15 Cheap Growth Stocks Amid the Volatility

Growth stocks are now broadly undervalued and the overall market now looks fairly priced.

Dave Sekera, CFA Feb 28, 2022

Meta Platforms Inc $(FB)$, Alphabet Inc $(GOOG)$,Teladoc Health Inc $(TDOC)$,Twilio Inc $(TWLO)$,Okta Inc $(OKTA)$,DocuSign Inc $(DOCU)$,Uber Technologies Inc $(UBER)$, Fastly Inc $(FSLY)$, Palantir Technologies Inc $(PLTR)$, Amazon.com Inc $(AMZN)$.

Equity volatility has roiled the markets over the past week as Russia invaded the Ukraine and in the process, added a new level of uncertainty about inflation and the direction of the global economy.

This geopolitical crisis came after U.S. stocks had already been sent broadly lower starting in January as investors ramped up expectations for the pace of Federal Reserve tightening in 2022 as the central bank aims to fight stubbornly high inflation.

The result is that U.S. stocks have gone from broadly overpriced to fairly valued, based on valuation estimates for stocks covered by Morningstar’s equity analysts.

The most notable change has been in growth stocks. Shares of the fastest-growing companies had also tended to be the most overvalued. But now that category has become undervalued, and is even more attractive than value stocks.

Stocks on the undervalued list include some of the market’s biggest names, such as Amazon.com $(AMZN)$, Uber UBER and Alphabet GOOGL, along with cybersecurity company Okta $(OKTA)$, Palantir$(PLTR)$--which provides intelligence software to governments--and Boston Beer $(SAM)$.

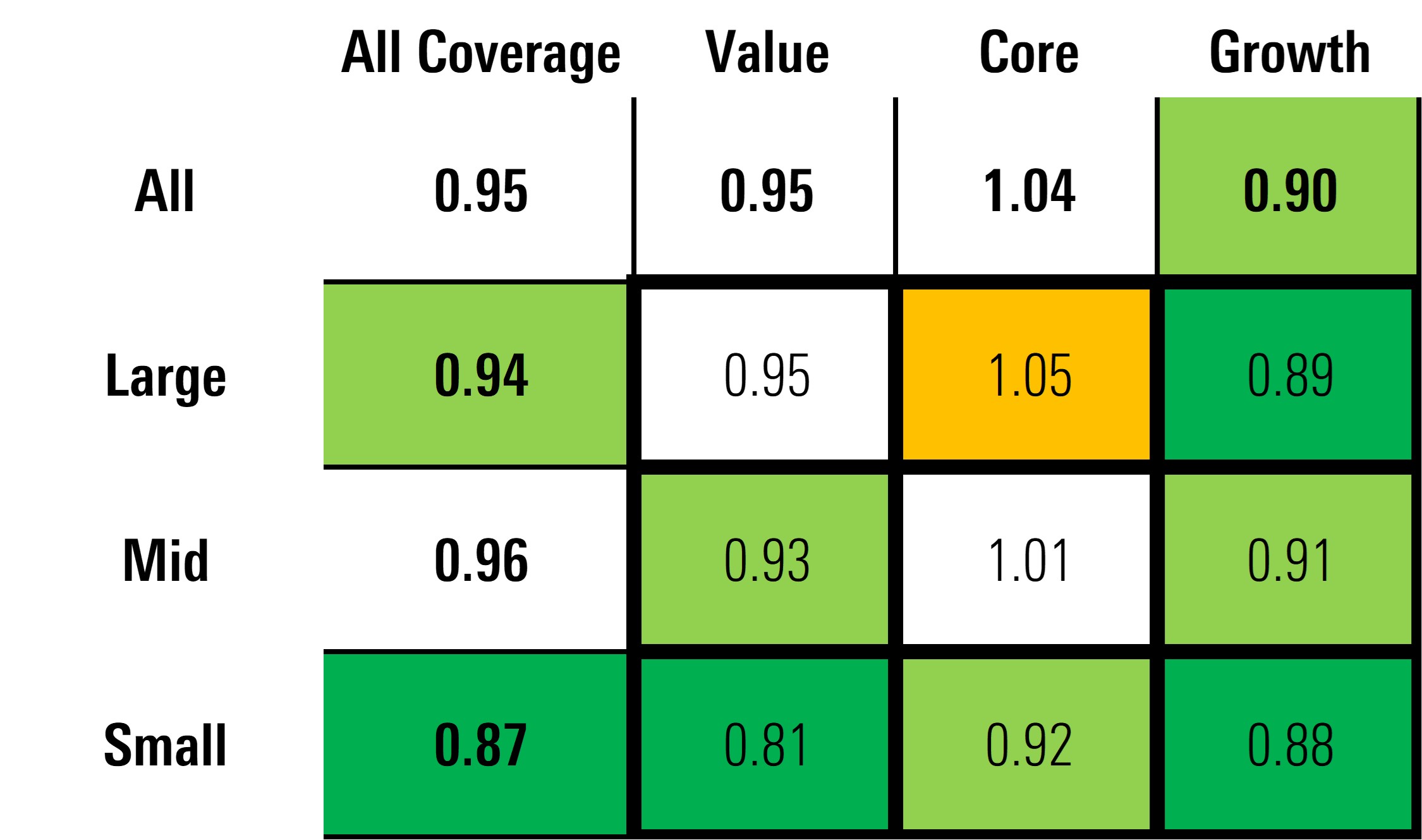

U.S. Equity Market Valuation

We hadcautioned investorsthat the market was overvalued coming into the year, and equities had been on a downward trend through mid-February, even before the Russian invasion.

As of Feb. 25, the composite of the price to fair value of the stocks under our equity research coverage has dropped to 0.95--the bottom of the range that we consider fair value.

Through the market turmoil, the value category has remained largely unchanged. However, the morningstar US Value Index has fallen 15.44% year to date through Feb. 25 and the Morningstar US Core Index has dropped 8.51%. The core category was the most overvalued coming into the year, and even following this pullback remains overvalued. We continue to think value stocks remain attractive and will have good economic tailwinds behind them through the year. Growth stocks, however, have dropped well into the undervalued territory.

The market price to fair value is a composite derived from the intrinsic valuations as determined by our equity research team of the stocks we cover that trade on US exchanges. Values > 1 are considered overvalued and < 1 are undervalued.

Undervalued Growth Stocks

We think Uber is one of the most direct and leveraged plays on our expectations for consumer activity to normalize in 2022 as the pandemic recedes and spending reverts back towards its historical levels for services and less on capital goods. We especially see a lot of pent-up demand for travel, dining out, and public events, all of which will help to bolster the ride-sharing business. We believe Uber has a 30% global market share and will be the leader in our estimated $452 billion total addressable ride-sharing markets (excluding China) by 2024.

Meta Platforms $(FB)$ stock was pummeled after it reported fourth-quarter earnings. The stock is now down 37% year-to-date and is trading at about half of our fair value estimate. However, we think the market has over-reacted to the short-term pressures that have arisen from the changes Apple has made regarding its privacy. In our view, we still consider Facebook and its other platforms to be some of the highest quality platforms for digital advertising, which still in the early stages of secular growth trends. We think Meta will be able to find additional means of targeting its advertising and demonstrating its value to advertisers.

Amazon$(AMZN)$ is down 8% year-to-date and is now trading at a 25% discount to our fair value. The stock soared in early 2020 as consumers shifted their purchasing habits to online, but the stock has traded in a relatively narrow range since. Compared to the extremely rapid rise in comparable sales in 2020, the growth rate has slowed in 2021. However, we think the market is overly concerned about this near-term slowdown in sales growth. In our valuation, we think the market is underestimating the value of Amazon’s advertising business as well as its Amazon Web Services.

Alphabet $(GOOGL)$ is down 7% year-to-date and is now trading at almost a 25% discount to our fair value. Similar to Meta Platforms, we think the market is underestimating the value of advertising on its platforms as secular growth trends in digital advertising continues. We also think the market is underestimating advertising revenue potential of YouTube and forecast that Google will continueto gain traction in the cloud market.

Stocks that fit into the category colloquially known as “Disruptive Technologies” skyrocketed in 2020 to unsustainable valuations and peaked in February 2021. At that time, many of those stocks that we covered were trading at 1- and 2-star ratings. These stocks then crashed back to earth in 2021 in many cases falling over 50+% from their highs. The downward momentum has now brought many of these companies deep into undervalued territory and we rate a number of them with 4- and 5-stars. Teladoc $(TDOC)$, Palantir, Twilio $(TWLO)$, and DocuSign $(DOCU)$ fall into this category.

Okta $(OKTA)$shares has bounced off its recent lows as the crisis in Ukraine and corresponding heightened concerns for cybersecurity has re-ignited the markets interest in this company. Within the cybersecurity space, Okta is one of our top picks. Identity and access management is foundational to cybersecurity and user experience, enabling workers and customers to securely access organizations' IT resources and applications. The pandemic caused well-defined security boundaries to vanish, and we think Okta is positioned to capitalize on identity becoming the new security perimeter.

Similar to Uber, Boston Beer is another way to invest in the normalization of consumer behavior. As the pandemic recedes, we expect a pickup in on-premises consumption (restaurants, taverns, sporting events, etc.) and based on the low valuation metrics for these stocks any increase in revenue would bolster investor confidence in these names.

Bed Bath & Beyond $(BBBY)$ has divested peripheral brands in order to focus on its namesake labels and has combined its online and in-store inventory management with its new “omni-always” initiative in the hopes of capturing more e-commerce business, and avoiding the long restock times and uneven inventories that previously plagued the firm. Additionally, it’s investing heavily in both its digital and brick-and-mortar platforms, with a revamp to the website for a more friction-less checkout process, and a remodel of its physical stores to offer a cleaner and more enjoyable shopping experience.

Looking Ahead

Most U.S. corporations have little to no direct exposure to Ukraine or Russia and should not see much of a direct impact on their earnings; however, the market sell-off was mainly based on the prospect that Russia’s military invasion could further exasperate global inflationary pressures.

The biggest risk to that happening even more quickly is in the energy markets. According to Dave Meats, Morningstar’s director of equity research for the energy sector, Russia’s oil exports account for approximately 5% of oil global oil supply. Furthermore, Russia provides a significant amount of natural gas to Europe, some of which flows through Ukrainian pipelines. In addition to energy, according to Capital Economics, Russia and Ukraine account for 25% to 30% of global wheat exports. Russia is also a global supplier for industrial metals such as aluminum, nickel, and palladium.

From a macroeconomic point of view, the size of Russian and Ukrainian economies ($1.5 trillion and $156 billion, respectively) is relatively small compared to the global economy ($84.7 trillion). However, there is still a potential impact from supply disruptions. For example, the Wall Street Journal reported that critical materials made in Russia and Ukraine are used in manufacturing semiconductors (already in short supply) and the disruption of these materials could heighten the current shortage.

Broadly, it is notoriously hard to predict how geopolitical events will evolve. We expect stocks will remain volatile in the short-term with brief selloffs if further escalation arises, or a snap-back rally if further Russia ceases additional military escalation.

So, what should an investor do? Maintain a long-term investment plan, review portfolio allocations, and if those allocations have shifted from long-term asset class targets, now would be a good time to rebalance.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.

is BABA consider cheap?