Tencent Q4 Earning: recovery is on the way, time to buy

$TENCENT(00700)$ released Q4 2022 and its full-year earnings after Mar,22.

Sales slightly beat market consensus, the effect of reducing costs and increasing efficiency continues, and the margin promoted better than expected. Offline business still affected, while games and entertainment performed steadily. Fortunately, video content is entering an accelerated monetizing period, ads revenue growing strong recovery potential. We expect further recovery in 2023.

Overview of Q4 performance

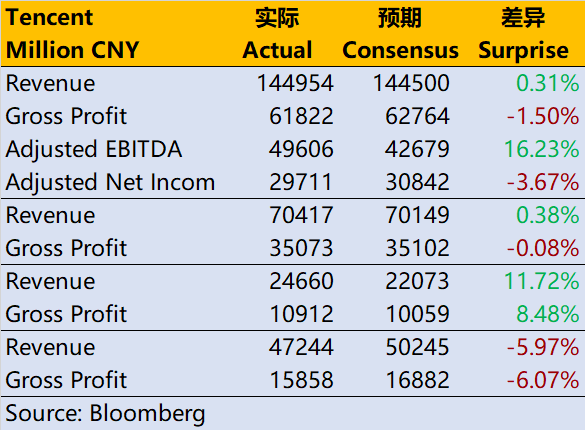

Revenue 144.95 billion yuan, up 1% year-on-year, higher than the market expectation of 144.50 billion yuan. Among them,

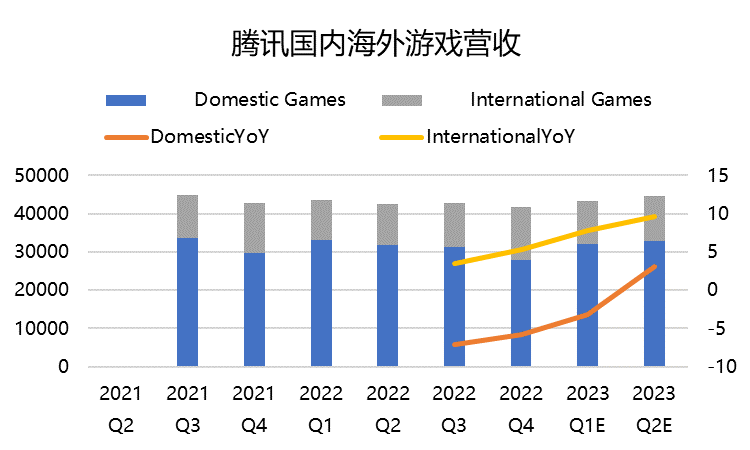

- The overall income of value-added services was 70.4 billion yuan, down 2% year-on-year, slightly higher than the market expectation of 70.1 billion yuan; The overall revenue of the game business was 41.8 billion yuan, which was the same as expected year on year. Domestic games decreased by 6% year-on-year to 27.9 billion yuan, slightly worse than the expected 28.7 billion yuan; Overseas games amounted to 13.9 billion yuan, excluding the influence of exchange rate and Supercell adjustment, which increased by 11% year-on-year, higher than the market expectation of 13 billion yuan. Social network revenue was 28.6 billion yuan, down 2% year-on-year, lower than the market expectation of 29.2 billion yuan.

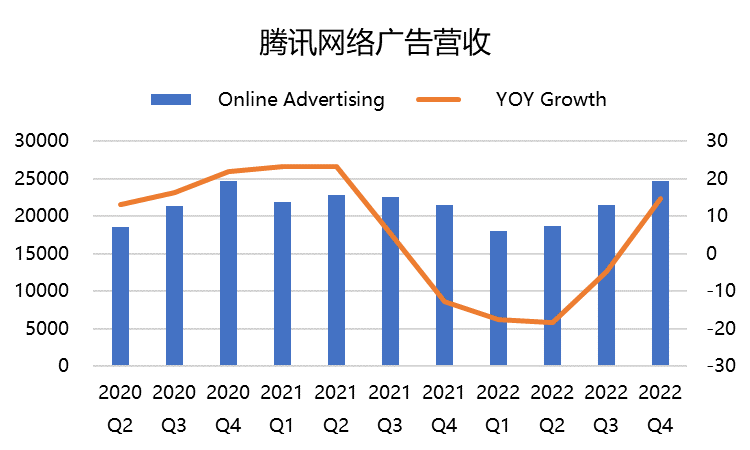

- The revenue from online advertising business was 24.7 billion yuan, up 15% year-on-year, which was significantly higher than the market expectation of 22.1 billion yuan. Among them, social advertising increased by 17% to 21.4 billion yuan, and media advertising revenue reached 3.3 billion yuan, which also resumed year-on-year growth.

- Financial technology and enterprise business income was 47.2 billion yuan, down 1% year-on-year, lower than the market expectation of 50.2 billion yuan.

Cost

- The operating cost of value-added services decreased by 4% year-on-year, mainly due to the reduction of live broadcast sharing and channel distribution; The cost of online advertising business increased by 11% year-on-year, mainly video and small programs and mobile advertising alliance; The cost of enterprise technology business decreased by 10% year-on-year, which was mainly reflected in the loss reduction of cloud services.

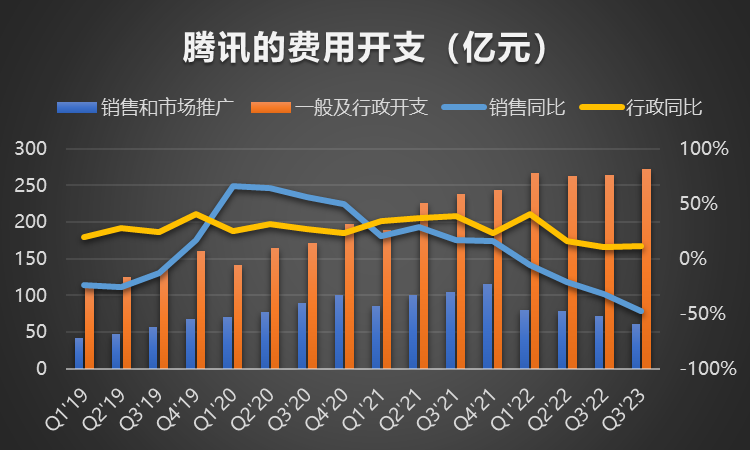

- Marketing expenses were 6.1 billion yuan, down 47% year-on-year, far lower than the market expectation of 8.3 billion yuan;

- Administrative expenses were 27.3 billion yuan, up 12% year-on-year, higher than the market expectation of 26.3 billion yuan.

Profit

- Gross margin 42.6%, an increase of 150bps over the same period of last year, and also higher than the market expectation of 42.54%.

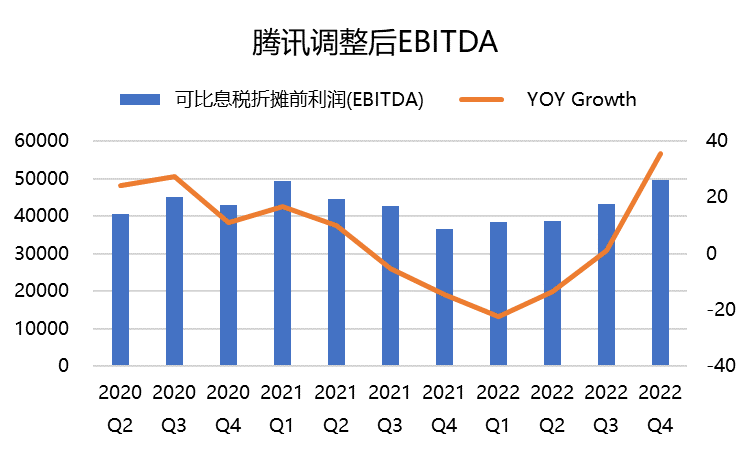

- The adjusted EBITDA was 49.6 billion yuan, up 17% year-on-year, which was the same as the market expectation of 49.5 billion yuan, and also increased the profit rate to 34%.

- The adjusted comparable net profit of Non-IFRS was 29.7 billion yuan, up 19% year-on-year. Since Q3 2021, it resumed double-digit growth for the first time, but it was slightly lower than the market expectation of 30.8 billion yuan, mainly due to the impact of some reduction items.

Investment Highlights

Game weaker domestic and stronger international, expecting recover in Mid 2023. We think there are two impacts on the decline of domestic game revenue, one is the pandemic situation (the last season), and the other is that the version number has not approved. October-December is the last season of the epidemic, and entertainment activities continue to be affected. At the same time, most people experience 1-2 weeks of illness, which affects games and related live broadcasts. On the contrary, the growth of end games exceeds that of mobile games. The version number was reissued in early 2023, so Q4 domestic games were worse than expected. However, the company also explained that "the glory of the king" resumed the year-on-year growth of DAU in Q4, and achieved a new high in the 23-year Spring Festival holiday, which also indicated that there was a rebound after a wave of epidemic in domestic games. The launch of new games, including "Code Dawn" and "the glory of the king World", may bring new growth points to Tencent after Q2.

Overseas game business grew more than expected,Q4 contributed 33% of the total game revenue, compared with 28% last year. "VALORANT" continues to be popular with players, and the call of duty mobile game and the new game "Victory Goddess Nikki" have also played a lot of roles.

Online video is affected by the delay of content broadcasting, and Q1 is expected to recover strongly.The number of Tencent video members in Q4 decreased slightly to 119 million, which was lower than the market expectation, and the overall entertainment revenue was also about 2 points lower than expected. This is mainly affected by the delay of content broadcasting, because "Three-body", a heavyweight new drama, was launched in January 23. Controversial issues such as the collapse of the word-of-mouth of bilibili animated version of "Three-body" and the restriction of iQiyi in multiple clients have also given Tencent video some room for growth. We are optimistic that Q1 Tencent video will return to growth.

Advertising in great potential for online and offline recovery. The most overjoyed business unit of Q4 is advertising. Besides the traditional media, the content ecosystem opened by video number has played a lot of roles. Video News has released more advertising inventory including video number information flow advertising, improved advertiser demand, and strengthened the ability of advertising ecosystem to drive transactions. Advertisements drained to WeChat and applets of merchants and enterprises account for more than one-third of WeChat advertising revenue. The video number of Q4 and the reading time of applets also exceed the circle of friends. Advertisers are extremely sensitive to the efficiency of advertising transformation, and the continuous presence of advertisers also shows that the advertising efficiency of Tencent's content ecosystem is improving. With the strengthening of enterprise activities after the epidemic in 2023, the advertising business is expected to further recover in 2023.

Fintech and enterprise business still weak, cloud need to reverse loss.As offline payment and corporate activities are affected, the overall revenue is worse than expected. We expect a good recovery in 2023 after the recovery of business activities and the increase of the application scope of small programs. The cloud business focuses on reducing losses in Q4, which has made a lot of contributions to profit margins. Pony Ma himself does not ask Tencent Cloud to care too much about market coverage, but to improve efficiency. It is expected that the growth rate of Tencent Cloud business will stabilize in 2023, and it is expected to achieve breakeven.

Cost reduction and efficiency increase continued, core profit indicators beats.Q4 Tencent's gross profit margin was 42.65%, up 150bps year-on-year, but down from 44.24% in the previous quarter. Tencent is shrinking its clothes and dieting in other businesses, and its marketing cost has been cut by 47%. Only the cost growth in online video and mobile advertising alliance is higher, which is also the focus of growth in 23 years. The increase in management expenses is, on the one hand, the investment in overseas business, such as overseas games, and on the other hand, the one-time layoff cost.

Q4 is affected by dividends of Meituan stock, and there are many one-off items.

We believe that the adjusted EBITDA is the most suitable indicator to observe Tencent's profit margin, and EBITDA increased by 19% in Q4, exceeding market expectations.

Estimates and valuation

Tencent's dynamic P/E after Q4 financial report is only 15.4x, far lower than the average level of the past 10 years, lower than the average level of major global entertainment companies(23.6x) and lower than the average level of major overseas technology companies.

Market is optimistic about its 2023. It is estimated that the overall revenue will increase by 11% year-on-year to 616.8 billion yuan, and the profit will increase by 24% year-on-year, while the P/E at current prices is only 12.6 times

Extremely Cheap!

Noted, as the discount between the stock price and intrinsic value of Naspers, the major shareholder, has not narrowed much, we expect that major shareholders may not stop selling in the short term, which is also the reason why Tencent's stock price continues to be under pressure.

If Tencent restarts repurchase after Q4 financial report, it will relieve the selling pressure on the current disk to a certain extent.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.

Great ariticle, would you like to share it?

Great ariticle, would you like to share it?

Are you buying?

Thanks for the tip

Interesting...

Share