AI Dream Crumbles? HPE's FY26 Forecast Sparks Market Panic.

$Hewlett Packard Enterprise(HPE)$ saw its stock price drop sharply by nearly 9% in after-hours trading following the financial outlook disclosed at its October 15, 2025 securities analyst meeting.

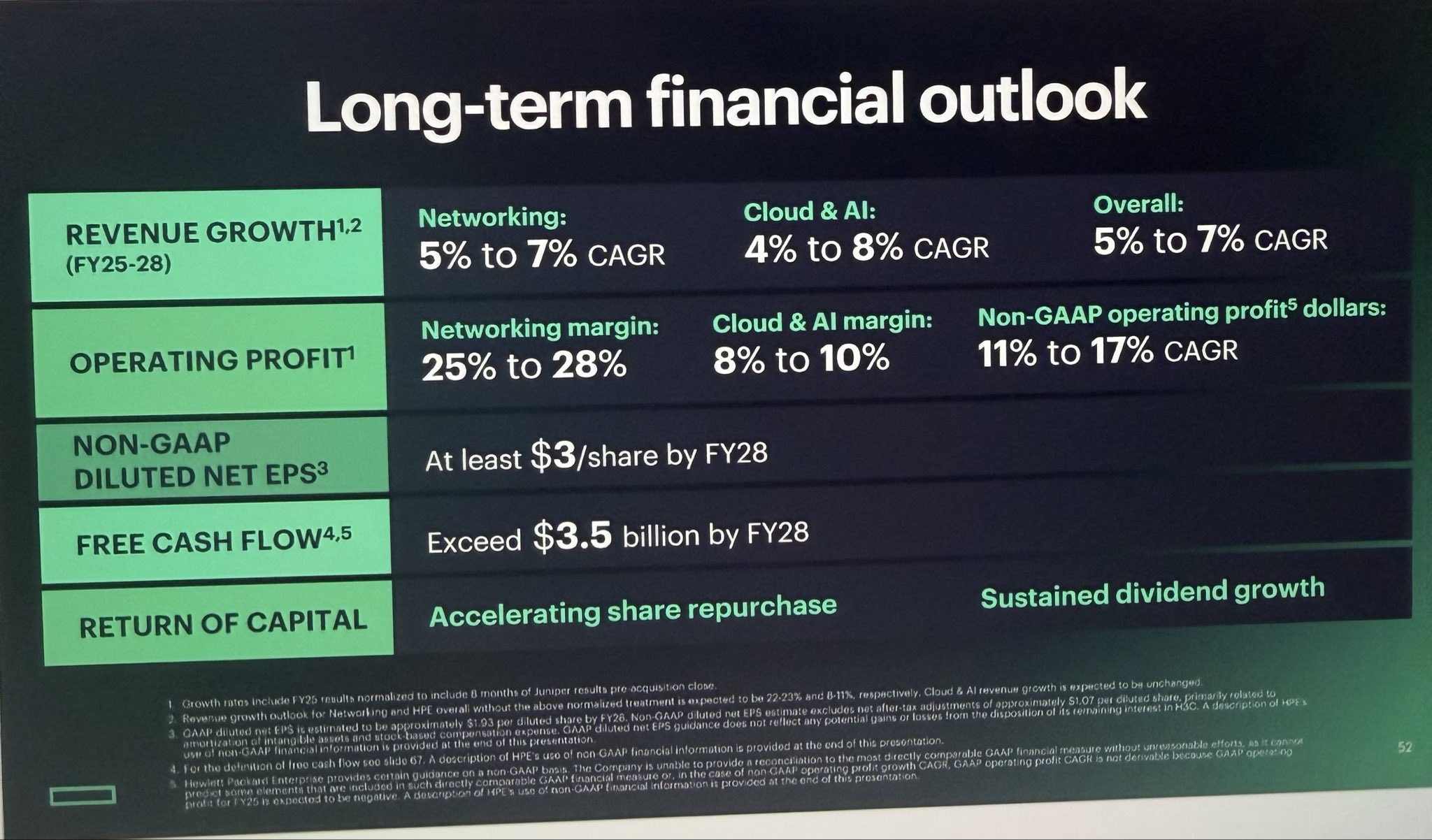

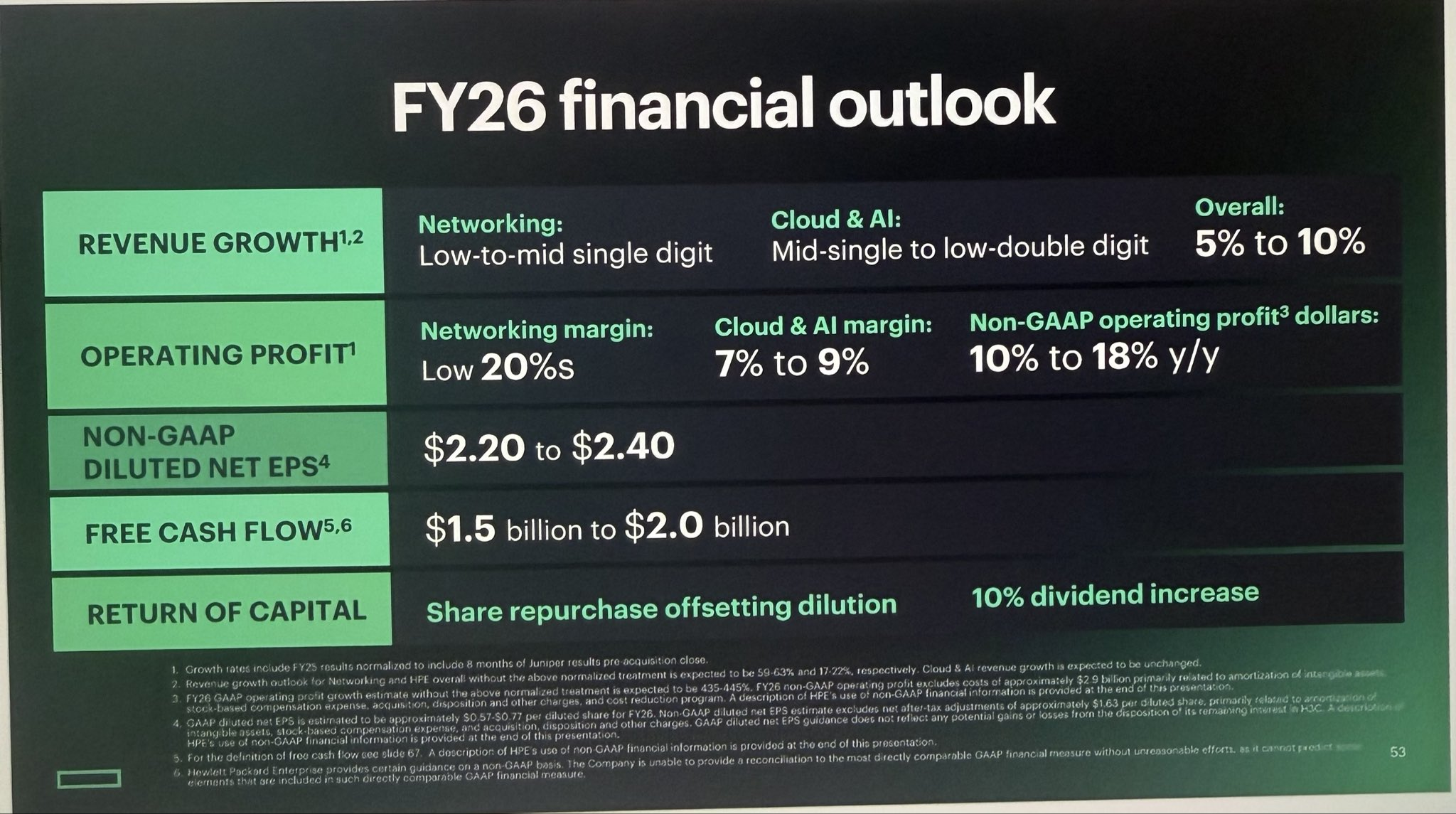

From a data perspective, the conservatism of this guidance is evident. HPE projects low to mid-single-digit revenue growth for its networking business in FY26, while its Cloud and AI segment is expected to transition from mid-single-digit to low double-digit growth. The overall operating margin target is set at the low 20% range, with non-GAAP operating profit growth controlled between 10% and 18% annually. Free cash flow is projected at $1.5 billion to $2.0 billion, significantly below analysts' optimistic estimates of $2.4 billion. Against its long-term targets, the company reaffirmed its FY28 compound annual growth trajectory: overall revenue at 5% to 7%, Cloud and AI at 4% to 8%, with Networking poised for robust expansion exceeding 10%. Non-GAAP EPS is targeted at a minimum of $3.00, with free cash flow surpassing $3.5 billion. While these long-term projections remain stable, FY26's specific figures show insufficient acceleration, particularly given market expectations for more pronounced synergies following the Juniper acquisition. The company explicitly excluded any revenue synergies from its FY26 outlook, designating this year as an integration transition period accompanied by approximately $2.9 billion in one-time costs, including intangible asset amortization.

Multiple analysts quickly voiced differing opinions after the meeting.

On one hand, some observers attribute the cautious guidance to real-world challenges. For instance, HPE faces marginal pressures in AI server construction, including supply chain volatility and intensifying competition—factors that have already squeezed profit margins at peers like Dell. Management noted during the conference call that the "Catalyst" program is projected to yield at least $350 million in savings by FY28, though these benefits will be incremental rather than immediately boosting FY26 performance.

On the other hand, while the 5% to 10% revenue guidance appears modest, excluding Juniper's full-year contribution (FY25 only covers four months) implies an even lower organic growth assumption. This reflects the company's caution regarding macroeconomic uncertainties, including slowing corporate spending and geopolitical risks. Conversely, optimistic voices suggest this outlook may underestimate the explosive potential of AI demand. HPE CEO Antonio Neri reiterated during the call that the company will align investments to capture market share in enterprise and sovereign AI segments, anticipating these areas will drive a medium-to-long-term rebound. However, in the near term, this defensive positioning failed to inspire bullish sentiment, triggering a wave of after-hours selling.

Turning to the impact on HPE itself, this incident highlights the growing pains of strategic transformation. The company is evolving from a traditional hardware supplier toward an AI and edge computing-dominated ecosystem, but the complexity of integrating Juniper has become a key stumbling block. While this acquisition strengthened networking capabilities, it brought short-term amortization burdens and operational overlaps requiring adjustments. Data indicates HPE shipped over 5,000 Alletra MP arrays by 2025, achieving triple-digit revenue growth. However, profit conversion efficiency in its AI business remains constrained by high component costs. Additionally, the previously announced 2,500 job cuts (approximately 5% of the workforce) aim to save $350 million by FY27. While this optimizes the cost structure, it may temporarily impact morale and execution. The company's net debt ratio is expected to improve through accelerated share repurchases, but if AI orders fail to accelerate as anticipated, the FY26 free cash flow range could face further pressure. Long-term, this conservative guidance may help HPE avoid overcommitment risks and maintain financial resilience in the fiercely competitive AI infrastructure market. Management emphasizes that investments focused on high-margin segments will gradually enhance shareholder value. However, the current stock price correction undoubtedly intensifies internal pressure, compelling leadership to demonstrate integration progress in subsequent quarters.

More importantly, investors shifted their focus away from its growth narrative. Prior to the meeting, HPE's stock had already climbed 18% cumulatively, hitting a record high of $26.44, reflecting the market's fervor for the AI theme. However, disappointment dominated after the guidance release, with many traders viewing it as the collapse of the growth narrative. The after-hours decline widened to 10% at one point, though it later stabilized slightly. Nevertheless, the surge in overall trading volume indicated institutional selling pressure.

Some value investors see an opportunity here: Based on current valuations, the midpoint EPS for FY26 implies a P/E ratio of approximately 10.9x, representing a 17% compression from the trailing P/E of 13.2x—relatively attractive among tech stocks. Discussions on forums suggest that if Juniper's synergies accelerate, the $22-$23 price range could become an ideal sweet spot for adding positions. Conversely, aggressive bulls may pivot to competitors like Cisco or Dell, which face similar headwinds but offer more aggressive guidance. Overall, investor sentiment is divided: short-term traders lean toward reducing positions, while long-term holders may view pullbacks as a window to position for AI growth—especially considering the additional buyback program representing 10% of market cap.

The ripple effects of this incident across the entire industry cannot be overlooked. AI servers represent HPE's core growth track, but the shortage of GPUs—a critical component—directly resulted in "high demand failing to translate into actual revenue." AI system revenue for Q1 FY25 dropped from $1.5 billion in the previous quarter to $900 million. While demand fluctuations played a role, supply chain constraints remained a major driver. This contradiction prevented HPE from leveraging its AI business to offset weakness in other segments, ultimately leading to a downward revision of overall guidance.

In the AI infrastructure sector, HPE's conservative stance highlights the widespread challenges of supply chain bottlenecks and fluctuating demand. While multiple companies are ramping up investments in GPUs and edge computing, margin compression has become an industry pain point, as evidenced by Dell's recent performance. This could reshape the competitive landscape in the cloud and AI markets. Should HPE's guidance signal broader spending caution, order visibility for suppliers like Nvidia may be impacted, potentially triggering heightened volatility in upstream chip stocks.

On the other hand, the low single-digit growth forecast for network services reflects a slowdown in corporate digital transformation, which could drag down valuations across the entire technology sector. Analysts widely agree that the HPE incident serves as a reminder for investors to scrutinize the execution risks underlying AI hype, particularly as uncertain interest rate environments may prompt companies to adopt a more conservative approach to capital expenditures. However, should HPE successfully integrate Juniper and capture sovereign AI demand, this could spark a wave of industry M&A, prompting more players to strengthen their ecosystems through acquisitions. Overall, while this pullback is confined to HPE, it amplifies doubts about the sustainability of tech growth, potentially prompting investors to focus more on fundamentals rather than narrative-driven narratives within the AI theme.

Taking a comprehensive view, HPE's FY26 guidance, while anchored in long-term value, diverges from short-term market expectations. Data indicates the company is balancing growth and risk, but investors must closely monitor subsequent quarterly performance to determine whether this adjustment represents a temporary opportunity or a lasting warning.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.

- Valerie Archibald·2025-10-16The technical debt this company has amassed will result in mass “End of Support” notices across many products with overlapping capabilities .LikeReport

- Mortimer Arthur·2025-10-16Looks like the company will grow at a steady rate and cut costs at the same time. Sounds really bad to me........LikeReport

- AmandaViolet·2025-10-16Investors need to remain cautious; it seems the AI dream might be turning into a costly illusion.LikeReport