloud growth suggests emerging signs of saturation in the traditional SaaS sector.

Adjusted earnings per share (EPS): $2.91, representing a year-over-year increase of approximately 25%. This exceeded the market consensus of $2.78 by approximately 4.7%, primarily driven by the release of operating leverage. Expense growth was kept below 5%, pushing the non-GAAP operating margin to 33.5%, about 5 percentage points higher than expected. While this performance surpassed market consensus, excluding one-time tax benefits would reveal a more neutral profit quality, not significantly exceeding historical averages.

Current Remaining Performance Obligations (cRPO): $29.4 billion, up 10.9% year-over-year (11% at constant currency). The quarter-over-quarter growth rate slowed slightly by 1 percentage point. Although the company's August price increase prompted some customers to renew contracts early, new contract momentum was not robust. As a leading indicator of future revenue, this metric suggests growth sustainability remains acceptable but falls short of the 15% level seen in the same period last year. This may reflect the impact of cautious customer budgets or intensified competition.

Annualized Revenue from AI and Data Cloud: Approximately $1.2 billion, accounting for 3% of total revenue. This represents an increase from the previous quarter's $1 billion, but its contribution remains limited, driving overall growth by only 1-2 percentage points. Key drivers include initial adoption of Agentforce (over 4,000 paying customers), though the validation cycle is lengthy. This falls far short of market expectations for AI disrupting SaaS, with the business structure still heavily reliant on traditional CRM operations.

Earnings Guidance

Salesforce's Q3 FY2026 guidance indicates a revenue midpoint of $10.425 billion, representing approximately 8% year-over-year growth, which falls below the market consensus midpoint of $10.5 billion. More notably, the adjusted EPS guidance of $2.45 is significantly below the consensus estimate of $2.77 by 11.5%, suggesting an expansion in expenses likely directed toward increased AI R&D or M&A integration (such as the recent $8 billion acquisition of Informatica). Full-year revenue guidance remains at $41.1-$41.3 billion (8-9% growth), but EPS guidance has been raised to a median of $11.35, reflecting management's confidence in operational efficiency during the second half of the fiscal year.

During the earnings call, the company emphasized that "we are at a pivotal moment for AI CRM, with Agentforce poised to reshape enterprise productivity, though the macro environment requires us to remain cautious." This statement leans toward optimistic reassurance, attempting to shift focus through an AI narrative while sidestepping the specific reasons behind the Marketing Cloud's weakness—perhaps to preserve investor confidence.

Key Investment Considerations

From a structural perspective, Salesforce's core CRM and subscription business remains a sustainable long-term growth track, benefiting from the essential demand for enterprise digital transformation. Particularly, the 120% annual growth of Data Cloud demonstrates the potential in data management. However, the AI Agent narrative relies more on sentiment-driven hype, currently contributing only 3% revenue—similar to early cloud computing hype. If not validated in future quarters, it may become a short-term topic rather than a growth engine. We believe the maturing of traditional SaaS offerings (such as the slowing growth of Marketing Cloud) may signal that the company needs to accelerate its transition to an AI platform. Otherwise, its growth ceiling will become increasingly apparent.

From a valuation perspective, the current price-to-earnings ratio (approximately 30x FY2026 expected EPS) implies an annual growth expectation of 10-12%, which appears reasonable relative to $ServiceNow(NOW)$ (40x) and $Workday(WDAY)$ (35x). However, market pricing is already quite full, especially as concerns over AI substitution weigh on the broader software sector. In contrast, the Data Cloud segment holds greater undervaluation potential. Should its penetration rate rise from current lows, it could follow Adobe's AI integration trajectory, unlocking valuation expansion. The market's pessimistic interpretation of guidance may be excessive (e.g., 4% post-market decline), but Salesforce's dividend and share repurchases ($3.1 billion returned this quarter) could serve as a buffer, especially when compared to Booking's post-pandemic valuation recovery.

Strategically, management's approach shows no major missteps, though its AI investments warrant closer scrutiny—the Informatica acquisition will bolster data platformization, signaling a shift toward horizontal expansion to build an ecosystem integrating MuleSoft, Tableau, and others. However, the guidance on cost expansion may reveal conservative resource allocation. We recommend prioritizing investments in validating Agentforce over broad-based acquisitions to avoid integration dragbacks like those experienced with Slack.

Regarding variables, if cRPO growth continues to decline by more than 5%, it could serve as an early warning signal for valuation repricing. Conversely, an AI ARR exceeding $2 billion or the realization of M&A synergies could catalyze a stock price rebound, similar to the valuation uplift following Microsoft Azure's AI growth.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.

- Valerie Archibald·2025-09-04Everything can happen tomorrow , did a thoroughly financial analysis, yes It can go lower but one of the best value PE with solid fundamentals.LikeReport

- Jason_88·2025-09-04基本面未动摇 有什么可以担心的呢LikeReport

- Enid Bertha·2025-09-04You will see tomorrow, it will end the day around 250$.LikeReport

- MatSg·2025-09-04👍LikeReport