BILI Q4: Remains Focused on Quality Growth and Efficienc

Earnings Review

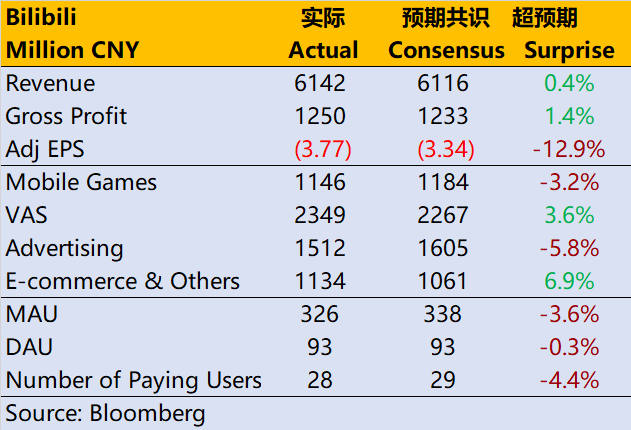

Q4 MAUs of 326M, grew 20% y/y, but down 6.6M sequentially due to seasonality. DAU growth continued to outperform MAU, up 29% y/y to 92.8M (+2.5M q/q). But average MPUs grew slower at +15% y/y to 28.1M, driving the overall paying ratio to 8.6%, down 40bps y/y. Engagement metrics continued to grow: average daily time spent was 96 minutes in 4Q, +17% y/y; active creators grew 27% to 3.8M; monthly video submissions grew 61% to 17.6M, with average submissions per creator increased 27% y/y to 4.6; average total daily video views grew 77% to 3.9B, implying daily views per MAU of 12.0, up 48% y/y; average monthly interactions per MAU increased 12% y/y to 41.7.

Revenue increased to 6.14B (+6.3% YoY), beating consensus of 6.11B; Gross income 2% above Tiger/Street, with margin 30bps/31bps higher. Revenue-sharing cost was RMB 2.5B, or 41% of total revenue, down 1pt y/y and flat q/q. Cost of revenue ratio was 79.7%, down 135bps y/y and 215bps q/q. Total Opex was 20% above Tiger, primarily due to one-off reorganization costs. In aggregate, non-GAAP operating loss of RMB 2B was 38%/39% above Tiger/Street.

By segment, mobile games revenue decreased 12% y/y (vs. +6% in 3Q), 3% below Tiger/Street, as no new games were launched. VAS revenue grew 24% y/y (vs. +16% in 3Q) to RMB 2.35B, 5%/3% above Tiger/Street. Advertising revenue declined 5% y/y to RMB 1.5B, 5%/4% below Tiger/Street, likely due to COVID outbreak. Ecommerce and others revenue grew 13% y/y to RMB 1.1B, 3%/5% above Tiger/Street.

Investment Highlights

Game business miss, new games are expected to be launched on 23Q2, VAS strong. Q4 is still affected by the shortage of new games, and its game business revenue is worse than expected. However, the company said that more games will be launched after 23Q2, including two self-developed games. Due to pandemic, the growth of broadcasting business still maintained good, while the number of large members increased by 6.5% year-on-year to 21.4 million.

Monetization of short videos is key to advertising business. Advertising business revenue 1.51 billion yuan, down 4.7% year-on-year. After the new Story Mode commercialization and transaction transformation scenarios mature, it is expected to raise expectations in the new quarter.

Profitability is new priority. Q4 gross profit margin increased by 2.1 ppt to 20.3% month-on-month, mainly due to the change of income structure. It is expected that the advertising business will rebound in 2023, which will drive the gross profit margin to increase to 25%. The operating rate is still relatively high, with the management rate increasing by 3.9 ppt to 13.3% month-on-month and the R&D rate increasing by 4.8 ppt to 24.3% month-on-month. The one-time expenses of layoffs and self-developed games are dominant, and the optimization results will appear in 2023. As bilibili is the latest Internet company to reduce costs and increase efficiency, the effect has not been fully reflected.

Users Declining? Pay attention to monetization of DAU.,Q4's marketing expenses dropped sharply year-on-year, reducing customer investment, and the growth of users slowed down (lower than expected, and lost 6.6 million users for the first time). The market also has some concerns about whether the "target of 400 million users by the end of 2023" can be achieved as scheduled, but fortunately, it may achieve a single-quarter break-even. 2023 may be a year in which user growth, cost reduction and efficiency increase are balanced. The proportion of daily life is further increased, which is related to the content, and how to get more cash flow from daily life users will become the key to reduce losses and profits.

Estimate and Valuation

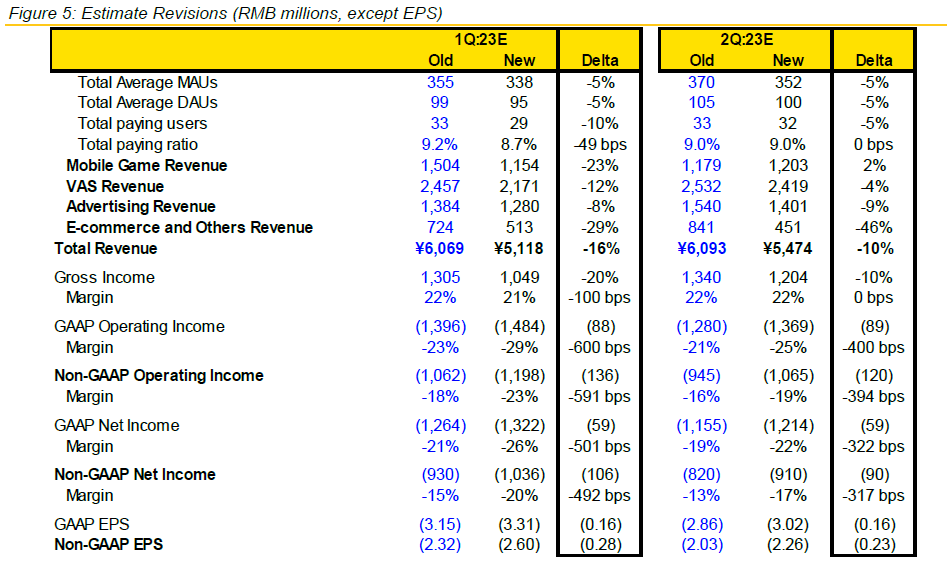

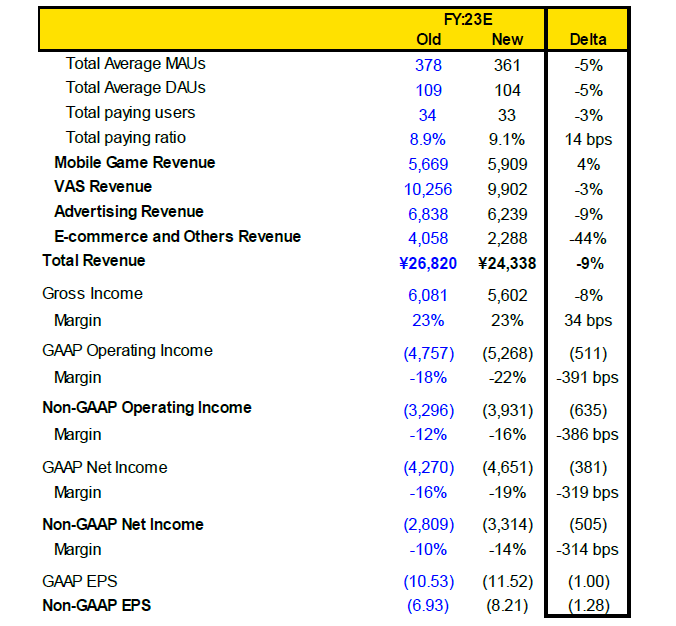

BILI guided '23 full-year revenue to RMB 24B to 26B, implying 14% y/y growth at the midpoint, accelerating 1pt from '22, 7%/4% below Tiger/Street estimates. Consistent with last earnings, BILI says it will focus on quality growth and efficiency gains in '23. Specifically, it aims to halve non-GAAP operating loss by 50% y/y in '23, with roughly 2/3 coming from increased gross income (gross margin to reach mid-20s by year-end) and 1/3 from lower Opex; and ultimately achieve non-GAAP EBIT breakeven in '24.

We are maintaining our BUY rating and $25 PT (unchanged) after BILI reported largely in-line 4Q results with '23 revenue guidance slightly below consensus.

Risks

1) Competition: BILI is competing with larger companies (e.g., ByteDance, Tencent and Kuaishou); 2) Foreign company risk: US has passed the Holding Foreign Companies Accountable Act, which requires more disclosures by Chinese companies listed in the US and might impact their listing status; 3) Data security risk: China is tightening the data security rules and might restrict companies with sensitive data from listing overseas; 4) VIE risk: China might also tighten the use of a VIE (Variable Interest Entity), a corporate structure most Chinese Internet companies use to attract foreign capital and list overseas; 5) Content regulation risk: China has relatively stringent content regulations. BILI might be required to remove certain content and suspend services if it fails to detect inappropriate content; and 6) Game regulation risk: Games in China need to receive approvals from regulators before they can be launched. If the regulators suspend the approval process, BILI's game business could be impacted.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.

- Sonar·2023-03-04Thanks for sharing1Report

- ikiwkiw73·2023-03-04Great ariticle, would you like to share it?1Report

- GerryLoh·2023-03-04good sharing thanks1Report

- xiaobaii·2023-03-04like & comment please2Report

- SPOT_ON·2023-03-08okLikeReport

- JTC·2023-03-07kLikeReport

- sky老夫子·2023-03-05加油1Report

- Karma Rider·2023-03-05delivery cost1Report

- 建稳的朋友·2023-03-05🙏🙏LikeReport

- 爱上投资学·2023-03-04OKLikeReport

- pyc·2023-03-04[强]LikeReport

- Chani·2023-03-04NiceLikeReport

- ethanlam·2023-03-04ok1Report

- Shashi rana·2023-03-04Ok1Report

- Alvis89·2023-03-04Go od1Report

- Tan Chung Hong·2023-03-04👍2Report

- V.lye·2023-03-04ok2Report

- NgKenny·2023-03-04Nice2Report

- ongcjeric·2023-03-04Hh1Report

- Aeron2020·2023-03-04ok1Report