KLA Quarterly result review

During this volatile period, and with tech stock, especially semiconductor related stock all beaten down by 20%-30%, gloom outlook, its really hard to say "lets continue to buy, outlook is very positive...etc"

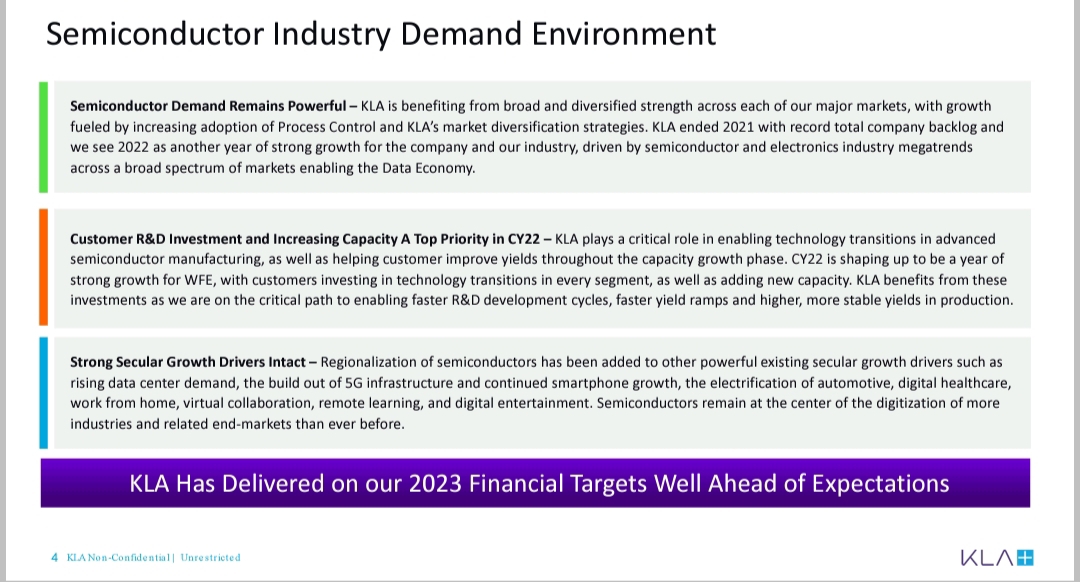

But lets take a step back, the fundamental of the company didn't change, the demand for chips did not disappear overnight, the new manufacturing plant that are in plan, are still going ahead. The order of semiconductor equipment are still in place with long queuing order and long lead time. Yes, supply chain is causing some distruption, but the backlog and bottleneck will be clear at some point. Semiconductor application can only expand from where we are today. So today, would like to share on the result from KLA. A company with I liked and shared many times.

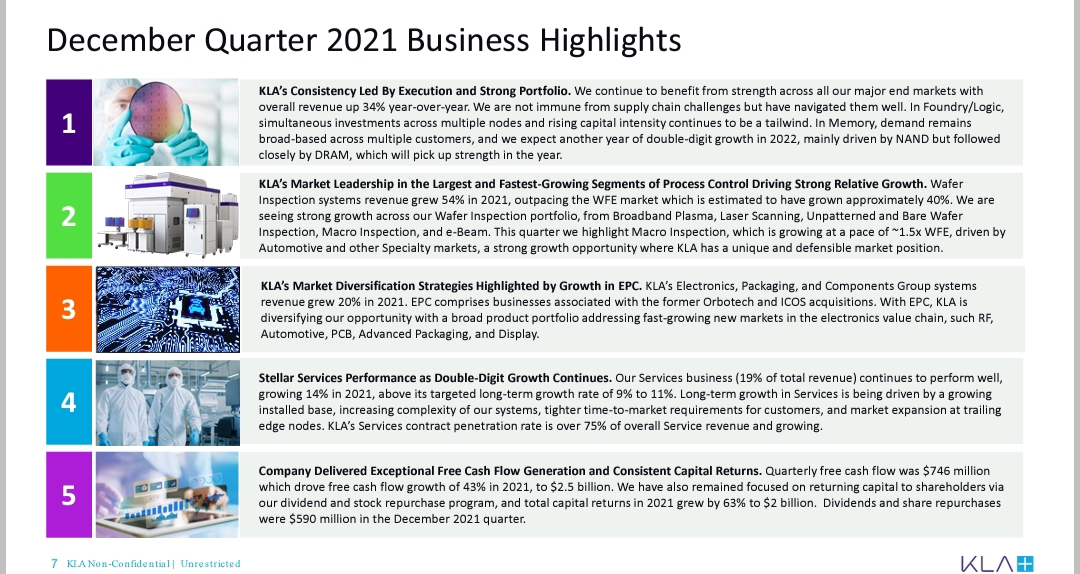

A recap, KLA Corporation develops industry leading equipment and services that enable innovation throughout the electronics industry. The company provide advanced process control and process enabling solutions for manufacturing wafers and reticles, integrated circuits, packaging, printed circuit boards and flat panel displays.

Key point of the results

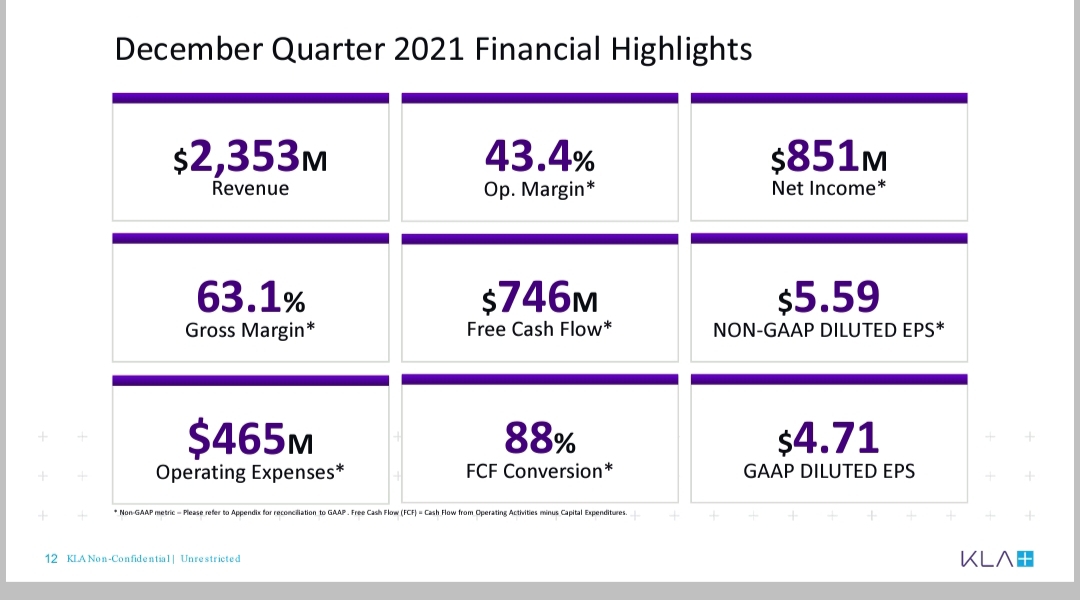

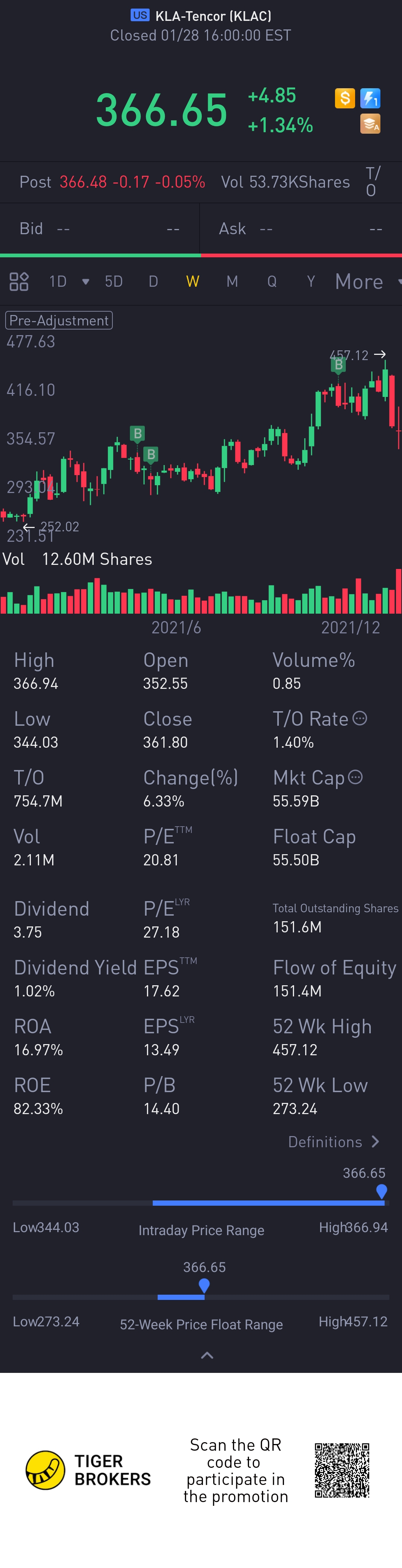

1) Total revenues were $2.35 billion, above the midpoint of the range of guidance;

2) GAAP diluted EPS attributable to KLA was $4.71 and non-GAAP diluted EPS attributable to KLA was $5.59, each within the range of guidance

3) Cash flow from operating activities and free cash flow were $810.8 million and $745.9 million, respectively;

4) Capital returns were $589.0 million with $159.1 million in dividends paid and $429.9 million in share repurchases.

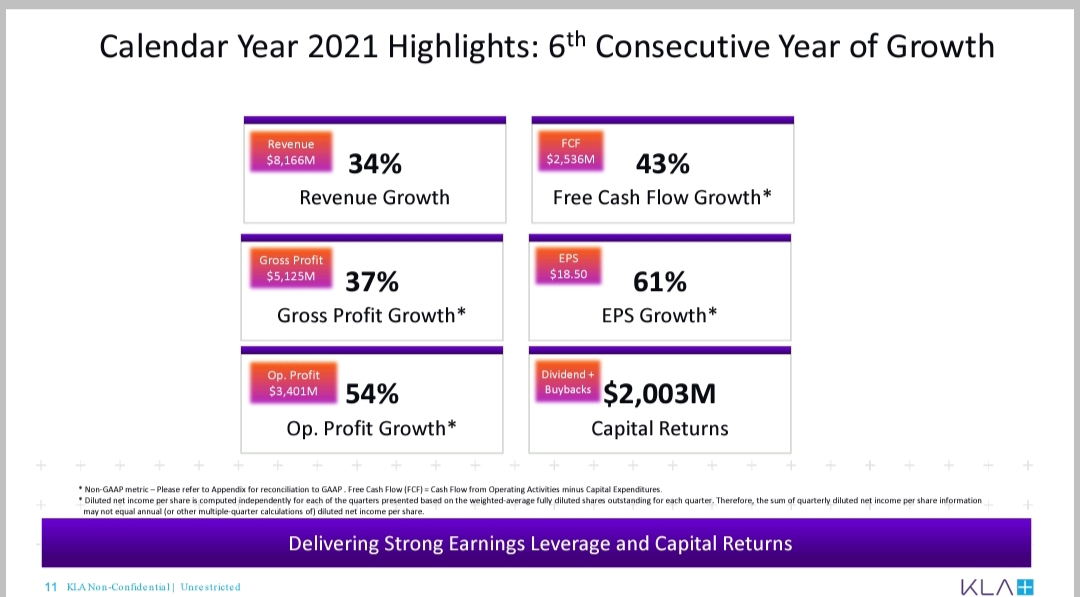

The performance exceeded expectations in a demanding and challenging environment. This results underscore the importance of their products and solutions in the marketplace, and showing their technology leadership and innovation.

KLA also returned $2 billion in capital to shareholders during calendar 2021 via both dividends and stock repurchases, confirming their strong balance sheet.

Looking forward to next quarter of fiscal 2022 ending in March, KLA provide the following guidance,

1) Total revenues between $2,100 million to $2,300 million

2) GAAP gross margin is expected to be in a range of 59.5% to 61.7%

3) Non-GAAP gross margin is expected to be in a range of 61.5% to 63.5%

4) GAAP diluted EPS attributable to KLA is expected to be in a range of $4.09 to $4.99

5) Non-GAAP diluted EPS attributable to KLA in a range of $4.35 to $5.25

The market did not react well with this guidance, calling it a weak outlook. For me, i look at it from a longer term. A market segment with huge growth potential in semiconductor, a good company KLA which is market leader and almost no competition in many of their solution with high profit margin.

I think I will just vest more and don't even look at the up and down in 2022. Because i truely believe in 3-5 yrs time, it will be worth more@小虎活动@TigerStars

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.

Repost