“Crony Capitalism”

A Historic Policy “Blunder” By The World’s Most Powerful Central Bank?

With some notable exceptions, businessmen favour free enterprise in general but are opposed to it when it comes to themselves”- Milton Friedman.

Much has been said and written about the Silicon Valley Bank (SVB) collapse and the subsequent events that unfolded post the meltdown. So, I would not waste your precious time by repeating the obvious.

However, we can’t ignore the precedence that the Federal Reserve has set in tackling the SVB crisis. Furthermore, the episode again brings to the limelight the complete failure of regulatory oversight by the regulators.

The preposterous policy that the Fed has unleashed to avoid a “systematic” collapse of the US banking system has transformed the basic foundation of monetary policy. As a result, some say that we are on the cusp of a “turbocharged” monetary policy.

Though we will cover this in detail today and its long-term implications, the one thing that matters most is who did the Fed bailout?

It’s a no-brainer that SVB had more than 94% of the uninsured deposits (more than $250k) or, in other words, was a bank of the “riches”. Isn’t bailing out the rich /VC world signifies that we are in a “regime” of crony capitalism?

Doesn’t the failure of many regional banks lead to the big banks becoming bigger and more powerful?

Haven’t we learnt anything from the banker’s greed that led to the Great Financial Crisis in 2008?

Can we conclude that our banking system is more fragile than ever, and in the age of social media, where information flows like wildfire, there is a grave risk that such spontaneous tragedies may occur frequently?

Does the new QE + higher rates paradigm lead to soaring inflation expectations?

Has the Fed lost the inflation battle?

The latest sequence of events raises some crucial questions whose answers are key to investing your hard-earned money.

Let us dig deep and understand the Fed’s bailout and its implications on the economy, inflation and markets.

The “Bailout” And Implications!

Just before the weekend’s release of the joint statement by the Fed, US Treasury and the FDIC, there was a fierce debate on social media about the “uninsured” deposits. Most of the market participants believed that since SVB was not a G-SIB (Globally Systematic Bank), the usual course of action should take place.

Most people expected a recovery of 80–90c per $1 for the uninsured guys; however, in a stunning announcement, the Fed decided to bail out the depositors while equity and some unsecured bondholders would lose all their capital.

This virtually meant that Fed would now jump in and backstop $17 trillion of deposits irrespective of the size of the account and “bank”.

Now, I would call this a policy “blunder” and a historic mistake by the Fed.

The move raises eyebrows, and the prime explanation is that the all-powerful VC community led to this move.

Nevertheless, the most significant concern remains the policy move concerning the Fed’s discount window.

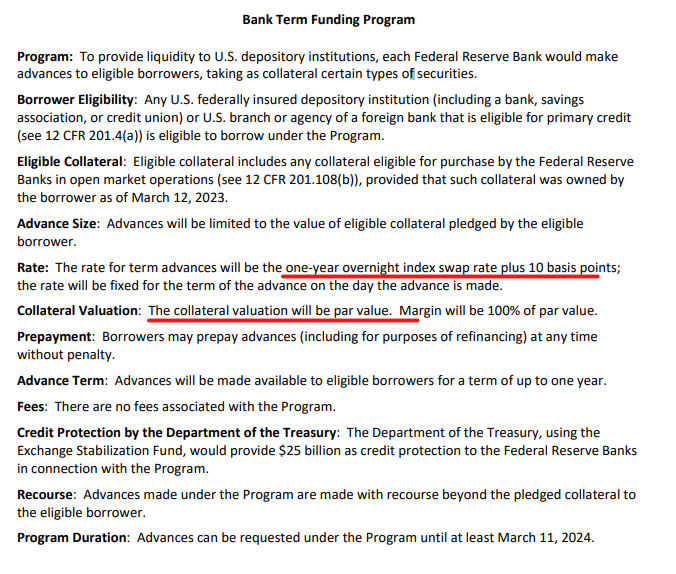

Bank Term Funding Program (BTFP) is an extreme out-of-the-box policy move undertaken to avoid a systematic collapse in case there is a flight of deposits across the system.

As per the BTFP, banks can now borrow for one year against UST, agency debt and MBS through BTFP by valuing the collateral at par, at a rate of 1Y OIS + 10 bps.

The most shocking move is “valuing the collateral at par”. In an unbelievable move, this was designed so that:

- Banks do not sell their HTM (Held-To-Maturity) holdings and book their unrealised losses, thus risking their equity. By borrowing from the Fed’s discount window for one year, banks can temporarily meet their liquidity needs, and the Fed thus acts as a lender of last resort.

- The Fed temporarily absorbs all the losses banks incur, thus providing them relief. The losses will be transferred to the Fed if and when realised, only if the bank borrowing from the Fed goes belly up.

The implications of this astounding move:

- Firstly, if many regional banks borrow from the Fed under BTFP, then there can be a significant expansion of the Fed’s balance sheet igniting inflation fears as financial conditions may ease going forward. The last thing Fed now wants is more liquidity hampering its QT program.

- Secondly, suppose collateral values don’t rise in the next year (assuming rates remain way higher than when they were accumulated in 2020–21), then considering the interest burden; weaker banks will still have to raise capital to survive even if things normalize thus permanently eroding their stock prices or equity values.

- Thirdly, these moves will immensely benefit the big banks or Too Big To Fail (TBTF) or G-SIB as they will get the lost businesses of now defunct banks. I expect at least $200–300 billion of deposits to move to the big four banks.

Market’s Reaction!

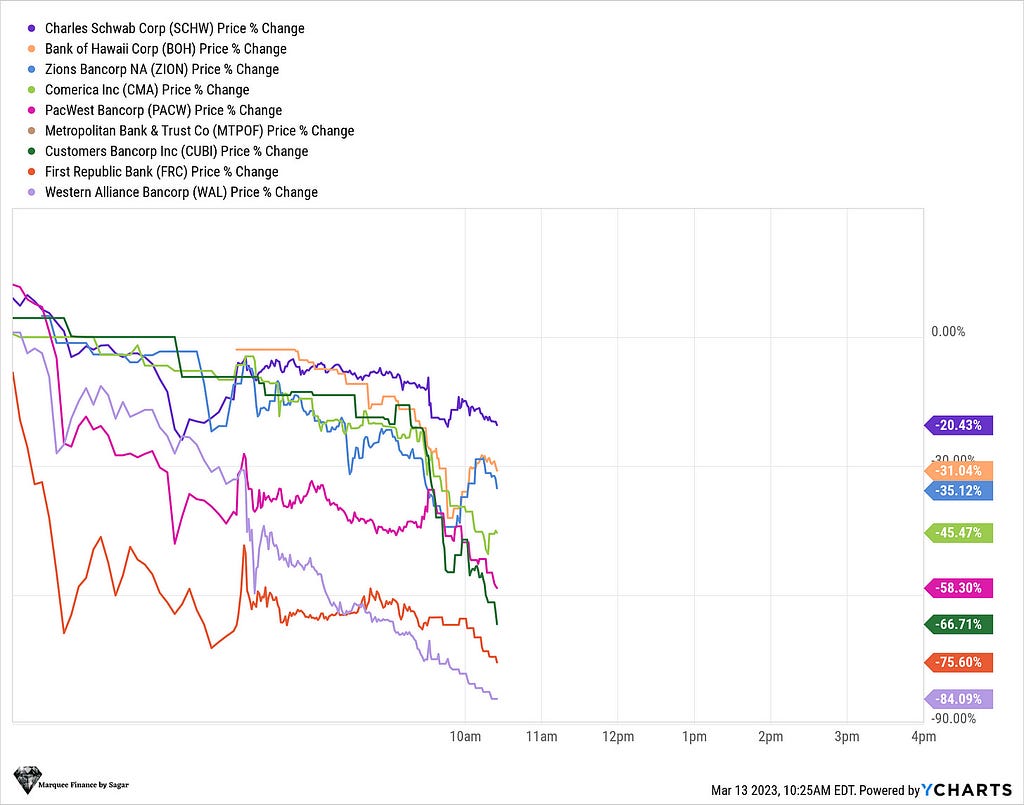

There is panic in the regional bank’s stocks as most are witnessing their worst sell-off “ever”.

The unprecedented pace indicates that markets believe that the regional banks are insolvent, with the Fed backstopping only the deposits. At the same time, equity will eventually be marked down to zero.

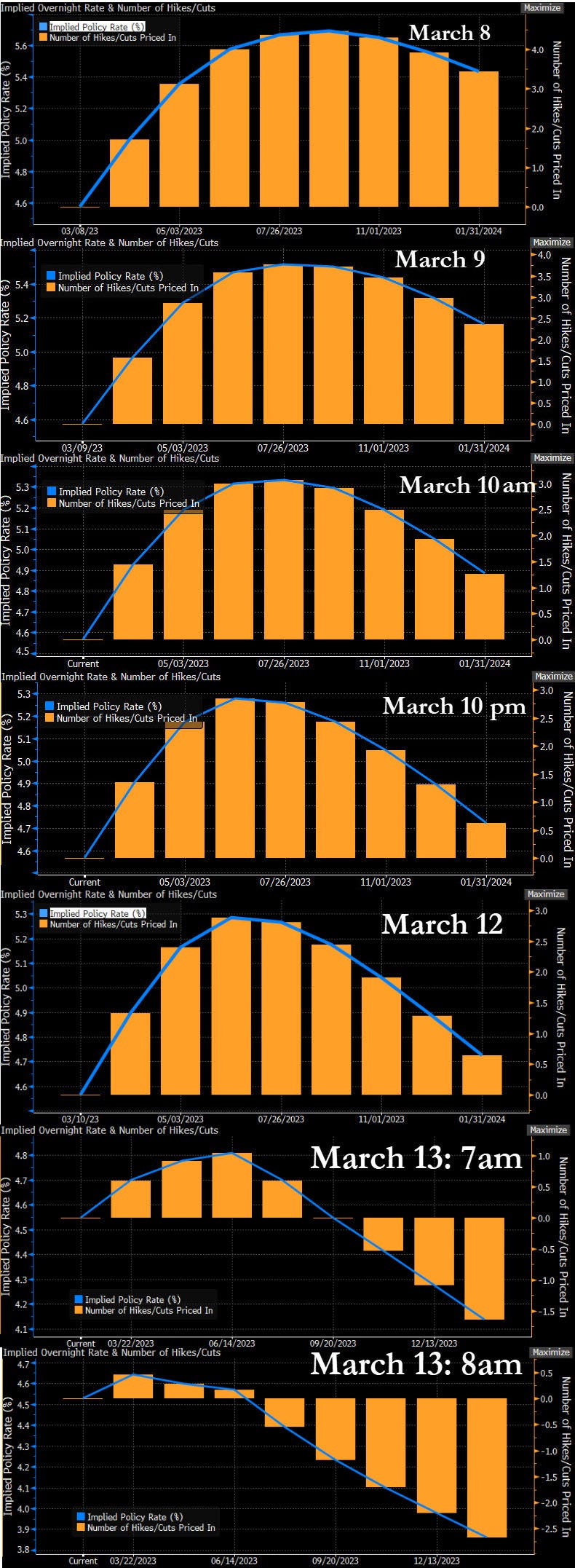

On the other hand, the long-awaited steepness arrived as the 3-day rally in 2Y was the most since Black Monday 1987.

In what could be termed as an unprecedented U-Turn, the markets are now pricing in an imminent pivot in the March policy and a 50 bps cut before the end of 2023.

While the pivot hopes cheered the tech stocks, gold and BTC, the FX market also got the taste of the pivot as CHF rallied, and the DXY was down 2% from its highs on Thursday.

Nevertheless, the true extent of the stress in regional banks will be evident in the next few days as the usage of the Fed’s discount window details emerges.

The current interbank liquidity is frozen, as visible from the FRA-OIS spread.

Note: The FRA-OIS spread measures the difference between the three-month Libor, or the inter-bank lending rate, and the overnight index rate, or the EFFR (Effective Fed Funds Rate).

The rise in FRA-OIS spreads indicates fear and shows that banks perceive interbank lending as risky.

Though, I believe this too shall pass as the weak banks go down under and the rest emerges stronger (primarily big banks).

The bottom line is that markets got their pivot, but the biggest question remains:

If the Fed pivots considering the stability of the banking system while the inflation still runs hot, then my friends, I would consider this as the worst-case scenario and a possible defeat of the Fed against the inflation battle.

The only way in this scenario the inflation comes down to the 2% level will be a “hard landing”.

Thus the Fed pivot at this stage increases the odds of a hard landing.

Conclusion!

Unfortunately, we have entered unchartered territories with the latest unprecedented moves by the Fed. As a result, next week’s FOMC meet becomes one of the most important in history, and a “pivot” means the risk of losing control against the monstrous inflation.

Furthermore, big getting bigger hurts competition and is against capitalism’s essence; thus, there is no doubt that there is a smell of crony capitalism in yesterday’s Fed moves.

Higher for longer is necessary to quell the inflationary fire, but in the quest to do so, the Fed’s balance sheet expansion might be counterproductive (though we would have to wait for the exact numbers).

The $17 trillion deposit guarantee and the “turbocharged” monetary policy is a horrific precedence and will not augur well in the long term.

“Crony Capitalism” was originally published in DataDrivenInvestor on Medium, where people are continuing the conversation by highlighting and responding to this story.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.

- MilkTeaBro·2023-03-20thanks for your informationLikeReport

- Stormriders28·2023-03-20KLikeReport

- SmartyCub·2023-03-20HmmLikeReport

- LuckyPiggie·2023-03-20thanksLikeReport

- peng321·2023-03-20👍LikeReport

- Just Do It·2023-03-20[shy]LikeReport

- 道心不变·2023-03-20[微笑]LikeReport

- BengSeng·2023-03-20doesLikeReport

- iamjingxian·2023-03-20OkLikeReport

- luv2trade·2023-03-20okLikeReport

- 蓝天一小白云·2023-03-20👍LikeReport

- _J_R_·2023-03-20KLikeReport

- JLSE·2023-03-20👍👍👍LikeReport

- LTTan·2023-03-20👍1Report

- Marcus146·2023-03-20[强]LikeReport

- LEEKONGYONG·2023-03-20OkLikeReport

- Aaronykc·2023-03-20👍LikeReport

- Goldilock·2023-03-20👍🏻LikeReport

- earn a meal·2023-03-20KLikeReport

- WmochaW·2023-03-20ThanksLikeReport