United Hampshire US REIT Review @ 6 March 2022

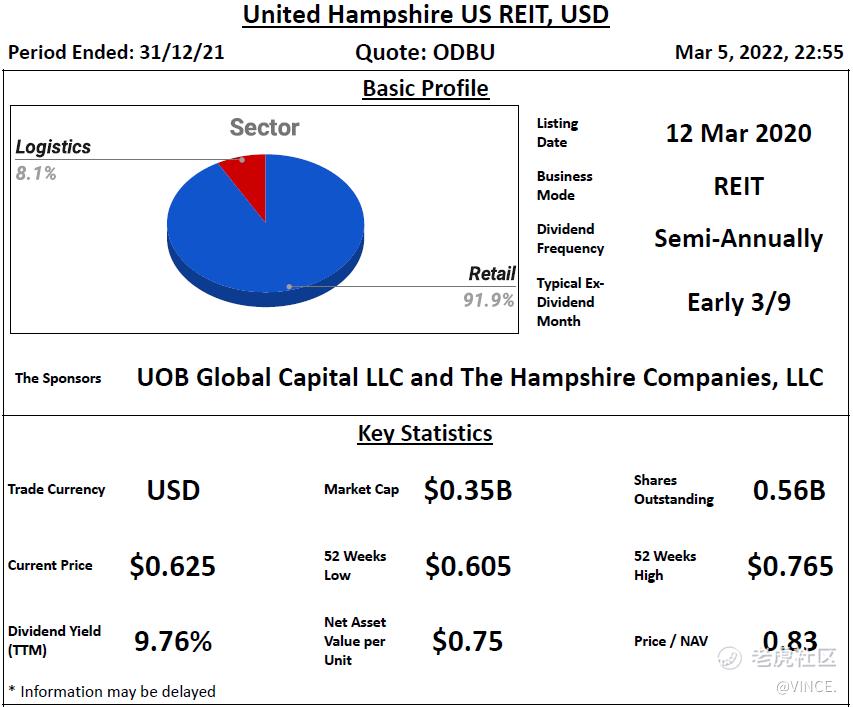

Basic Profile & Key Statistics

United Hampshire US REIT (UHREIT) invests in Retail and Logistics (self-storage) properties which currently owns 24 properties in U.S.

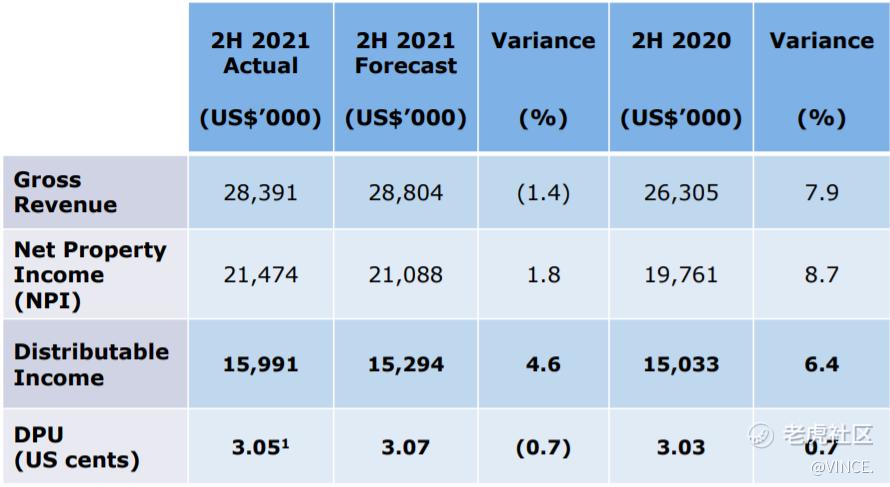

Performance Highlight

As compared to 2H 2020, gross revenue, NPI, distributable income and DPU have improved YoY due to higher contribution from self-storage properties as well as newly acquired properties.

Tenant Sales

Tenant sales has improved YoY for the 4 anchor tenants.

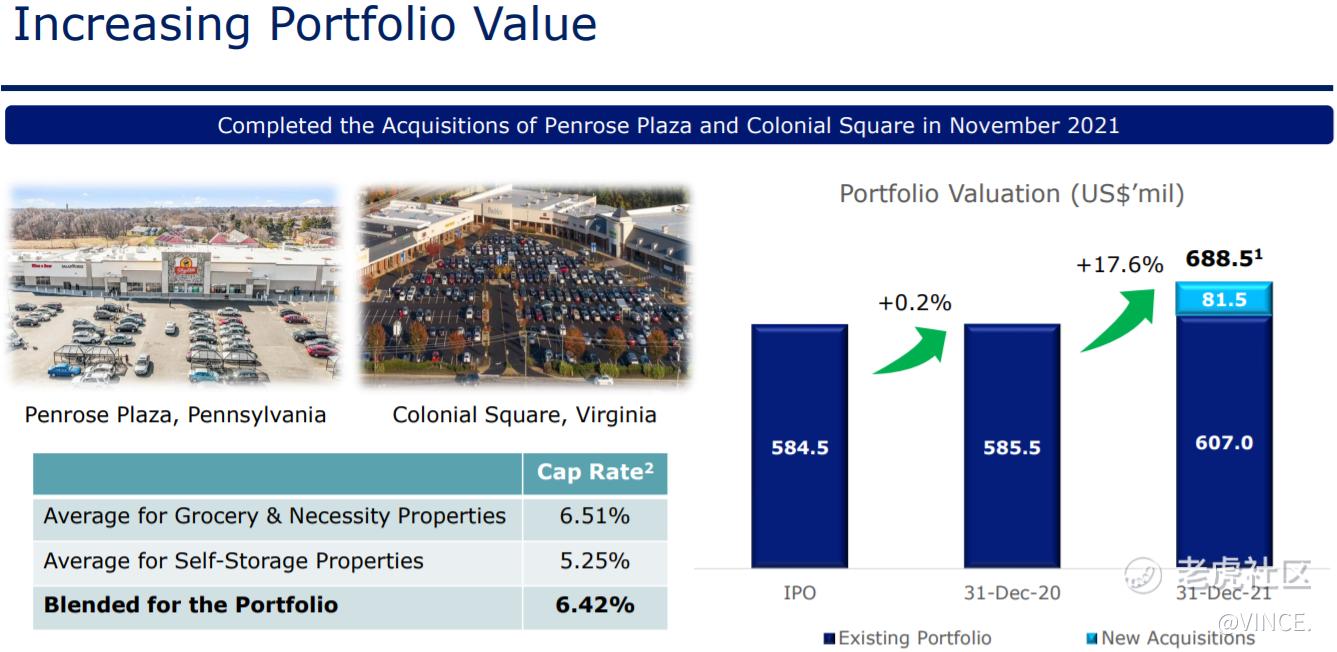

Acquisition

In November 2021, UHREIT has completed the acquisition of Penrose Plaza and Colonial Square.

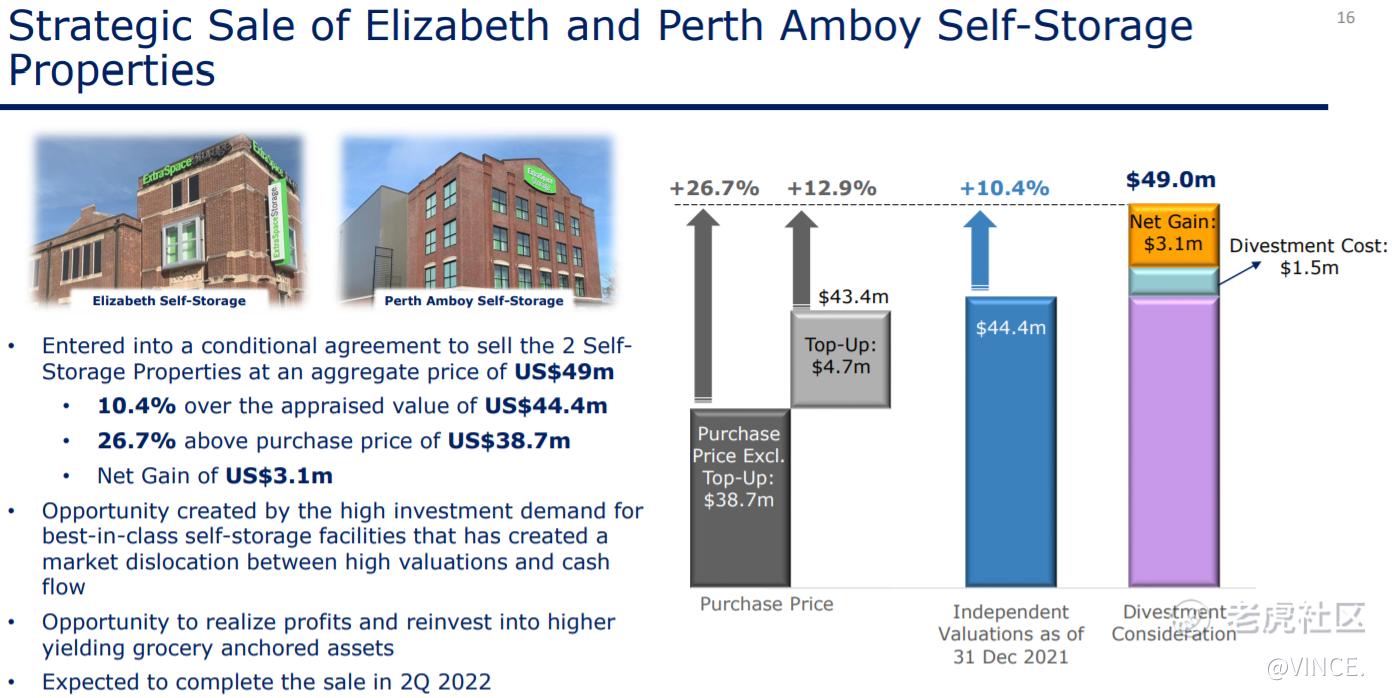

Divestment

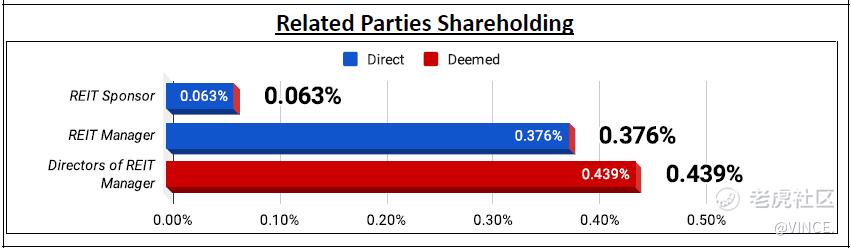

UHREIT has announced for proposed divestment for Elizabeth and Perth Amboy self-storage properties. The divestment gain is at US$ 3.1 mil, which is around 7% over valuation. This divestment is expected to be complete by 2Q 2022.Related Parties Shareholding

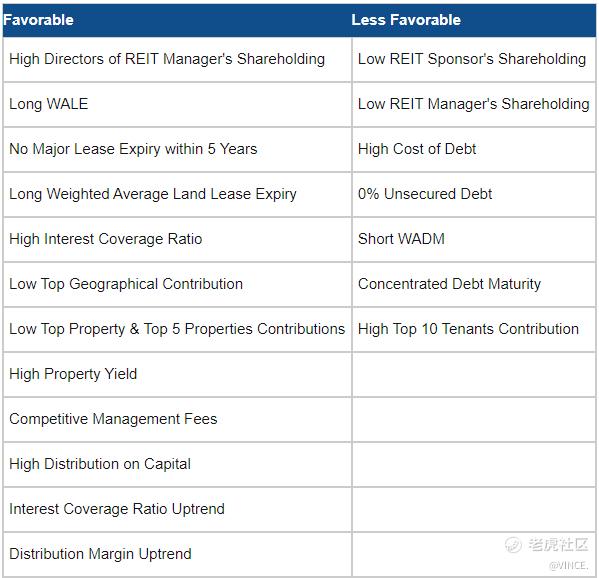

- REIT sponsor's shareholding is low at 0.063%

- REIT manager's shareholding is low at 0.376%

- Directors of REIT manager's shareholding is high at 0.439%

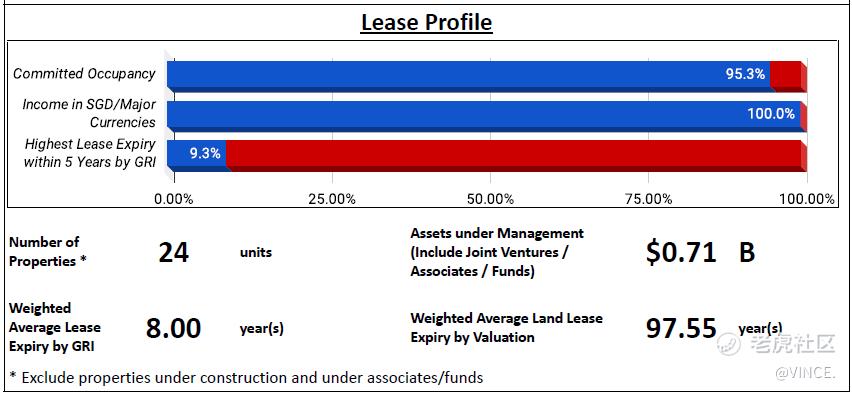

Lease Profile

- Occupancy is slightly high at 95.3%

- WALE is long at 8 years

- Highest lease expiry within 5 years is low at 9.3% which falls in 2024

- Weighted average land lease expiry is long at 97.55 years

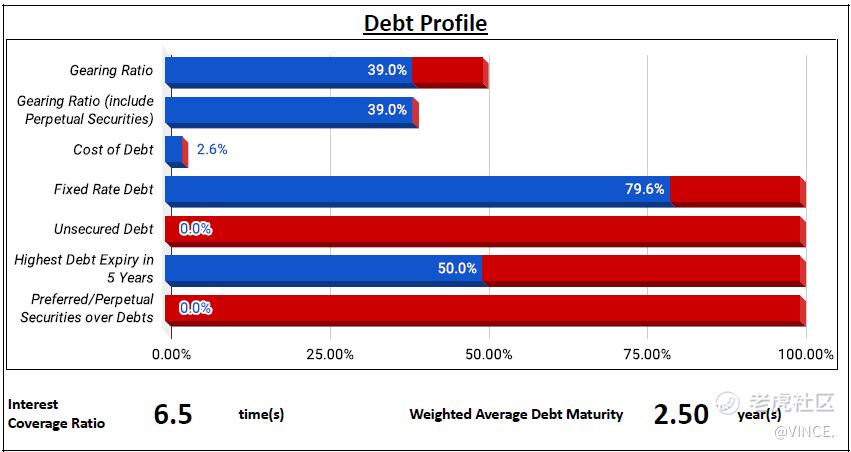

Debt Profile

- Gearing ratio is moderate at 39%

- Cost of debt is high at 2.63%

- Fixed rate debt % is slightly high at 79.6%

- All debts are secured debts

- WADM is short at 2.5 years

- Highest debt maturity within 5 years is high at 50%, which falls in 2024

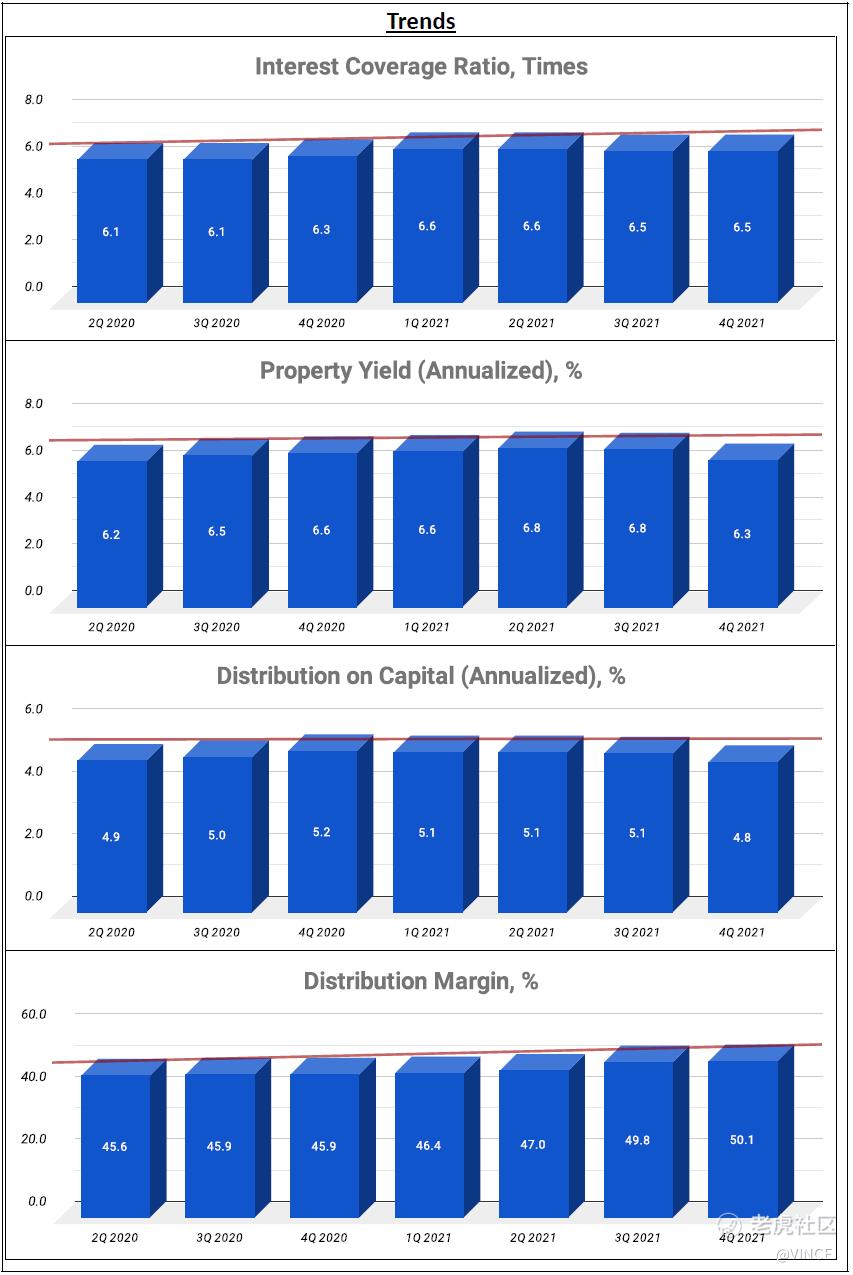

- Interest coverage ratio is high at 6.5 times

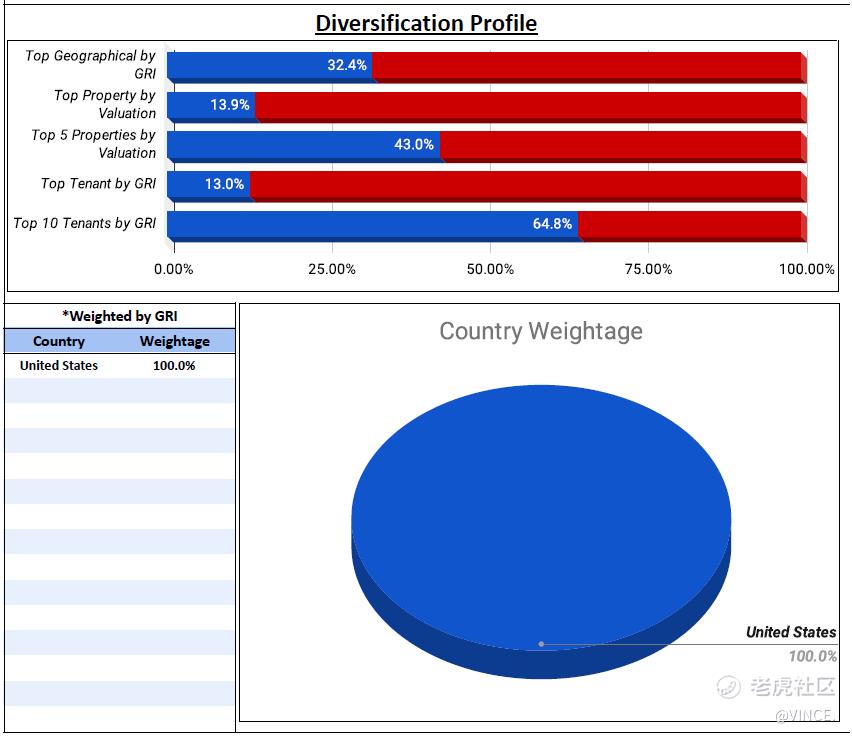

Diversification Profile

- Top geographical contribution is low at 32.4%

- Top property contribution is low at 13.9%

- Top 5 properties contribution is low at 43%

- Top tenant contribution is moderate at 13%

- Top 10 tenants contribution is high at 64.8%

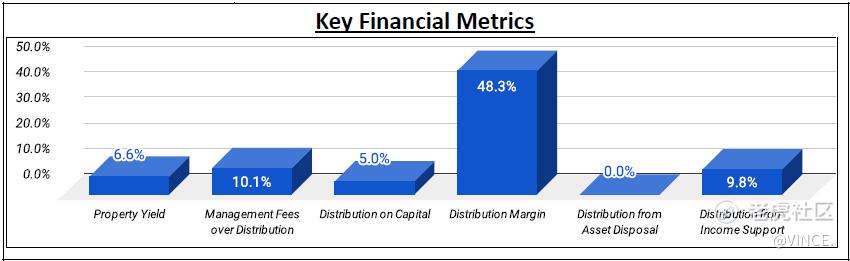

Key Financial Metrics

- Property yield is high at 6.6%

- Management fees over distribution is low at 10.1% in which unitholders receive US$ 9.90 for every dollar paid

- Distribution on capital is high at 5%

- Distribution margin is moderate at 48.3%

- 9.8% of the TTM DPU is from income support

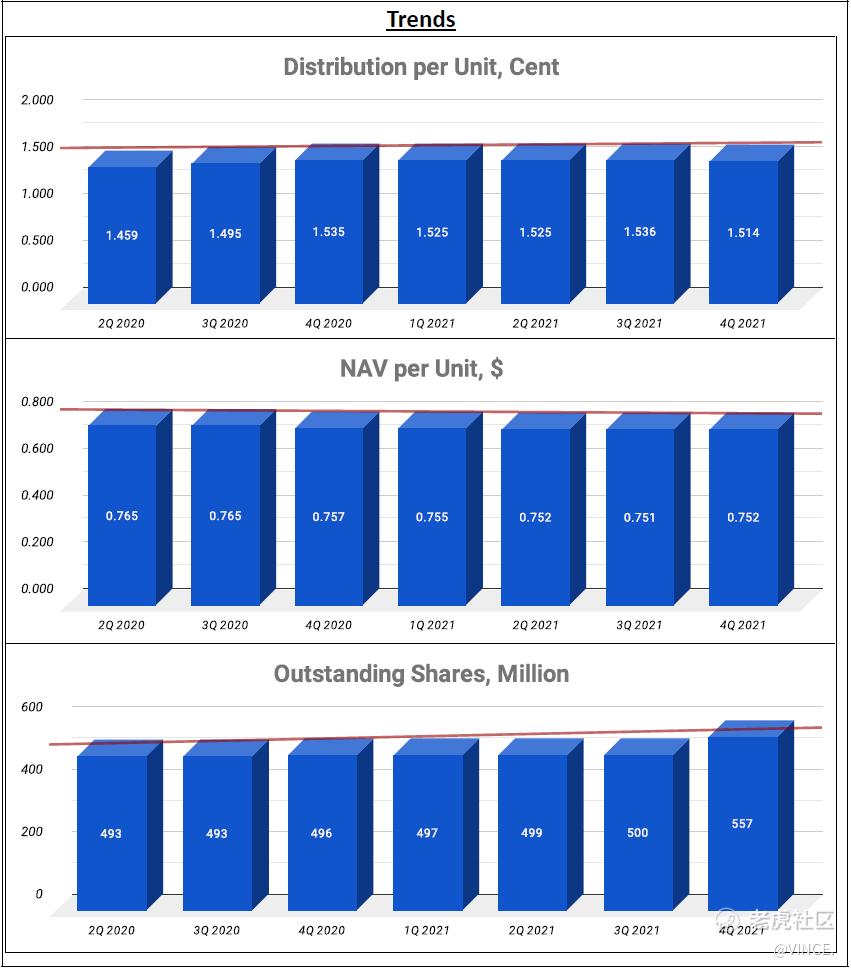

Trends

- Uptrend - Interest Coverage Ratio, Distribution Margin

- Slight Uptrend - Property Yield

- Flat - DPU, NAV per Unit, Distribution on Capital

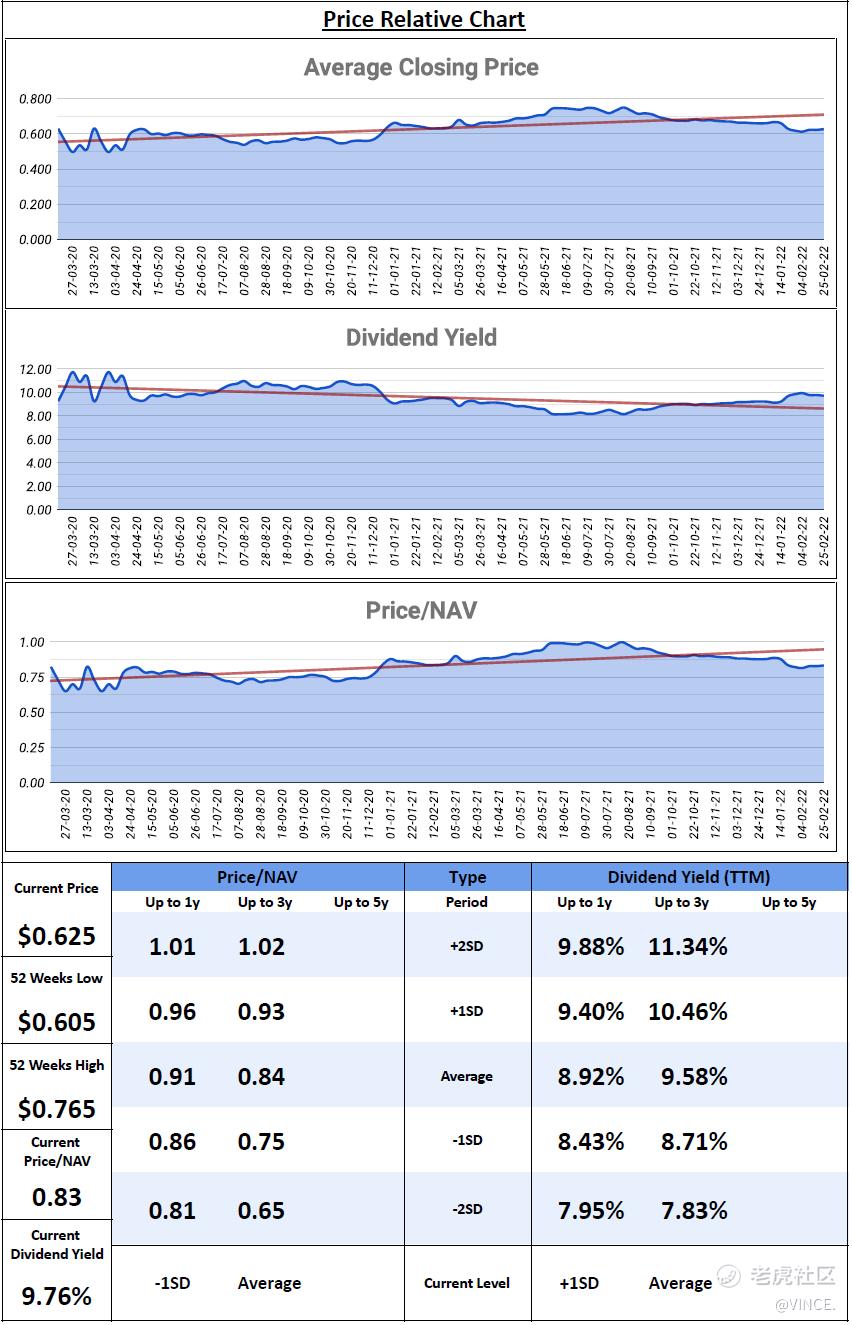

Relative Valuation

- P/NAV - Below -1SD for 1y, Average for 3y

- Dividend Yield - Above +1SD for 1y, Average for 3y

Author's Opinion

The full half yearly contribution from the 2 newly acquired properties would improve UHREIT performance moving forward. However, it would be offset by loss of income from the divestment of Elizabeth and Perth Amboy self-storage properties which is target to complete by 2Q 2022. Let's see later whether managements would acquire any property after the divestment.

You could also refer below for more information:

SREITs Dashboard @https://www.reit-tirement.com/p/sreits-dashboard.html- Detailed information on individual Singapore REIT

SREITs Data @https://www.reit-tirement.com/p/sreit-data.html- Overview and Detail of Singapore REIT

REIT Analysis @https://www.reit-tirement.com/p/reits-analysis.html- List of previous REIT analysis posts

And you could join the following to support my work:

REIT-TIREMENT Facebook Page @https://www.facebook.com/reit.tirement- Support by liking my Facebook Page

*Disclaimer: Materials in this blog are based on my research and opinion which I don't guarantee accuracy, completeness, and reliability. It should not be taken as financial advice or a statement of fact. I shall not be held liable for errors, omissions and loss or damage as a result of the use of the material in this blog. Under no circumstances does the information presented on this blog represent a buy, sell, or hold recommendation on any security, please always do your own due diligence before any decision is made.use of the material in this blog. Under no circumstances does the information presented on this blog represent a buy, sell, or hold recommendation on any security, please always do your own due diligence before any decision is made.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.

- frosti·2022-03-07Boosting property investment is also a conventional way to stimulate the economy10Report

- bouncyo·2022-03-06Thank you very much for your information, which will be very useful to me.8Report

- Oldhead·2022-03-08Has higher yield compared to other Reits of US properties but it seems more riskier fundamentals wise.4Report

- quiettt·2022-03-07I don't think it's wise to overinvest in real estate.2Report

- RedpillBluep·2022-03-07Thanks for the information, appreciated. [Grin]2Report

- CKF68·2022-03-08Well Written article. Good sharing1Report

- Pluto891·2022-03-07Retail and Malls might be a dying breed1Report

- adeley·2022-03-07us has too much land though1Report

- Olegarki·2022-03-08Like back please…thanks4Report

- AnnieReis·2022-03-08Thanks for sharing 👍3Report

- 太好多多·2022-03-08好好好保障3Report

- TKY1978·2022-03-08Trade with care1Report

- makingrich·2022-03-07thanks for the insight1Report

- luckyone·2022-03-07looks like an interesting REIT1Report

- SL828·2022-03-07Into watchlist..1Report

- MandyLow118·2022-03-07nice..tq for sharing..1Report

- Mohammad Haz·2022-03-08Great ariticle, would you like to share it?1Report

- SnailWalker·2022-03-08[Miser] [Miser]1Report

- kaido·2022-03-08like pls1Report

- Cheahkim·2022-03-08好LikeReport