Interest rate hiking, Stocks peaking?

Last week, Federal Reserve officials, including Powell, began delivering speeches in a hawkish tone. They not only reiterated that "almost all" Fed officials support raising interest rates later this year at the June meeting, but also mentioned the possibility of two more rate hikes this year. The decision to pause rate hikes in June was aimed at slowing down the pace to a more cautious level.

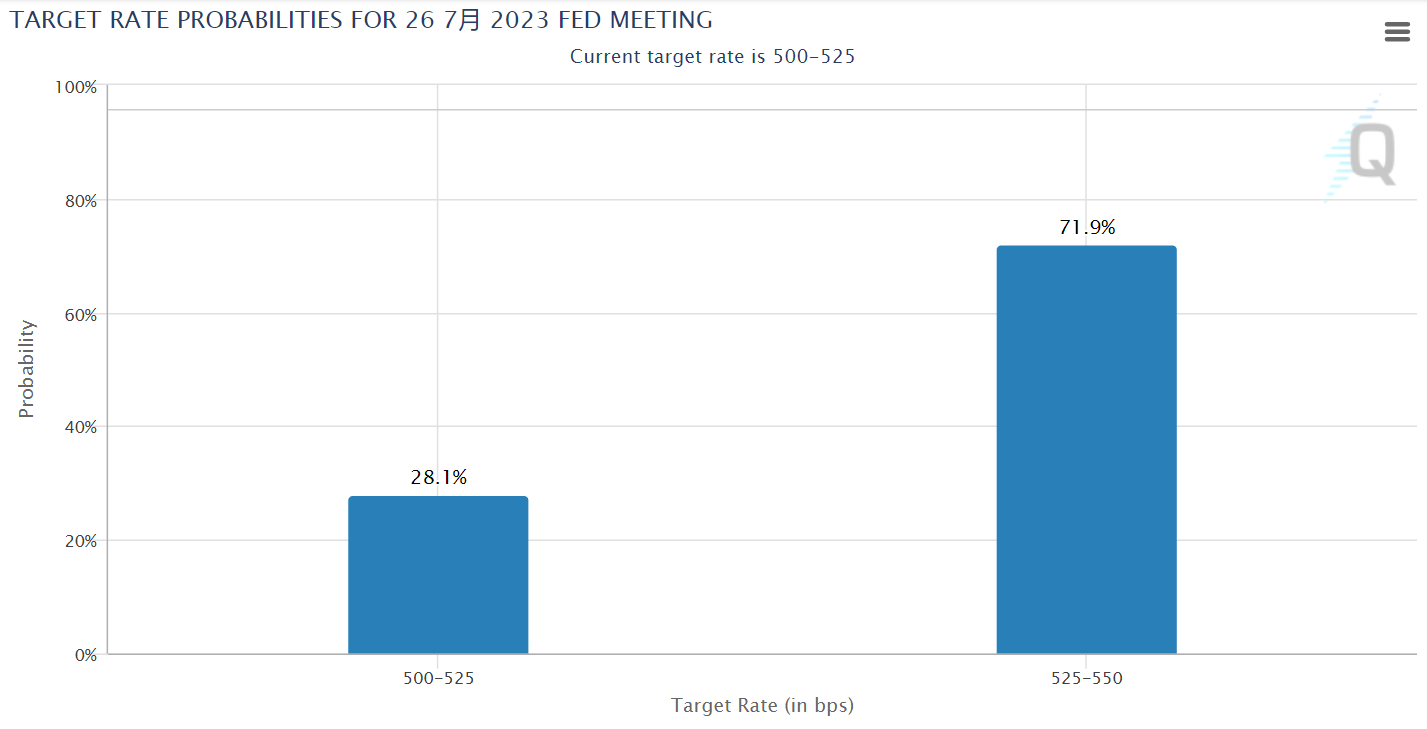

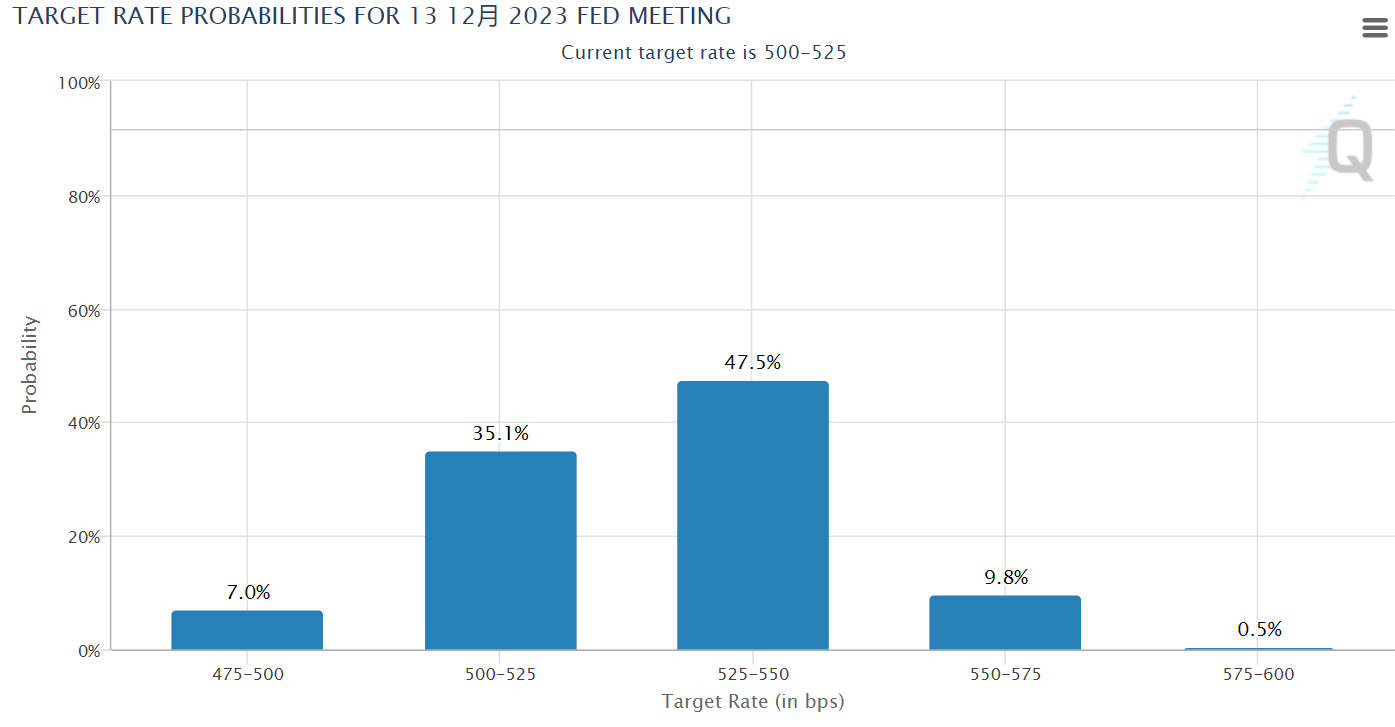

This outlook contrasts with the market's previous consensus, which anticipated only one rate hike and potential rate cuts later this year. According to CME's Fed Tool observation, the probability of a rate hike in July stands at 71%, and the probability of no rate cuts this year has risen to 47%, while the probability of a 25 basis point rate cut this year has decreased to 35%.

Furthermore, other central banks are also continuing their tightening processes.

Earlier this month, the Reserve Bank of Australia raised its key interest rate by 25 basis points to 4.1%, reaching its highest level since April 2012. Prior to this, Australia's CPI had been hovering around 7%, and the labor relations department increased the minimum wage for approximately one-fifth of the country's workers by 5.75%, adding inflationary pressure.

The European Central Bank (ECB) raised interest rates by 25 basis points as planned and hinted at another rate hike in July, bringing euro rates to their highest level since 2001. Additionally, the reinvestment of assets under the asset purchase program will no longer take place starting from July.

The Bank of England unexpectedly raised interest rates by 50 basis points, surpassing market expectations. This decision was primarily influenced by the UK's May CPI, which rose by 8.7% year-on-year, reaching its highest level since 1992.

The Swiss National Bank also raised interest rates by 25 basis points for the first time since March, citing a renewed rise in medium-term inflation pressures.

The Norwegian central bank increased its key policy rate by 50 basis points and indicated the possibility of another rate hike in August, raising the peak of the rate hike path.

Moreover, last week's release of the US June Markit Manufacturing PMI (6.3 vs. previous 48.4) continued its decline, while the Services PMI (54.1 vs. previous 54.9) experienced its first drop this year. Similarly, the eurozone's June Manufacturing PMI (43.6 vs. previous 44.8) decreased for the fifth consecutive month, and the Services PMI also experienced a significant decline (52.4 vs. previous 55.1). The cooling down of the services sector contributes to a "soft landing".

In terms of US stocks, the sustained strength led by technology stocks since March has become the biggest highlight in global markets. The AI frenzy has been a significant driving force behind the surge in leading technology companies.

In terms of valuation, despite the slowdown in earnings growth during the Q1 earnings season, the overall index is still at a high valuation. The Nasdaq Composite Index has a trailing twelve months (TTM) P/E ratio of 26.5 times, higher than the historical average of 22 times. Due to companies revising their profit targets, profit expectations for the second half of 2023 have been lowered by 12% compared to the peak in 2022. However, the valuation of large technology companies remains relatively favorable, with a current TTM P/E ratio of 21.3 times, lower than the historical average of 22.8 times.

From the market sentiment, investors are still enthusiastic about overbought technology companies. The implied volatility of major technology companies' options has also increased, and the Put/Call Ratio continues to decline, approaching the levels before the February decline this year. In addition, stocks like Nvidia (NVDA) and Tesla (TSLA), which have been rising for multiple days, have started to experience short-selling pressure and other phenomena, which to some extent pushes up stock prices.

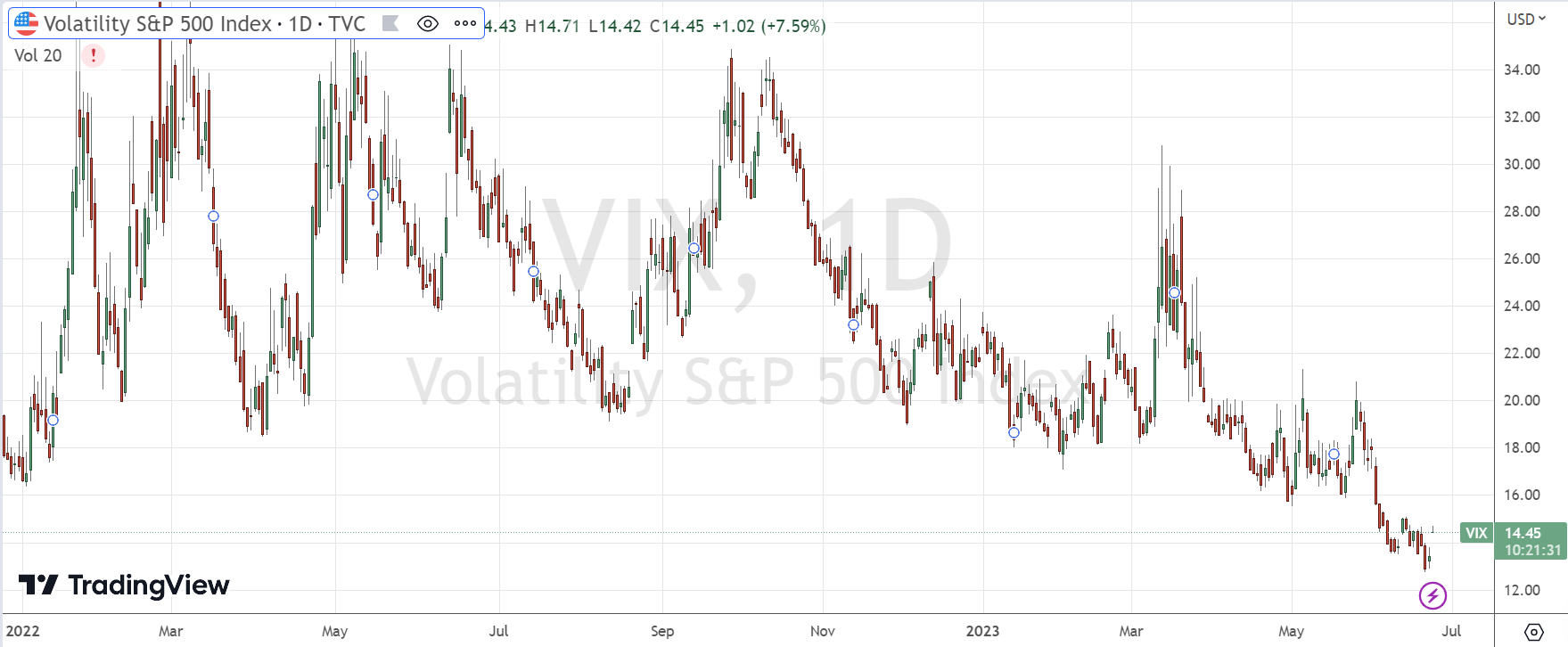

The S&P 500 Volatility Index (VIX), which measures the volatility of the S&P 500, rose to 14.6 on Friday after reaching a low point of 12.7 last week, but it remains at an extremely low level since the outbreak of the pandemic on February 14, 2020.

As we mentioned before, with the gradual increase in growth pressure in the second half of the year, the overall high valuation and low risk premium may increase the subsequent growth pressure and cause disturbances in stock prices, but it is not expected to lead to a trend reversal in technology stocks.

In the long term, the long-term returns of leading US tech stocks mainly come from improved performance (primarily revenue and profit growth) rather than valuation. Since mid-March this year, technology leaders have seen a 38% increase, with valuation contributing 25% and profit contributing 12%.

Therefore, under the current consensus of a "soft landing" in the United States, the growth pressure may gradually increase, and there may even be a slight pressure for recession. However, compared to the previously adjusted growth sectors, cyclical and value sectors face greater profit pressure. From this perspective, it is still preferable to allocate to growth stocks with abundant cash flow and promising prospects.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.

FFED is giving us more twists and turns than a soap opera. I don't know about you, but I'm on the edge of my seat, emotionally invested in this interest rate drama!

officials are like the weather forecasters of the stock market - constantly changing their tune, keeping us all guessing and questioning our investment strategies. Grab the popcorn, folks

Forget about rollercoasters and thrill rides, investing in stocks is becoming its own adrenaline-pumping adventure, thanks to the Federal Reserve's wild interest rate predictions!

brace yourself for the suspenseful saga of interest rates: will they hike, will they cut, or will they just make things interesting? Stay tuned

Well, looks like the Federal Reserve is on a rollercoaster ride, and we're all just hanging on for dear life! Buckle up, stockholder!"