Schrodinger's nuclear bomb suggests that near-term risk skews deeply negative

“Don’t wait for the last judgement. It comes every day.” – Albert Camus

Key Points:

-The Twin Sessions set ambitious growth target and fiscal expansion. But China’s macro leverage will likely stay steady, and the onshore market will stagnate.

-Every oil crisis or oil price surge is followed by a US recession.

-RMB strength explains the divergence between on- and off-shore markets in 2021. But the Hang Seng has outperformed CSI300 YTD by 2x.

-Schrödinger’s nuclear bomb suggests that near-term risk skews deeply negative.

The "Twin Sessions"

The all-important “Twin Sessions” are still proceeding. Many were surprised by the 5.5% GDP growth target set for 2022, but with a lower budget deficit than 2021. It is at the top end of consensus forecast, and well above the IMF’s estimate of below 5%. The sessions have set an ambitious target amid historic oil and bond volatility globally. No doubt it will be a challenging environment, especially in the near term. In times like this, it pays to set a target that conveys the determination to progress in yet another trying year.

Note that 2022 will be another record year of university graduates joining the workforce. Growth of 5% or above will be necessary to keep all the young and eager faces employed. Further, even though the fiscal deficit seems modest, a lot of the fiscal spending will come from central government expenditure, surplus from last year and retained earnings submitted by SOEs in recent years. All these budgetary items amount to around 1% of extra budget deficit, more than compensating the seemingly lower fiscal deficit this year.

But there weren’t specific policy statements on consumption. Neither on the property sector. Even so, there have been positive developments recently. Country Garden was approved to issue medium-term notes of RMB5bn; Shanghai, an important signpost, lowered its mortgage interest rate, and Zhengzhou lowered the down payment requirements for mortgages and margin requirements for land auctions. More positive news will come for the property sector on a city-by-city basis. Yet, as discussed in our previous notes, it has already been written in the Shanghai property index (Please refer to our report“The PBoC Articulates its Policy Stance”on 2022-01-19).

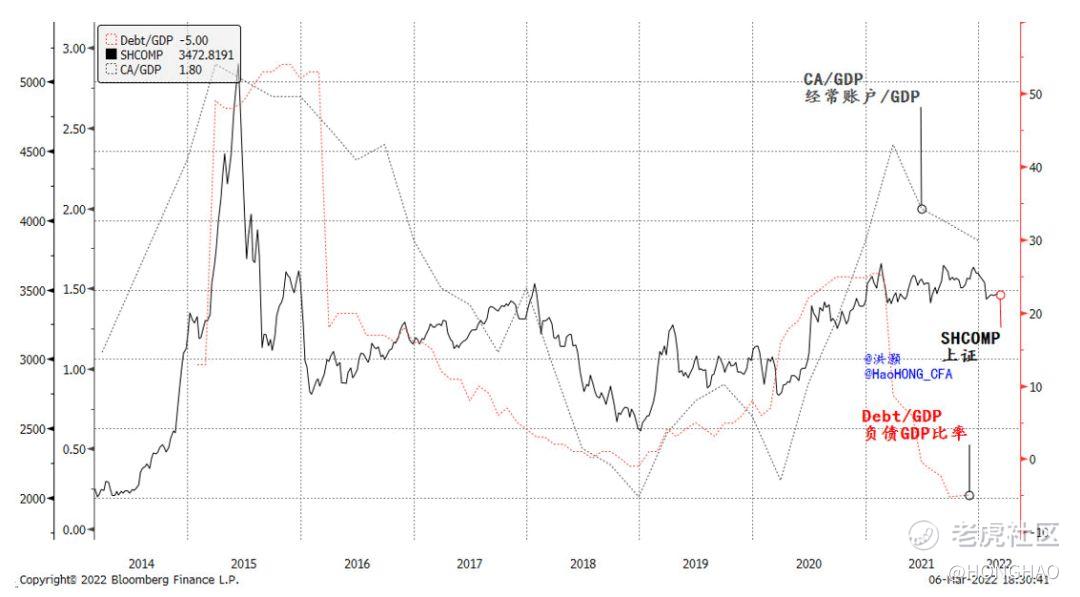

As such, money and credit growth is unlikely to be as strong as consensus hopes, given the strong fiscal response embedded in the government work report. Since 2014, China has undergone two important periods of leveraging, one in 2015 and then another in 2019, as measured by the change in China’s debt-to-GDP ratio (Figure 1). The first leveraging campaign ended with a bang during the summer of 2015 when the stock market bubble burst. The second was in response to the trade war in 2018, and peaked in February 2021, together with the onshore stock market.

Given the outlook of China’s money and credit growth, its macro leverage ratio will likely be steady in 2022. That is, credit growth will be commensurate with the economy, keeping the macro leverage largely steady. As macro leverage is closely correlated with the stock market index, the onshore stock market will unlikely get a boost from macro leverage.

This observation of macro leverage is also consistent with our framework of forecasting 2022, by examining how the changes in macro accounts correspond to stock market performance. As China’s exports slow to its normal rate of growth in 2022, current account surplus as a percentage of GDP will fall. Such a decline in the surplus ratio will be consistent with a change in China’s role as a global production and export center since the onset of the pandemic. Slower foreign consumption (i.e. exports) but slightly improving domestic consumption will mean peaked surplus and a steady macro leverage ratio. Hence, the onshore stock market is unlikely to be helped by this macro shift (Figure 1).

Figure 1: China will likely pause deleveraging for now, but no significant re-leveraging, either; a significant divergence between the Shanghai Composite and China’s debt/GDP

The New Oil Crisis

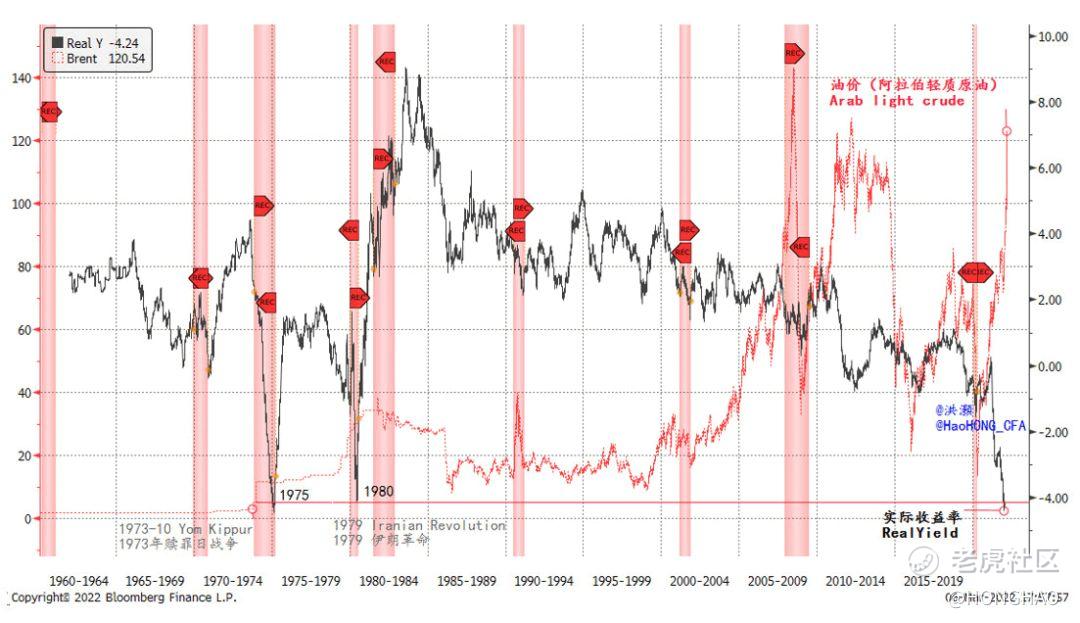

The macro changes are not the only factor affecting the market. Constant headline risks from the Russia-Ukraine war front have jolted the global markets. Oil price has surged to US$120 per barrel, and the Bloomberg Commodity Index is making all-time highs (Figure 2). We have been recommending allocation to the energy and commodity sectors since we published our 2022 outlook last November. But the strength in oil, spurred by intensifying geopolitical conflicts, continues to dumbfound pundits. Indeed, oil price has been surging with such astounding momentum that we could only catch up by updating our real-name verified Weibo, China’s Twitter equivalent.

We have also been warning of the biggest risk that the global economy is facing – the Fed is obliged to tighten just as the US economic growth starts to slow. As oil price soars, the real yield on the US 10-year has plunged to its historical lows, equivalent to the bottoms we witnessed in the two oil crises in the 1970s and early 1980s (Figure 2). And every time when oil price surged with such breakneck momentum to such great heights, a US recession ensued. Roaring oil price piles on inflationary pressure, increases macro uncertainties and binds the Fed’s policy choices – especially at this juncture. As such, global markets will continue to be volatile in the near term, as a struggling US market will be felt across the globe.

Figure 2: Every oil crisis or oil price surge is followed by a US recession

What To Do With Market?

The volatility in the US market is clearly felt in Hong Kong. It has yielded back all its gain YTD. Amid the tremendous turbulence, many have failed to recognize that Hong Kong continues to be the best-preforming major index globally, and its loss so far in 2022 has been half the size of CSI300. Many market pundits claim that the onshore market is a risk haven, but forget that, for an onshore investor, s/he does not really have any overseas investments that need shelter.

Even though the onshore market seems to be less volatile, its role in global diversification is limited as a market in which cross-border capital flows are still closely monitored, although they will increase over time. As such, an onshore investor’s risk profile has not changed if s/he has only position in the onshore market, and will still lose out as the overseas volatility ripples across.

Besides this, what other factors would have contributed to the on/offshore market divergence?

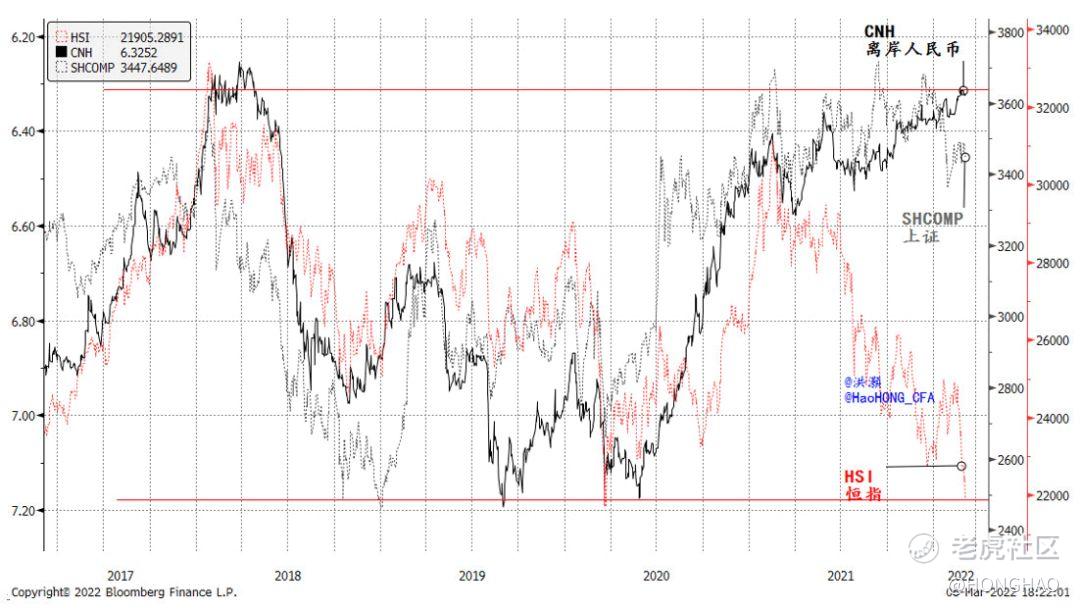

The offshore RMB has been closely correlated with the on/offshore market performance in recent years. Since 2021, the RMB has strengthened to one of its highest levels, concurrent with an elevated Shanghai Composite. At the same time, the Hang Seng Index seems to have decoupled and plunged to its nadir (Figure 3). In a normal market environment before the pandemic, a strong RMB is a reflection of strong exports and thus strong current account. It is a sign of abundant domestic liquidity.

Yet, at the same time, the offshore liquidity condition has been tightening, as the HKMA began to shrink its balance sheet since early 2021. It is a determinant force pressuring the Hong Kong market, trumping the positive effect on the Hang Seng from a strong RMB. And thus the divergence between on/offshore China markets. Going forward, a weakening RMB due to slowing exports will pressure the onshore market, if history is a guide. But less so for the offshore market such as Hong Kong, if the HKMA is done with its balance sheet tightening. Even so, Hong Kong will continue to feel the pressure from other global elements, namely the Fed tightening and the Ukraine War.

Figure 3: The strength in RMB explains the divergence between on/offshore markets

Schrodinger's nuclear bombConclusion

In sum, China’s “Twin Sessions” have set an ambitious growth target for 2022, and budgetary details suggest that fiscal spending will carry most of the load. While there is little articulation on property policy, the sector is starting to loosen on a case-by-case, city-by-city basis. But it is mostly demand-side maneuvers, and the three-red-lines remain hanging over the property developers. As China and the West start to redefine their export/production and import/consumption relationship this year, exports will slow, current account will peak, the RMB will weaken somewhat, and the onshore market will stagnate.

Meanwhile, oil price is surging with momentum seen only in the two oil crises in the 1970s and early 1980s. History suggests that every oil crisis or oil price surge has been followed by a US recession. This time it will not be different. The biggest macro risk is that the Fed is obliged to tighten its policy as the US economy, as well as that of the globe, starts to slow. Real yield on the US 10-year has plunged to a level seen only in the previous two oil crises. Such depressed yield on a safe-haven asset hints at an environment that will likely go into risk-aversion shock in the near term. There will be hardly anywhere to run, except for oil, gold and commodities.

The historic strength in RMB explains the divergence between on/offshore market performances. As the RMB’s strength weakens, the onshore market will no longer get a boost. While we continue to believe that Hong Kong offers deep allocation value at its recent levels (“This Christmas, Hong Kong in Deep Value”, 2021-12-23), not everyone can stomach the potential market upheaval, should the Ukraine War intensify further.

The prospects of a nuclear war cannot be easily dismissed. It is like Schrödinger’s nuclear bomb – it is now both there and not there. If so, the payoff from wading into the currents today is deeply and negatively skewed in the near term. But the world eventually bounced back after Hiroshima and Nagasaki. For sure, the entry point today will look wise if we one day look back upon today’s decision in the long term. But to see the long term, we must survive the short term. And in the long term, we are all dead.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.

Sishsoaosidd