Big-Tech Weekly | How ORCL/AVGO Creating 'Multi-Core' AI-Eco? Unpacking Tesla's Rally To $400

Big-Tech’s Performance

Macro Headlines This Week:

Indices Hit New Highs Amid Increased Volatility. The three major indices repeatedly set new closing records this week, with the Nasdaq performing particularly strongly, driven by tech stocks. However, due to disappointing inflation (CPI rose to 2.9% year-on-year from 2.7% in July) and employment data (approximately 22,000 new jobs added, which is relatively low; the unemployment rate rose to about 4.3%, and initial jobless claims surged to 263,000), market sentiment began to diverge, and concerns about stagflation (stagnation + inflation) intensified.

Oracle's Surge Sparks Debate Over AI Concept Hype. The AI narrative received a boost from ORCL's earnings report and positive cloud service contracts, leading to a one-day surge of approximately 36%. This once again highlighted the market's strong expectations for AI infrastructure demand, but also raised concerns about an "AI bubble," especially as valuations continue to be pushed higher while profit growth may not be broadly sustainable.

Market Widely Expects First Rate Cut at September FOMC Meeting, anticipated to be 25 basis points. However, due to persistent inflation (particularly in services and housing), the Fed faces a dilemma between "easing policy" and "maintaining its anti-inflation credibility." The data presents a mixed picture of loosening employment and rebounding inflation, forcing the Fed to proceed cautiously: cutting rates too quickly or too much could let inflation become entrenched; not cutting could further pressure economic growth and employment.

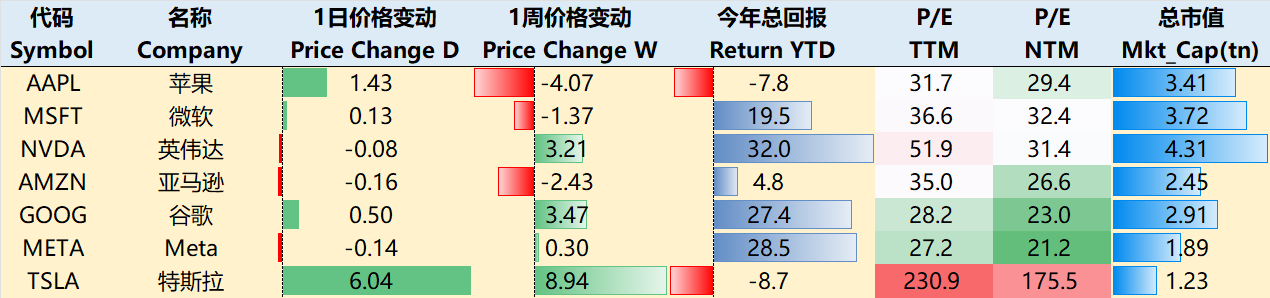

Big Tech maintained a steady upward trend this week. As of the close on September 11th, the weekly performance was: $Apple(AAPL)$ -4.07%, $Microsoft(MSFT)$ -1.37%, $NVIDIA(NVDA)$ +3.21%, $Amazon.com(AMZN)$ -2.43%, $Alphabet(GOOG)$ $Alphabet(GOOGL)$ +3.47%, $Meta Platforms, Inc.(META)$ +0.3%, $Tesla Motors(TSLA)$ +8.94%.

Year-to-date returns show only AAPL and TSLA are still in negative territory, but there's potential for them to turn positive.

Big-Tech’s Key Strategy

Is Oracle's AI Order Bluffing?

Following Oracle's (ORCL) earnings, the biggest highlight is its signing of a 5-year, $300 billion AI cloud computing agreement with OpenAI. In other words, from now on, ORCL could become the large-cap tech stock most closely associated with OpenAI news, potentially replacing MSFT and AMZN in the market's conventional perception. The core question now is whether ORCL can transition from a "cloud company" to a "Hyperscaler," which will determine its valuation and growth path.

The valuation logic investors are currently applying is: optimism for FY2029 EPS between 14 17 (consensus expectations are around 13.5),withsomemorebullishinvestorsevenseeing19~20.Usinga30xP/Eratio,thestockpricerangewouldroughlybe420~510.Forecastsfor2030generallyfallbetween17~$20+.

However, what truly determines ORCL's valuation ceiling is the profit margin of OCI (Oracle Cloud Infrastructure). Safra [Catz] provided revenue guidance for 2030 during Investor Day, but the market is more concerned about how future growth translates to operating margins. If OCI margins can align with the consolidated business post-acquisition (around 35%), it would result in "explosive" EPS figures. But many investors, including institutions, admit that no one truly sees clearly how far OCI margins can go. In other words, predicting FY2029/2030 EPS is essentially betting on whether OCI gross margins will reach 20% or 35%. The difference between these two assumptions is enormous.

Among different investment banks' views, beyond the surprise at the massive orders (known information), there is greater focus on the feasibility of execution and the methods.

The Optimists (e.g., Citi, Goldman Sachs) focus more on the potential of the growth story and the market's underestimation.

The Cautious (e.g., JPMorgan, Morgan Stanley) delve deeper into potential significant risks, including high customer concentration (reliance on a few giants like OpenAI), doubts about the customers' own long-term payment capacity, and pressure on financials from massive capital expenditures and financing needs (negative free cash flow, high net debt).

ORCL's unexpected surge post-earnings can be seen as a gear shift for capital's "new favorite." Over the past few years, the market's AI consensus was "NVIDIA is king" because its GPUs are the core of computing power. But after Oracle disclosed the $300 billion deal with OpenAI and released potential revaluation space for OCI margins, the market began to realize that value capture in the AI industry chain wouldn't stop only at the chip level. Capital is starting to flow partially from NVDA, the "old flame," to "new favorites" like ORCL and $Broadcom(AVGO)$ . AVGO is cut in AI infrastructure through networking and custom chips, while ORCL is leveraging databases + cloud services to capture incremental demand. Investor preference is gradually shifting from "betting on the hardware leader dominating alone" to "seeking multi-point blooming infrastructure providers."

The AI story is evolving from being single-core driven by GPUs to multi-core driven by cloud, data, and networking. Capital is also starting to favor "second-tier giants" that are directly linked to AI demand and have confirmed orders, rather than continuing to all-in on NVDA.

Big Tech Options Strategies

This week we focus on: When Tesla's narrative becomes "Optimus as the engine for market cap growth"

In early September, TSLA's board proposed the most aggressive incentive plan in corporate history for Elon Musk, likely to be approved at the November 6th shareholder meeting. If Musk achieves all targets, its potential value could reach 1trillion,farexceedinganycurrentexecutivecompensationglobally.ThecoreobjectiveofthisplanistoincreaseTesla′smarketcapfrom1.3 trillion to $8.5 trillion within ten years, equivalent to creating six more Nvidias. Its realization path heavily relies on disruptive breakthroughs in artificial intelligence and robotics technology.

How to achieve it?

Optimus' Strategic Central Role. The company plans mass production of Optimus in 2026. When annual production reaches 1 million units, the marginal cost could drop to 20,000−25,000, only 1/6th of Boston Dynamics' Atlas robot, making it the core engine for market cap growth and potentially contributing 80% of Tesla's long-term value. The third-generation Optimus design is complete.

Robotaxi and FSD Synergy. With 1 million self-driving taxis deployed, their dispatch system reuses FSD's Occupancy Network model, achieving 3D environment reconstruction through multi-camera fusion. Annual revenue could reach $951 billion, far exceeding Uber's current scale, and Tesla could capture 40-60% of the收益 through a sharing model.

xAI's "Dark Horse" Value. The Grok model is already integrated into Tesla vehicles, and its multimodal interaction capabilities can improve FSD's decision-making efficiency in complex scenarios. If Tesla acquires xAI (valuation 1750−2000 billion), both parties could share computing resources — xAI's Colossus supercomputer boasts 100,000 Nvidia H100 chips.

Furthermore, it is also possible that...SpaceX?

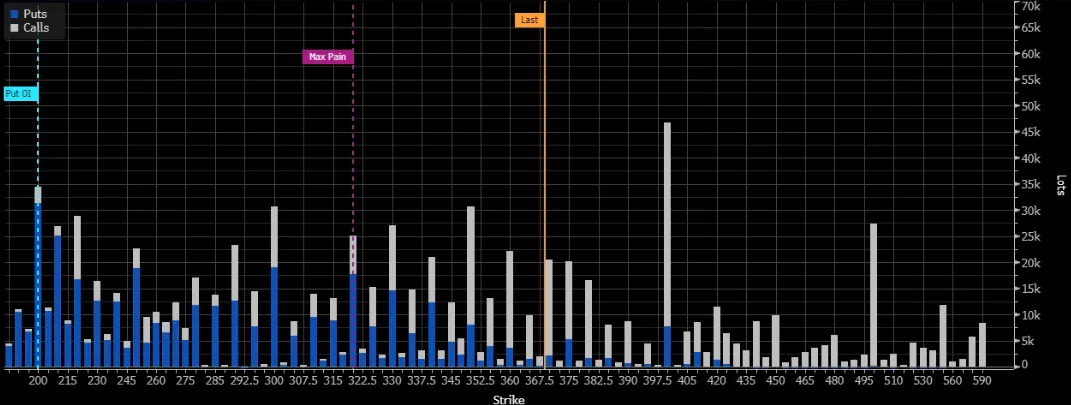

TSLA has performed stronger than other Mag7 companies over the past 5 trading days, up +6% in a single day. This wave has the potential to challenge $400 again. From an options perspective, the proportion of bets on Calls for September 19th (monthly options) is not low.

Big Tech Portfolio

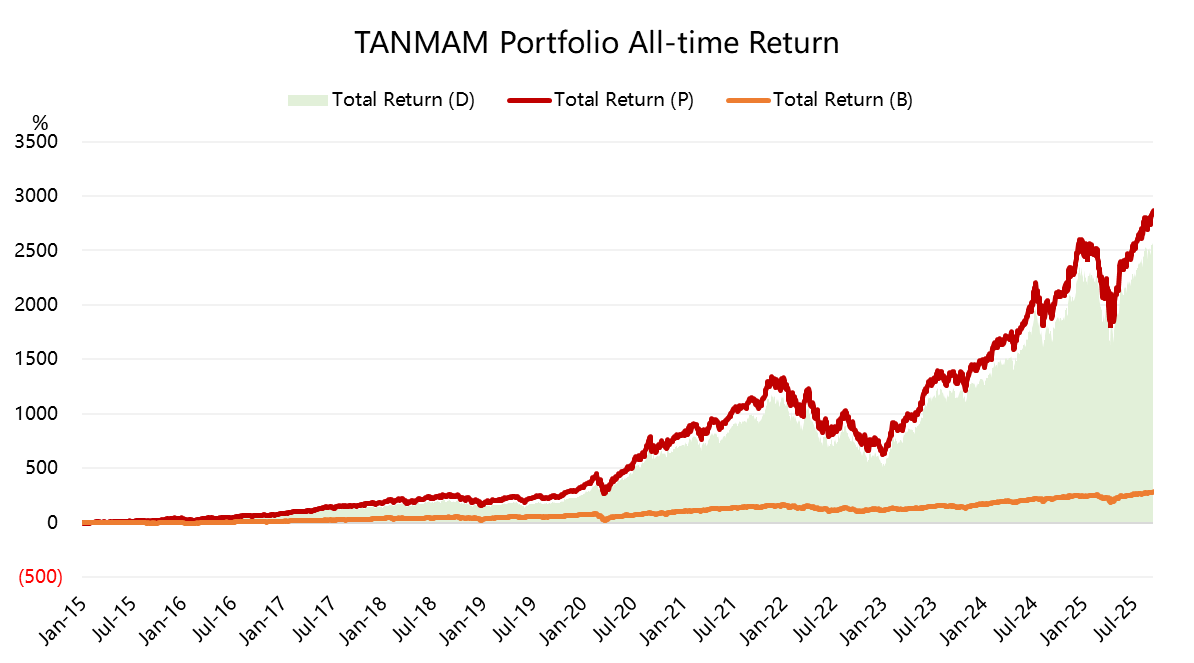

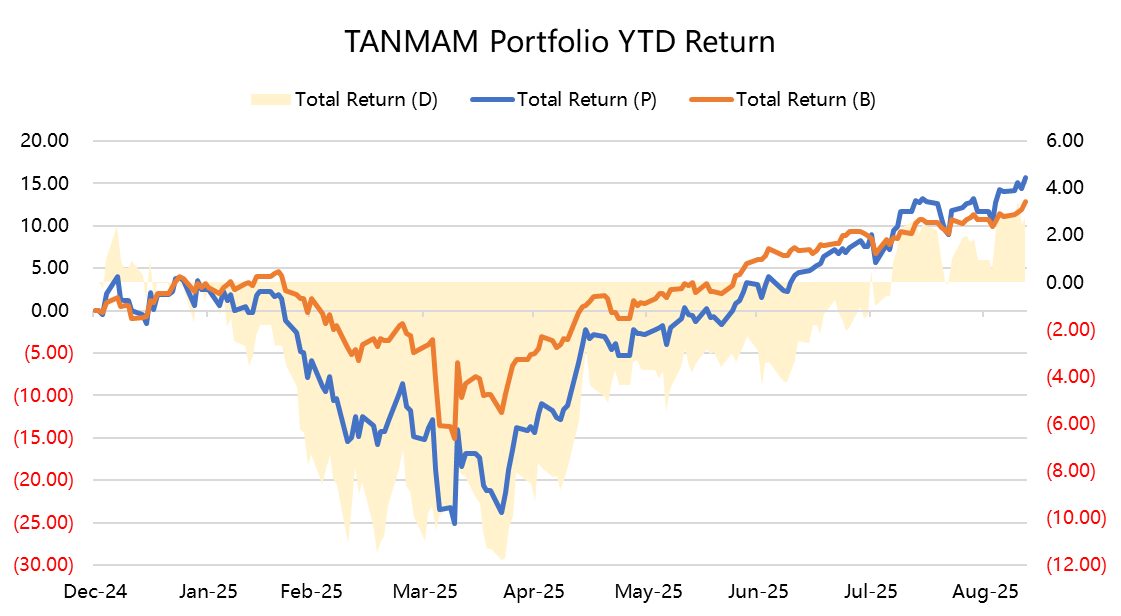

Forming an investment portfolio with the Magnificent Seven ("TANMAMG" portfolio), equally weighted and rebalanced quarterly. Backtest results show performance far exceeding the $S&P 500(.SPX)$ since 2015, with a total return reaching 2867.47%, compared to $SPDR S&P 500 ETF Trust(SPY)$ return of 283.65% over the same period, resulting in an excess return of 2583.81%, once again hitting a new high.

Year-to-date, Big Tech returns have reached new highs at 15.66%, outperforming SPY's 12.88%.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.

Great article, would you like to share it?