How Valuation changes after Alibaba's split?

Alibaba As a Whole

Because of the complicated business, large companies often consider the overall indicators of the company in valuation, such as profit (P/E, EV/EBITDA), income (market-to-Sales ratio, EV/Sales) and cash flow (P/FCF, DCF discounted sustainable cash flow). The advantage is intuitive, simple and can be compared horizontally; The disadvantage is that it is difficult to maximize the valuation potential of each business.

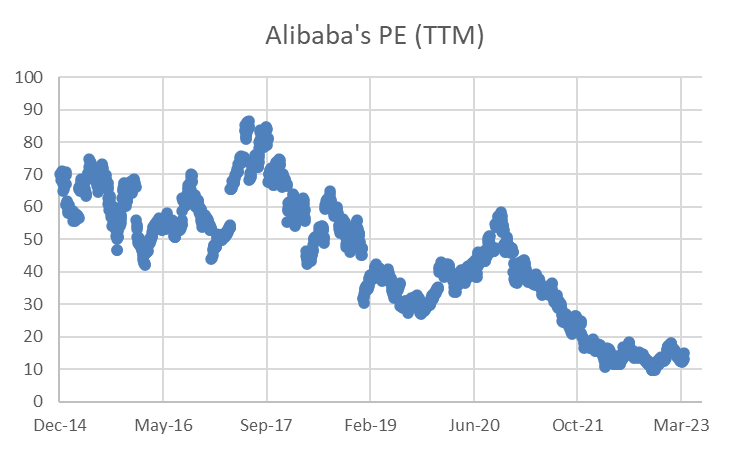

For Alibaba, the latest dynamic P/E is 15 times.But the average ttm P/E since listing is 44.2x, Even since July 2021, it has an averag of 17.2 times. The current valuation is lower than the historical average, that is, "Undervalued".

2024 adjusted EPS is 60.5 yuan(market consensus), That is, the valuation in 2024 should be US $154 per share, equals US $130.6 per share in 2023 at a discount rate of 18%.

After split

After the split, each business department is an independent part, so it needs to be valued separately. The valuation method adopted is "Sum of the Part", which is often used by analysts. The greatest advantage is that it will not waste hidden value.

Alibaba announced the "1 +6 + N" organizational structure. Under the group, it set up six business groups and several business companies, including Alibaba Cloud Intelligence, Taobao Tmall Business, Local Life, International Digital Business, Rookie and Grand Entertainment. It means that these six businesses should be valued separately.

1. Taobao Tmall is the core and domestic e-commerce business.Because the industry is relatively mature and the profit rate is stable at over 30% (the profit of individual business modules is greater than that of the whole company, only because other businesses lose money), it is still suitable to take profit multiples or discounted cash flow for valuation.

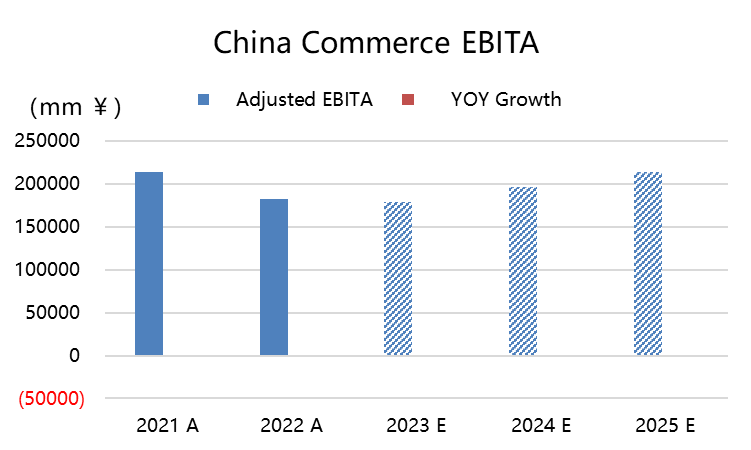

The expected adjusted profit (EBITA) in 2023 is 179.4 billion yuan (conservative value). If we give this part 17.24 times the average P/E of the company since 2021, the valuation of this part should be 30,936 trillion yuan.

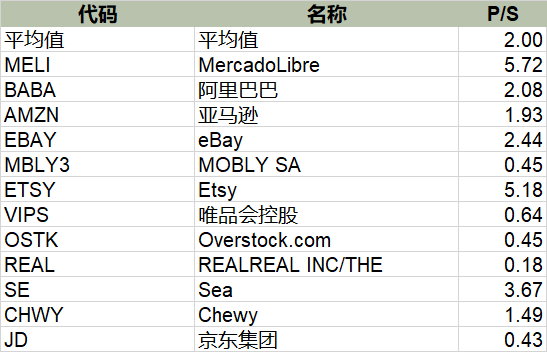

2. International digital commerce is also e-commerce. However, due to continuous losses, it cannot be valued in the form of profit or cash flow multiples at present. Referring to other overseas e-commerce platforms, including $SEA (just profitable) and $MELI, many of them are still losing money, so it is more appropriate to use revenue multiples. As the company is also a combination of self-operated and three-party, average the average number of three-party platforms and self-operated platforms, and give 1 times PS.

Based on the expected revenue of 66.6 billion yuan in 2023, the valuation of this part is 66.6 billion yuan.

3. Alibaba Cloud Business,It is a high-growth business in itself, but it has also fallen into stagnation after 2021, and it is expected to achieve break-even this year by continuously reducing costs and increasing efficiency to improve profit margins.

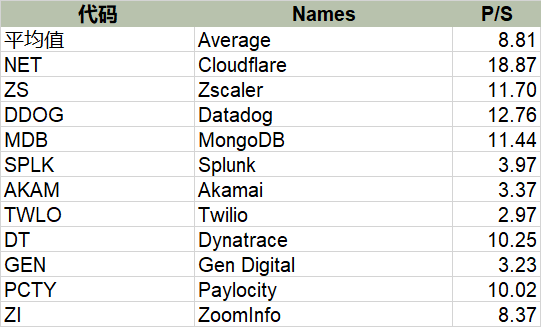

The market once gave cloud service companies a high valuation multiple, even reaching a triple-digit market sales rate. However, the current industry average market sales rate is 8.8 times. Considering that Alibaba Cloud's business is difficult to expand abroad, we will make a conservative discount of 4.4 times the market sales rate.

In 2023, the market expects the revenue of cloud business to reach 79 billion yuan, that is, the business valuation of this part is 348 billion yuan.

4. Local life businessIt is a business with high growth but large losses. In fact, Ali's local life includes a large number of business types, so its valuation is relatively general, which is suitable for valuation by multiple of income. Most of the similar companies listed in China have a market sales rate of about 1 time.

Based on the expected revenue of 48.7 billion yuan in 2023, a double market sales rate is a valuation of 48.7 billion yuan.

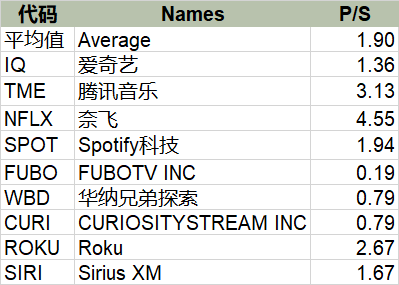

5. Big entertainment businessAt present, Youku's long media market is weaker than Tencent Video and iQiyi, and there is even the risk of being run by short videos. The business is not yet profitable, and the profit expectation is unknown. In fact, it is a risky piece. At present, the average market sales rate of the industry is 1.9 times, but it is mainly brought by leading companies such as Netflix. Excluding giants, the average market sales rate is 1.4 times, which is close to the level of iQiyi.

Based on the expected 31.5 billion yuan in 2023 and 1.4 times the market sales rate, the valuation is 44.4 billion yuan (it seems that this business is unlucky).

6. Cainiao as a logistics business,It should be kept at the same level as the profit margin of logistics companies. At present, the profit margins of domestic logistics companies are uneven. Apart from different business scales (affecting marginal profit margins), the rules for revenue recognition are different. For example, the profit margin of Zhongtong is nearly 20%, while that of SF Express is about 4%. The latest profit of Jingdong Logistics is less than 1%, and it is expected to be less than 1% after the profit in 2025.

The market expects Cainiao Logistics to achieve profitability in 2024, possibly earlier. It is expected that the profit rate will reach nearly 2% in 2025, that is, 1.4 billion yuan. In a conservative way, the industry average P/E of 25 times, that is, the market value of 36 billion yuan, will be given at a discount rate of 11% to 2023, that is, 29.3 billion yuan.

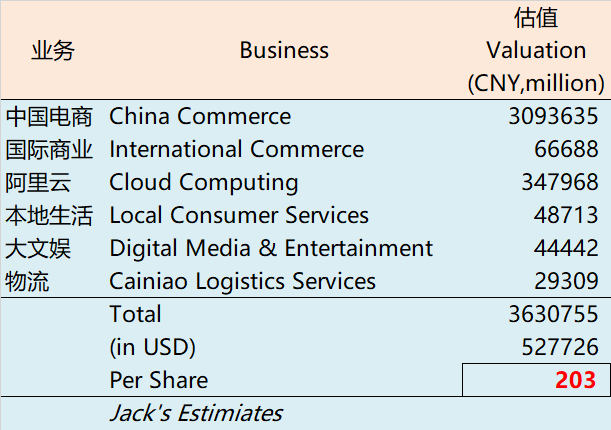

To sum up

Taken together, Ali's valuation should be $527.7 billion, or $203 per share. This is quite different from the previous separate calculation of $130.6

Do you think splitting is valuable?

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.

Great ariticle, would you like to share it?

Great ariticle, would you like to share it?

Great ariticle, would you like to share it?

What is “N”???