Palantir: 7 Interesting Things From The Q2 2021 Earnings Call

Summary

- First, I briefly review the big news and highlights from PLTR's Q2 2021 business update.

- Second, I cover some of the details that are less well-known, including comments made by leadership on the earnings call.

- Third, dive into some important details about Alex Karp's compensation, including his insider selling activity; leadership had a response prepared.

- Lastly, I visit several metrics on my radar, including stock-based compensation, contribution margin, and deal value.

It's likely that you've already heard the news that Palantir (PLTR) just reported astrong Q2 2021. I'm certain there will be plenty of coverage of the empirical results, including the tremendous growth andincreased cash flow outlook.

Here, I'll just highlight those numbers then I'll turn to a few things that came up directly on the earnings call that surprised me.

First, revenue was up 49%, beating the estimates. it's notable that commercial revenue was up an eye-popping 90%, because it's an area that bears have complained about. This mostly squashes the idea that PLTR is only driven by secret government contracts.

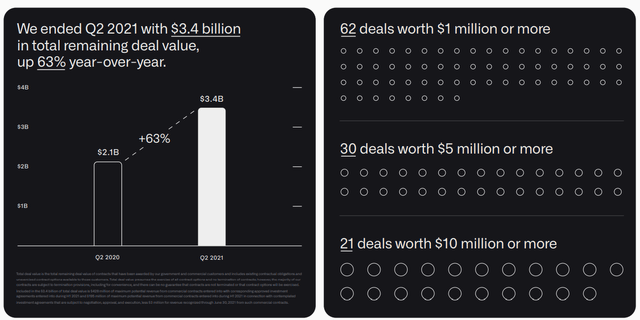

Second, PLTR closed a ton of deals in Q2. Specifically, they scored 62 deals worth $1 million or more. I like this view:

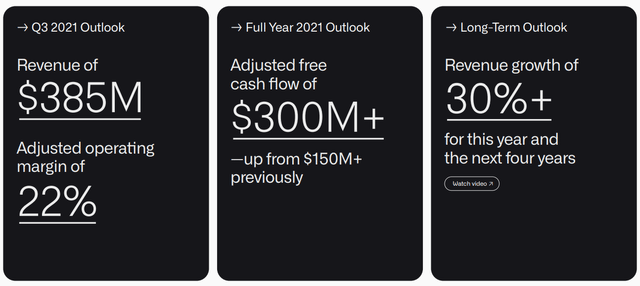

Third, it's looking like Q3 is going to work out fairly well. Sales are projected to be about $5 million great than consensus. And, as I've already mentioned, PLTR raised its free cash flow outlook. To be clear, the jump is rather big, going from greater than $150 million to now greater than $300 million.

I didn't see or hear much about changes in annual revenue growth, but one thing is crystal clear -I do not expect growth to slow down. And, per the presentation and earnings call, growth is expected at 30% or more this year, and then through 2025.

Interestingly, revenue grew by 49% in Q1 YoY, generating $341 between government and commercial. And now, in Q2, revenue grew by 49% YoY to $376 million. That's two quarters in a row at 49%. It's for this reason that I stick bywhat I previously wrote about PLTR sandbagging:

In other words, when we start with $800 million for 2021, it's pretty obvious that the 30% growth doesn't cut it. We cannot reach $4 billion by 2025 with "only" 30% growth. PLTR is perhapssandbaggingto keep expectations lower. It's hard to know for sure. It could also be that they expect faster growth in 2022 through 2025.

I'll have to dive in deeper in a future article to see exactly how current and future growth projections line up against the hard numbers that have come in. For now, my point is simply that they've set the bar at a reasonable albeit conservative level and seeing beats like this is not too shocking, but also encouraging.They're managing Wall Street and the analysts fairly well.

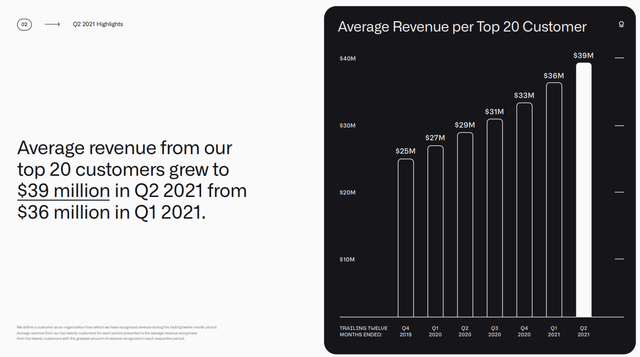

Fourth, in addition to new customer acquisition, the revenue dollar value for PLTR's top 20 customers continues to march upward.

Fifth,in Q1, we heard about "Day Zero" customers. Here's a taste:

We are seeing opportunities for companies to build their digital infrastructure around foundry from day zero, where they can shave years off their ramps and mountains of risk off their roadmaps by cost efficiently standing on the shoulders of 15 years and more than $2 billion of R&D. And we see this as the first salvo in expanding distribution of foundry to broader markets and a broader set of customers.

In Q2, PLTR leadership continued to push this theme, highlighting Roivant, Celularity and Wejo, for example. The idea is to get these companies using Foundry while they are just getting started, or otherwise very small. They're treating Foundry as the "operating system" of these businesses.

Supporting this thrust,PLTR added another 60 sales hires. If I recall correctly, they hired about 50 sales people in Q1, so they are steadily adding headcount in sales and marketing, without going gangbusters. That said, their pipeline is accelerating, with active commercial pilots up 26% since the end of April.

Sixth, I heard leadership quickly say that they have paid off what they owed, and thatPLTR is now debt free. In a future article, I'll have to do a deeper dive, but I wanted to report it here since I have an affinity for extremely strong balance sheets. It's possible I didn't understand the comment on the call, but I'm pretty sure that I've got it right. I reviewed the Q2 2021 business presentation but didn't see any notes on this so I'll have to revisit this at a later point. But again, I think I've got it right, and it's great news.

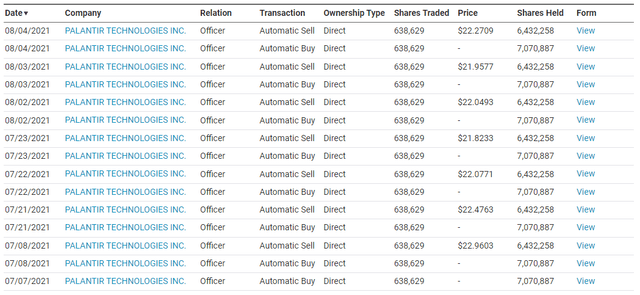

Lastly, there was a question about Alex Karp's executive compensation, and specifically about the relentless insider selling. Before I get to that, here's some quick backgroundreported by CNBC back in April 2021:

Palantir CEO Alex Karp earned compensation worth about $1.1 billion in 2020, primarily through equity awards granted shortly before his software company went public.

In a proxy filing on Thursday, Palantir said the bulk of Karp’s pay was tied to options worth $797.9 million, with another $296.4 million for stock awards. The outsized package is the result of an equity incentive plan agreed upon last year, giving Karp 141 million options that begin vesting in August 2021. Each quarter, 2.5 percent of the equity will vest.

Now, here's just a quick peek about what that selling looks like:

Karp's salary is just over $1 million, which isn't too bad, but it's also not crazy. Clearly, PLTR stock and options are fueling his incredible compensation package. This is a bit frustrating to track, however, when the options vest, get exercised and then sold there are also tremendous taxes to pay. So, in part, Karp is necessarily working through the process of exercising long-term options, while handling tax obligations on a rational schedule.

Again, all of this is to say two things. Karp's made a ton of money but at the same time, he hasn't given up on PLTR. His selling doesn't say anything substantial about PLTR's future, in my opinion. It's his own mind-boggling personal finance process, that's on display in public as the CEO of PLTR.

Summarizing everything, PLTR had a strong quarter in Q3 2021 looks like it should be strong as well:

I'll be looking for a deceleration in stock-based compensation expenses. I'll be looking for strong growth in both government and commercial. I'll be looking at Q2 growth, given the high bar set with49% growth in Q1 2021. I'll be looking at total remaining deal value, which was about $2.8 billion at the end of Q1 (and up 40% YoY). I am expecting contribution margin to remain high, and hopefully over 60% in Q2.

- Stock based compensation increased. I'll have to review this more closely in a future article. It's still a major thorn in my side. Virtually every chart has this phrase in the footnotes:"...excludes stock-based compensation and related employer payroll taxes."It's my #1 issue with PLTR.

- Q2 growth was excellent, as I've pointed out. Both government and commercial did well. And, long-term customers keep sticking and spending, more and more. I like what I'm seeing in terms of growth.

- Deal value increased 63% to $3.4 billion. So, they did very well in that department. That gives us a glimpse into future sales and related growth.

- Lastly, contribution margin didn't hit my big goal of 60%, but it still improved strongly to 58% in Q2 2021 from 55% in Q2 2020.

Source: Seeking Alpha

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.

- AlanGoh·2021-08-14Thank you very much for summarising the earning into a well written report (:LikeReport

- Frosty4ever·2021-08-14$Palantir Technologies Inc.(PLTR)$ are executing very well.LikeReport

- jtigger·2021-08-17Thanks for highlighting all theseLikeReport

- yattreblif·2021-08-15nice reportLikeReport

- coolstuff·2021-08-13excellent analysis!LikeReport