Big-Tech Weekly | NVIDIA and Intel Reshape AI Future; iPhone 17 Pre-Orders Skyrocket!

Big-Tech’s Performance

Macro Headlines This Week:

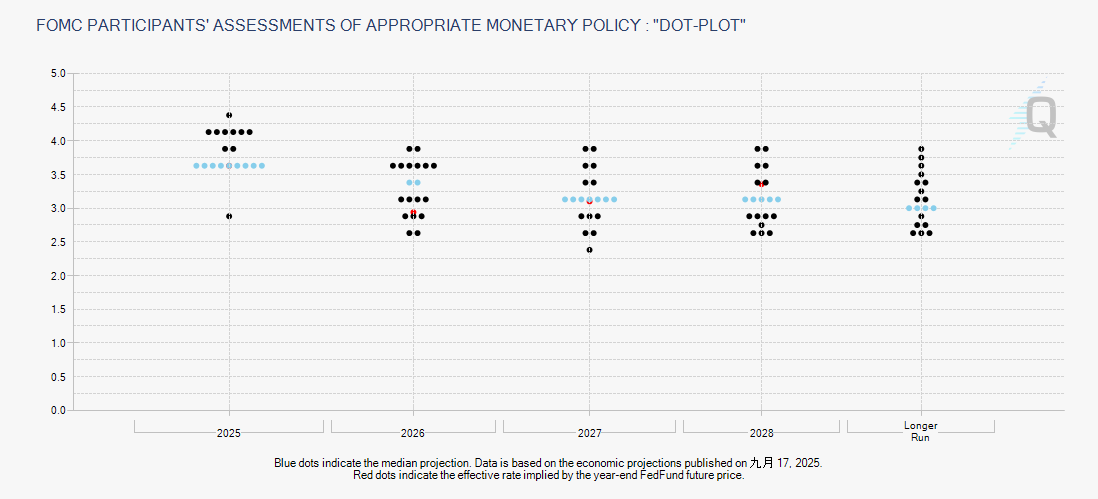

The Fed's first rate cut in nearly a year signals a softening labor market. On September 16, the Federal Reserve lowered the federal funds rate by 25 basis points—the first cut since December 2024. The decision was driven primarily by weakness in the labor market and inflation that remains not fully under control. The Fed's economic projections (dot plot) indicate there could be two more rate cuts in 2025 (in October and December). However, internal opinions aren't fully aligned; new board member Stephen Miran advocates for a larger cut, while some officials remain wary of upside inflation risks. With job growth slowing but inflation still sticky, economists are once again warning of the risk of "stagflation" in the U.S. (slow growth + high inflation).

The tech sector remains a key market driver, particularly subsectors like AI, semiconductors, and cloud infrastructure, though much of the momentum stems from forward-looking expectations and strategic positioning. While market sentiment is buoyant, valuations for some tech stocks are already elevated. For companies whose earnings growth isn't reliably steady or that rely on single drivers (like AI hype or external subsidies), any slowdown in the pace of rate cuts or an inflation rebound could heighten the risk of valuation pullbacks.

Markets widely anticipated the first rate cut at the September FOMC meeting, with expectations centered on a 25-basis-point move. That said, inflation (especially in services and housing) remains resilient, leaving the Fed in a bind between easing policy and preserving its anti-inflation credibility. Data shows a mixed picture of loosening employment + rising inflation, forcing the Fed to tread carefully: Cut too quickly or deeply, and inflation could spiral out of control; hold back, and growth and jobs could face further pressure.

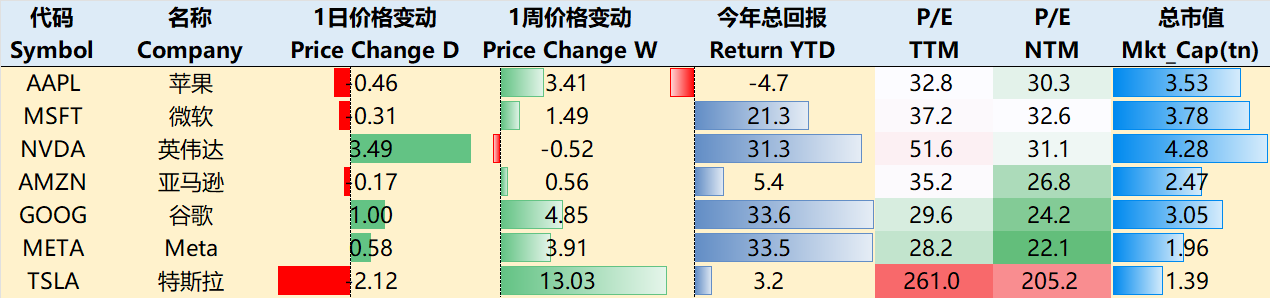

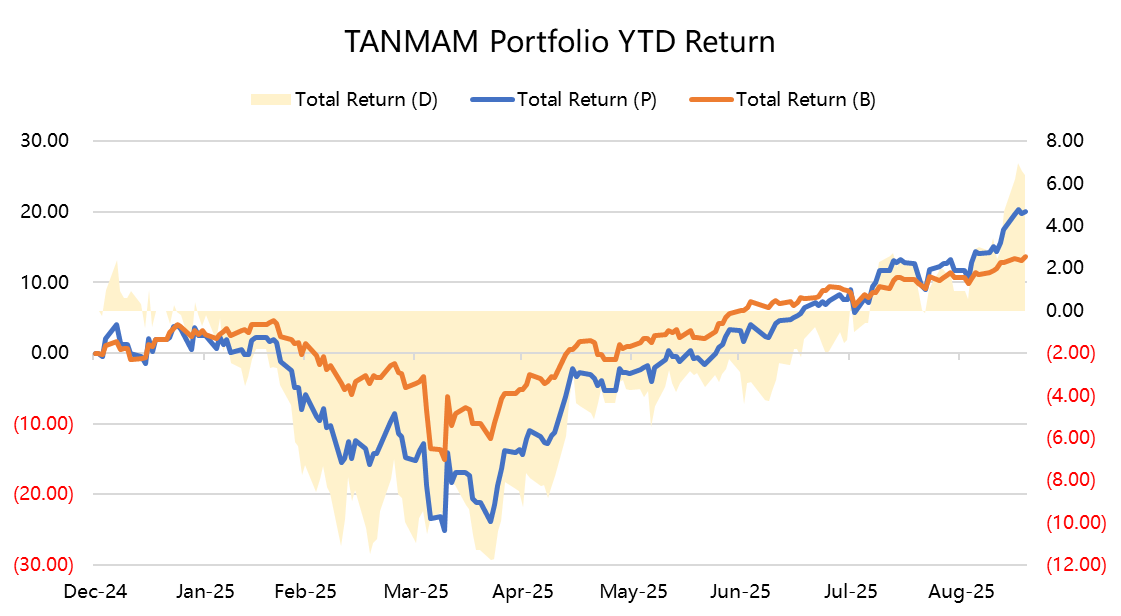

Big Tech stocks continued their steady upward grind this week, with Tesla shining brightest and flipping to positive YTD returns. As of the September 18 close, the past week's gains were: $Apple(AAPL)$ +3.41%, $Microsoft(MSFT)$ +1.49%, $NVIDIA(NVDA)$ -0.52%, $Amazon.com(AMZN)$ +0.56%, $Alphabet(GOOG)$ $Alphabet(GOOGL)$ +4.85%, $Meta Platforms, Inc.(META)$ +3.91%, $Tesla Motors(TSLA)$ +13.03%.

Year-to-date returns: Only AAPL is still in the red, but it could turn positive soon.

Big-Tech’s Key Strategy

NVDA and INTC's Unexpected Union: A Mixed Bag?

NVIDIA announced a strategic partnership with $Intel(INTC)$ , including a $5 billion investment to develop AI PC and AI server solutions. This isn't just a cash infusion—it's a pivotal event that could reshape the industry landscape.

For INTC:

Strategic Endorsement and Capital Structure Boost. Following the U.S. government's equity injection via the CHIPS Act, NVIDIA's investment further cements Intel's "Too Big to Fail" market narrative. It's reminiscent of the 2010s logic when Intel, Samsung, and TSMC jointly invested in ASML—this deal will accelerate Intel's push into advanced nodes (like 14A).

Dual Boost for Products and Foundry. NVIDIA will collaborate deeply with Intel on SoCs combining x86 CPUs and GPUs, helping Intel reclaim a core spot in HPC. The funds will secure execution on the 14A node's 2029 mass production roadmap and pave the way for potential splits in its products/foundry businesses.

Advanced Packaging (EMIB/Foveros) Gets a Heavyweight Vote of Confidence. This could ramp up external foundry orders and strengthen Intel's bargaining power in the post-Moore era.

Strategic Value for NVDA:

Full CPU Spectrum Coverage. With ARM's Grace already in its fold, tying up with Intel's x86 locks in the entire CPU architecture map. If future Rubin-series products adopt x86, it could expand NVDA's reach in HPC and AI PCs, significantly squeezing AMD's strategic room.

Supply Chain Security. Intel's domestic capacity and government backing help NVDA mitigate export controls and geopolitical risks to ensure steady supply.

Long-Term Synergies: Their PC-end SoC collaboration could swiftly define AI PC standards and erode AMD's Ryzen APU TAM. Industry estimates suggest that if Intel's x86 + RTX SoC captures 5–15% of the AI PC market by 2027, AMD's APU annual revenue could take a $130–380 million hit

Spillover Effects on Other Competitors:

$Taiwan Semiconductor Manufacturing(TSM)$ : Short-term risks are limited—TSMC remains NVIDIA's sole foundry for core GPUs, and AI GPUs (H100, B100, and subsequent Blackwell series) demand cutting-edge nodes (N4 → N3 → N2) that Intel's current 18A/14A can't handle yet, so NVDA won't shift GPU tape-outs. Long-term, watch the structure: If Intel's 14A advances smoothly and pulls in NVDA for some x86 SoCs or lower-end AI chips, TSMC could lose share in specific lines. But with TSMC's leading-edge advantage likely holding through 2030 and low exposure to networking/PC chips, risks are manageable.

$Advanced Micro Devices(AMD)$ : Short-term market jolt is muted, but long-term pressure mounts in data center CPUs and PC APUs. For data centers, if the Intel+NVDA alliance grabs 6–22% of AMD's EPYC market share over the next three years, that's $80–290 million in annual revenue leakage.

$ARM Holdings(ARM)$ : NVDA reaffirms support for Grace, but its x86 embrace undercuts ARM's data center penetration thesis, souring investor sentiment.

$Synopsys(SNPS)$ : Markets had fretted over Intel scaling back partnerships, but with the collab details now clear, it's a net positive—shares have rebounded over 10%.

$Astera Labs, Inc.(ALAB)$ : The NVLink-over-PCIe trend introduces structural uncertainty, but if AI server shipments rise overall, PCIe/CXL demand could still drive volume growth.

$KLA-Tencor(KLAC)$ : Good news ripples through the semi equipment chain; short-term 2026 low-CapEx guidance holds, but long-term Intel CapEx outlook improves.

Big Tech Options Strategies

This Week's Focus: Will iPhone 17 Be AAPL's Catalyst?

Apple's iPhone 17 series, launched in September 2025, saw a strong opening weekend for pre-orders, with overall demand topping last year's iPhone 16. Per reports from multiple analysts, pre-order figures exceeded expectations, prompting Apple to ramp up production plans for 86–90 million iPhone 17 units in the second half of 2025.

In detail, demand for the Pro Max model was hottest, with Q3 production surging 60% YoY while maintaining similar shipping timelines—highlighting the pull of premium models. Pro series delivery times stretched longer: U.S. Pro Max averaged 22.5 days, international 24 days; U.S. Pro 14.2 days, international 18.1 days—all beating last year, suggesting a stabilizing upgrade cycle. The standard iPhone 17 clocked U.S. delivery at 15.5 days and international at 19 days, another positive sign. Pre-orders in China were even stronger YoY, bolstering global demand recovery.

That said, not every model sailed smoothly. The new iPhone Air, positioned as a slimline option, had ample stock on hand during the first weekend, with delivery times of just 6.7 days in the U.S. and 7.9 days internationally—seemingly softer than last year's iPhone 16 Plus (~2 weeks). But factor in its production volume exploding 200% YoY to triple last year's Plus levels, and as Apple's first ultra-thin model, pre-orders may not yet capture pent-up demand from thin-design fans. Watch in-store sales post-launch, especially among style-conscious buyers. In emerging markets like India, iPhone 17 pre-orders crushed iPhone 16, fueled by Diwali timing—Q3 sales could top 5 million units. Overall pre-orders rose 25% YoY, thanks to better supply chain prep and buzz around AI upgrades.

From aggregated sources, iPhone 17 is off to a solid start, but caveat: Delivery times are bullish but not a foolproof predictor of 12-month shipments. Strong demand could steady Apple's phone biz, but the Air's long-term traction remains a wildcard that could sway overall targets.

On launch day, AAPL shares dipped 1.5–3.2% amid worries over lackluster innovation and unchanged base pricing—only to rebound on robust pre-order data, up 1.1% to $236.57 on Monday. Some see the pullback as a buying dip; if iPhone 17 momentum holds, it could fuel a year-end rally. Overall, though, iPhone 17's stock lift is modest—more reliant on services and the pipeline—but early vibes are optimistic.

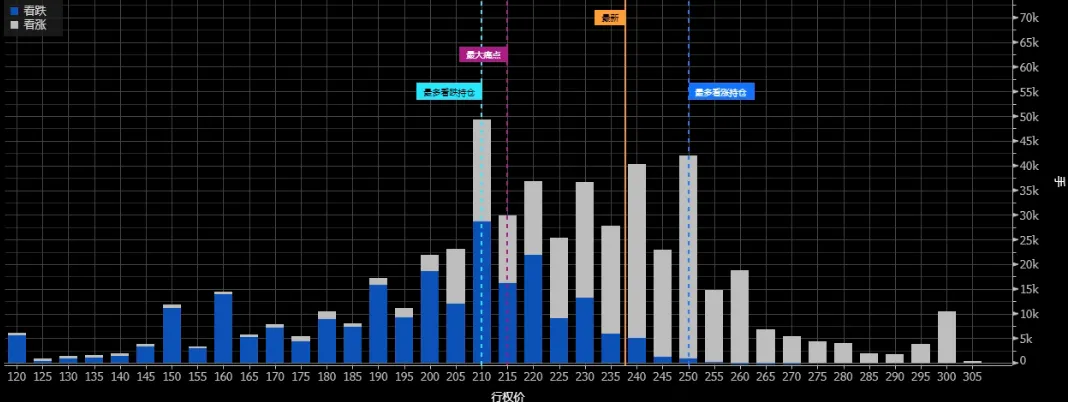

From an AAPL options lens, gamma is screaming high right now: September 19 weekly ATM gamma is sky-high (with some triple-witching influence). But October 17 monthlies also rank high among the Mag 7 (second to NVDA), signaling potential wild delta swings and gamma squeezes. Open interest in October calls piles up heavily at 235–260; any fresh catalysts could flip AAPL YTD back to green.

Big Tech Portfolio

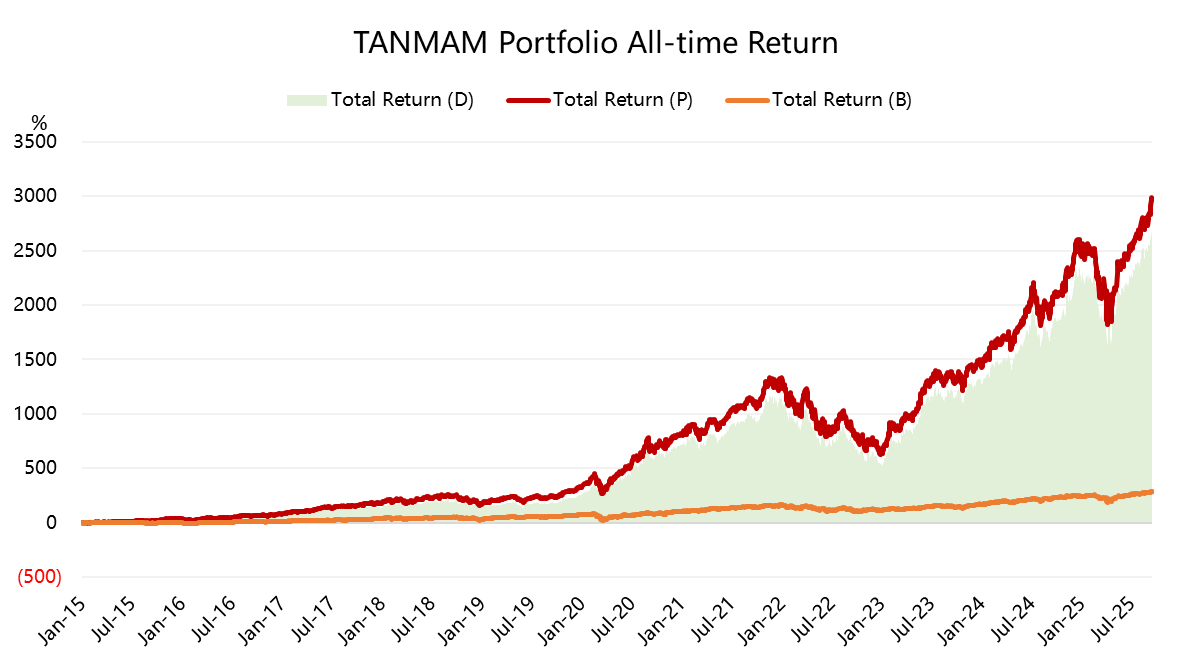

The Magnificent Seven form an equal-weight investment portfolio ("TANMAMG"), rebalanced quarterly. Backtests since 2015 show it crushing the $S&P 500(.SPX)$ , with total returns hitting 2,980.2% vs. $SPDR S&P 500 ETF Trust(SPY)$ 's 286.35%—an alpha of 2,693.85%, a fresh all-time high.

YTD, Big Tech's gains have hit a new peak at 20.06%, topping SPY's 13.67%.

$NASDAQ(.IXIC)$ $NASDAQ 100(NDX)$ $ProShares UltraPro QQQ(TQQQ)$ $ProShares UltraPro Short QQQ(SQQQ)$ $Invesco QQQ(QQQ)$

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.

- Merle Ted·2025-09-20After hitting record high after record high into earnings I believe Nvda is going through consolidation again. Guess what will more than likely happen into next earnings? Yep, rinse and repeatLikeReport

- Venus Reade·2025-09-20NVDA should be $200 already lol they are supplying the AI revolution!LikeReport

- AGaby·2025-09-20Very good detailed insights on AI tech and the foundries and the chefs are fantastic1Report

- Goldbars72·2025-09-20what is the difference between short sell and long sell or buy?1Report

- LouisLowell·2025-09-19Incredible insights on the tech landscape! [Wow]LikeReport

- YueShan·2025-09-20Good ⭐⭐⭐LikeReport

- Brando741319·2025-09-20GoodLikeReport

- Calwsh·2025-09-19Love itLikeReport