15% Crash! From IPO Frenzy to Rationality: Figma's Challenges Just Begun

Recently listed $Figma(FIG)$ released its first earnings report since going public. While Q2 revenue still grew by 41%, overall performance showed signs of fatigue. EPS fell significantly below expectations, triggering market concerns and causing the stock price to plummet nearly 15% in after-hours trading.

This quarter's highlights include robust expansion in user metrics and the launch of new AI products, yet underlying flaws are becoming increasingly apparent: declining net retention rates, weakening growth momentum, and impending pressure from share lock-up expirations may signal the company's return to rationality following the IPO frenzy, making short-term prospects difficult to view optimistically.

Key Financial Highlights

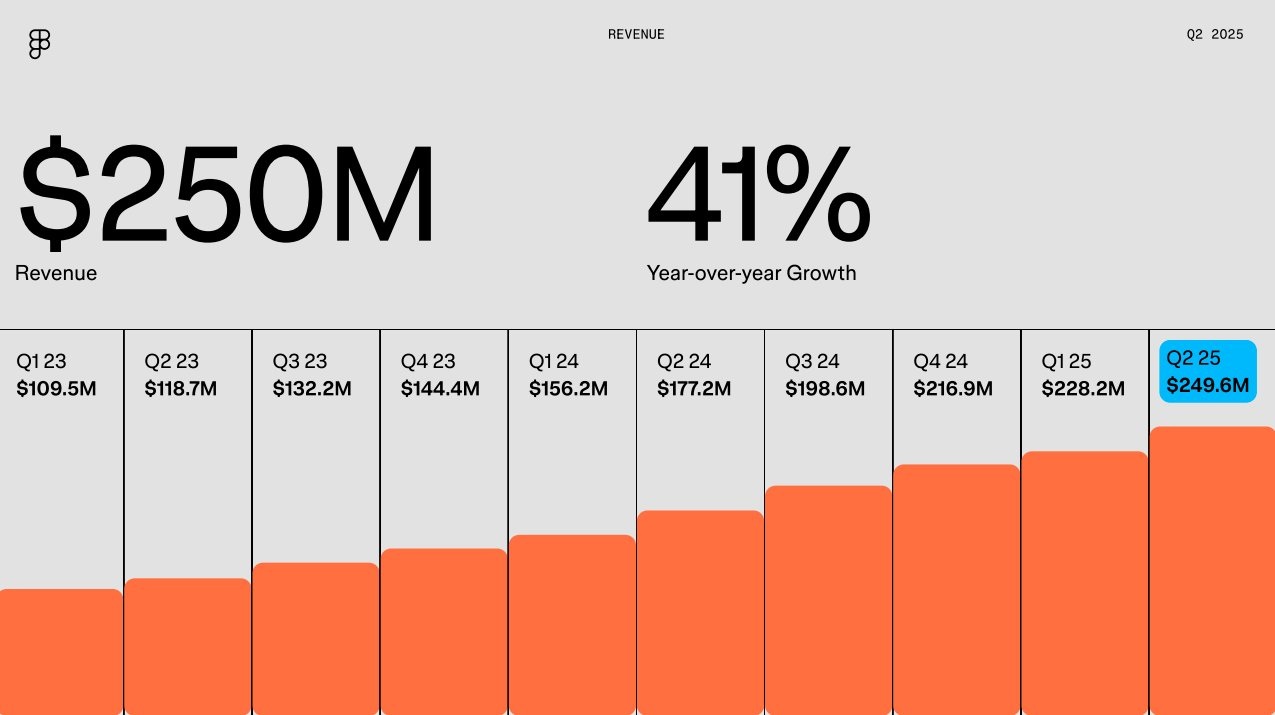

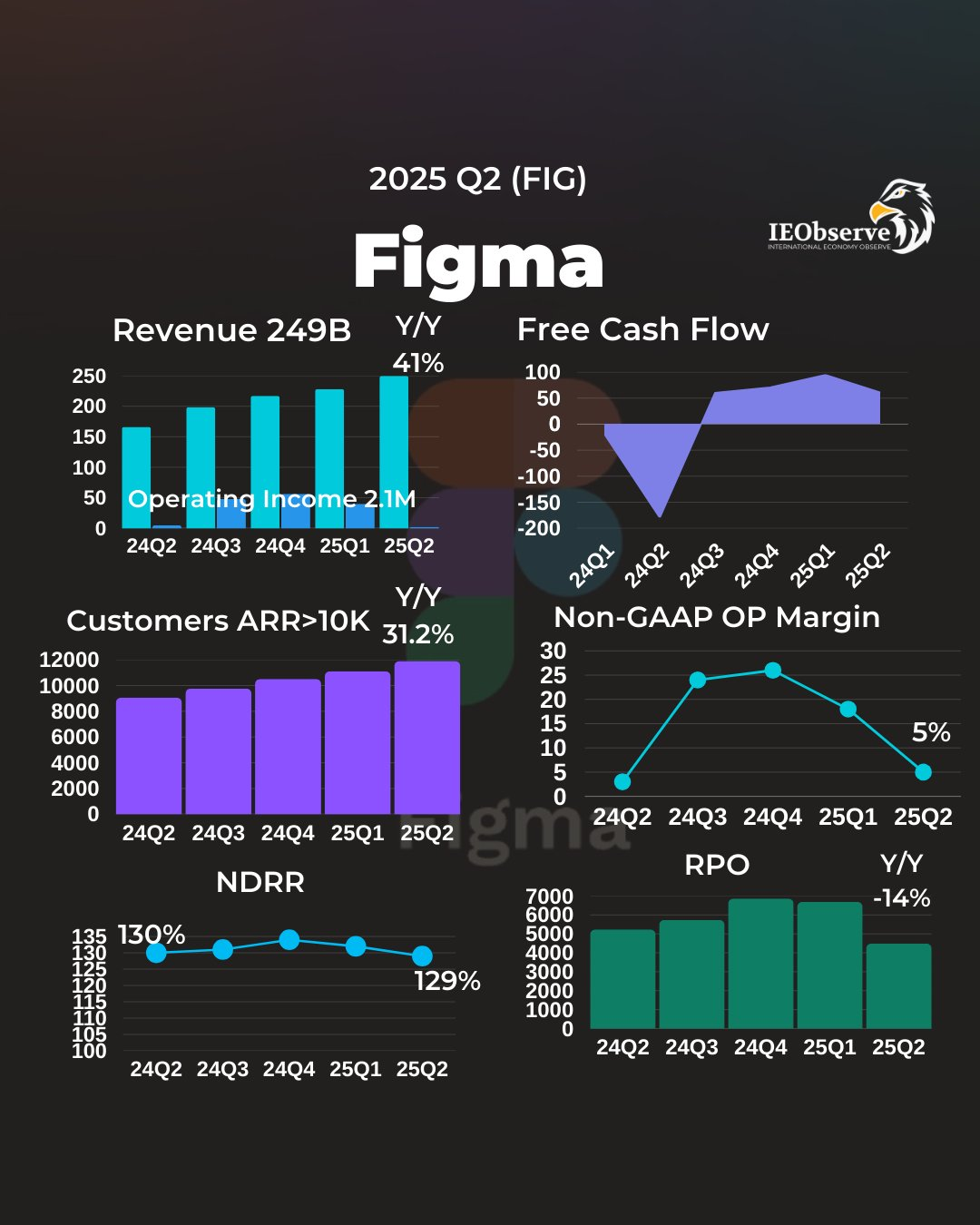

Revenue reached $249.6 million, representing a 41% year-over-year increase and approximately 9% quarter-over-quarter growth. This growth was primarily driven by the continued penetration of products like Dev Mode and the expansion of enterprise customers. However, the growth rate slowed compared to the previous quarter, falling slightly below the upper end of the company's own preliminary forecast range ($247-250 million), indicating signs of market saturation. While exceeding the analyst consensus of $248.8 million, it failed to boost confidence, reflecting a shift in growth drivers from rapid expansion to reliance on existing customer upgrades.

The Net Retention Rate (NDR) declined to 129%, down 3 percentage points from the previous quarter's 132%. This metric indicates slowing expansion among existing customers, potentially stemming from a tightening economic environment or intensified competition (such as the pursuit by Adobe and Canva). While remaining above 100% suggests sustainability, the downward trend implies the business relies on sentiment-driven short-term upgrades rather than structural growth.

Free cash flow and adjusted free cash flow reached $60.6 million, with a margin of 24%. The number of customers with annualized revenue exceeding $100,000 increased to 1,119 (from 1,031 in the previous quarter). These metrics underscore cash generation capabilities, though year-over-year growth has slowed. Potential signs of change lie in AI products (such as Figma Make) not yet being fully monetized, which may further impact cash flow stability in the near term.

Earnings Guidance

Meanwhile, the company remains cautious in its full-year outlook for Q3, projecting revenue between $247 million and $250 million for the quarter—implicitly indicating a slowdown in sequential growth to approximately 0-2%. While no specific full-year guidance was provided, the company emphasized that AI investments will continue.

Dev Mode's momentum is putting pressure on revenue growth," noting that AI product costs have been factored into the model but full-scale monetization has yet to commence. This guidance leans conservative, falling well below market expectations for rapid growth—perhaps reflecting a focus on managing expectations rather than aggressive expansion.

Key Investment Considerations

From a structural perspective, Figma's core design tool offerings (such as Figma Design and FigJam) remain a sustainable long-term growth track, benefiting from the digital collaboration trend and enterprise customer loyalty. However, AI-driven new products (like Figma Make and Sites) rely more heavily on market sentiment and short-term trends, similar to the explosive growth of Dev Mode in previous quarters. Once the innovation dividend fades, these products may face demand volatility. Historical comparisons reveal signs of NDR decline in the previous quarter, cautioning investors against over-relying on AI as a perpetual growth engine.

From a valuation perspective, the current price implies extremely high growth expectations—calculated at approximately 37 times price-to-sales ratio (far exceeding $Adobe(ADBE)$ s 6x or $Shopify(SHOP)$ 's 18x). the market appears overpriced, implying a sustained annual growth rate above 40% is required for support. However, Q2's EPS miss and declining NDR indicate limited downside potential. Compared to peers like Adobe (more mature ecosystem) and Canva (user growth at lower valuations), Figma's premium stems from IPO euphoria while overlooking competitive pressures. It may be repriced to a more realistic 20-25x range during an economic downturn.

Strategically, management's approach contains missteps, such as heavily investing in AI while delaying monetization. While this warrants amplified investment to seize platformization opportunities (e.g., expanding horizontally from design to development), signals indicating the company's shift toward platformization (e.g., acquiring Modyfi and Payload) may delay profitability due to cost erosion. We believe greater emphasis should be placed on monetizing existing customers rather than pursuing blind expansion, thereby avoiding a repeat of Workday's early-stage fate where a high valuation bubble ultimately burst.

Regarding key indicators, investors should continuously monitor NDR (a break below 125% signals a warning), AI product penetration rates (such as the proportion of paying users), and shifts in DAU/GMV structure. These factors could serve as catalysts—for instance, if AI-powered credit consumption outperforms expectations, it may trigger re-pricing and upward valuation adjustments. Conversely, if macroeconomic tightening leads to customer attrition, it could become a downside risk factor.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.

- Merle Ted·2025-09-04This is going to be a squeeze play! The biggest squeeze is coming and Figma is got its name written in the record books!LikeReport

- Mortimer Arthur·2025-09-04All the shorts will cover in the morning! And we will ride back up to the mid 80's. Thanks in advance shorts!LikeReport

- MatSg·2025-09-04👍LikeReport