Default again? Why is market betting debt ceiling fight?

Last week's data showed that the US manufacturing and service sector PMIs rose for the fourth consecutive month. The April Markit Manufacturing PMI was 50.4, higher than the previous value of 49.2 and above expectations of 49, returning to expansion territory after six months; while the Service Sector PMI was 53.7, higher than the previous value of 52.6 and above expectations of 51.5 but slightly lower than in recent months.

In Europe, while manufacturing PMIs continued to decline, service sector activity improved with April Markit Manufacturing PMI at 45.5, lower than the previous value of 47.3 and below expectations of 48 for a third consecutive month; whereas Service Sector PMI was at 56.6 which is higher than its previous reading (55) marking fifth straight monthly gain.

Japan's March CPI YoY remained steady at 3.2%, matching market expectations but still higher compared to last year’s figure (3.3%) excluding fresh food & energy items it stood at 3 .8% YoY beating estimates by recording an increase from last year’s figure (3 .5%). Meanwhile services CPI maintained a certain level.

Additionally, according to EPFR data: US stock market funds saw outflows worth $1 .975 billion after inflows worth $5 .392 billion in the prior week; emerging markets equity funds saw inflows worth $2 .222 billion reversing outflows worth $215 million in prior week.

Chinese assets

As MSCI China Index fell by -2.4%, Hang Seng State-owned Enterprises Index dropped by -2.2% and Hang Seng Index declined by -1 .8%. Insurance and energy sectors led gains rising by +3.2% and +2.6%, respectively; however real estate (-5%)and media/ entertainment (-4.4%) sectors lagged behind.

According to data released by the National Bureau of Statistics, China's Q1 2023 GDP YoY growth was 4.5%, significantly higher than market expectations of 4% and last quarter’s figure (2.9%). Domestic consumption became the main driving force for economic growth recovery, contributing about 66.6% to GDP growth rate.

In addition, attention has been given to "China's unique valuation system" related areas where public funds have increased their holdings in undervalued state-owned enterprises which are still underweighted as a whole; it is expected that three types of companies will continue to receive repair: 1) leading national enterprises with strong competitiveness in core technology fields; 2) state-owned enterprises with stable valuations and reform and capital operation expectations; 3) companies benefiting from national strategic opportunities; and finally high-quality state-owned enterprises with abundant cash flow, potential dividend and buyback capabilities, and high dividend yields.

Federal Reserve officials' statements indicate that they believe the economy still has resilience

Cleveland Fed President Mester said that we are now closer to ending tightening than at the beginning but how much more interest rates need to be raised or how long restrictive policies should be maintained depends on economic and financial developments. She also urged caution regarding potential economic risks from banks while acknowledging recent banking pressures that could inhibit credit extension & economic activity.

Fed Governor Cook stated on Friday that although US inflation had slowed down recently it remained relatively high while labor markets had cooled off somewhat but many indicators still showed strong employment such as African American unemployment rate being only slightly above overall unemployment rate compared historically when it used to be around +4-5%. This indicates that employment gains have extended across broadest swathes of society suggesting greater resilience for economy than anticipated.

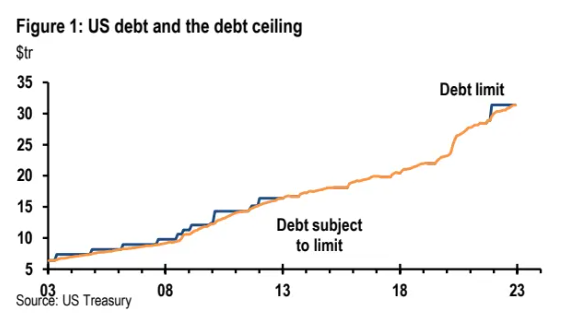

The US debt ceiling cannot be ignored either

In January this year, the US hit its statutory $31 .4 trillion debt ceiling and has not raised it since. This could lead to a risk of default on its debt obligations, which would have widespread implications for global financial markets. At the same time, this increases the prospect of extending short-term debt limits.

Treasury Secretary Janet Yellen said that government spending before early June will not increase the limit reached in January, so it may exhaust its cash and borrowing capacity at some point in Q3 or Q4. The day when this happens is called "X Date."

Currently, weak tax revenue collection during April's tax season may bring forward the deadline. Until Congress passes legislation to raise the debt ceiling, Treasury cannot issue new bonds; therefore Treasury can only take special measures (extraordinary measures) such as using cash reserves (Treasury General Account or TGA account) and suspending some non-essential expenditures.

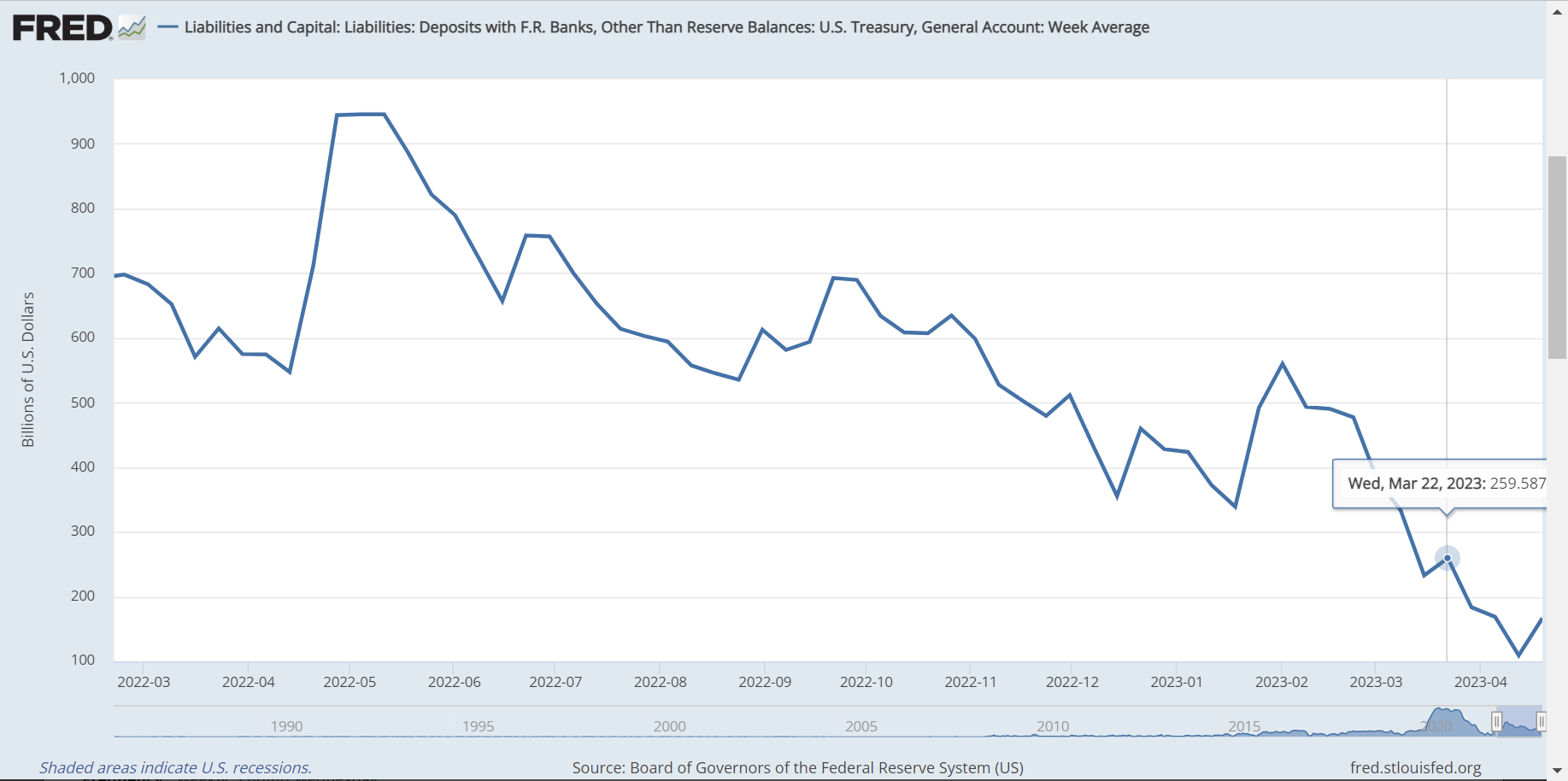

According to data from St Louis Fed: The Treasury Department's TGA account fell rapidly from $573 billion in late January to $166 .6 billion on April 19th. On annual tax filing deadline day i.e., April 18th US treasury collected total taxes worth $1298.2 billion

According to data from the St. Louis Fed, the US Treasury's TGA account fell rapidly from $573 billion in late January to $166.6 billion on April 19th. The US Treasury collected a total of $129.82 billion in taxes on the annual tax filing deadline of April 18th, with a significant drop in tax revenue for April and lower government spending compared to last year's $262.8 billion.

If tax revenues fall by 35% or more year-on-year in April, the Treasury may announce early June as the final deadline for raising the debt ceiling. However, if tax revenue does not fall below 30%, then late July is more likely to be the deadline.

What is the market response?

The market has responded with some short-term US bond prices reflecting an increased default risk premium. The three-month US bond rate has risen significantly due to its proximity to debt ceiling risks and reached a new high since 2001 at 5.318%. In contrast, one-month US bond rates have fallen due to hedging and substitution demand, reaching a new low since October last year at 3.2%. This makes it clear that there is an upward trend in yields for bonds with longer maturities such as March.

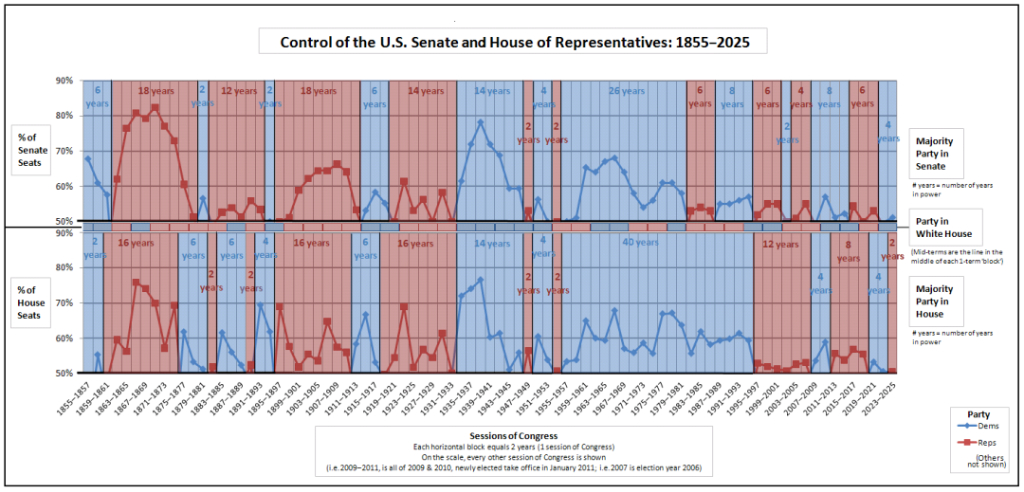

The tug-of-war between both parties remains routine politics; Biden met with Republican leader McCarthy at the beginning of February but failed to reach any agreement on raising the debt ceiling issue; On April 19th McCarthy announced "Limit Save Growth Act of 2023", proposing suspending raising debt limit until end-March next year while requiring significant cuts in government spending and reducing budget deficits by USD4.5 trillion over ten years which clearly contradicts Biden administration’s commitment towards expenditure thus facing oppositions.

In fact, reaching an agreement between both parties is not difficult, it is crucial during this process that each party tries their best to gain more benefits.

What happens if America defaults?

The rising risk of default may prompt some investors to transfer funds to international stocks and foreign government bonds. At the same time, potential defaults may also lead to quality evasion and push down bond yields.

In most cases over the past decade, the repeated legislative deadlock on raising debt ceilings has been resolved without affecting markets; market volatility mainly comes from reactions between both parties' tug-of-war. When the government and Congress are controlled by the same party, there is a higher likelihood of reaching an agreement in the end. However, currently due to Republican control of Congress, investors fear that their slight advantage in Congress could make it more difficult to reach a compromise. Regardless of how this debt ceiling tug-of-war ends up, it will inevitably cause periodic liquidity tightening which affects monetary supply, fund liquidity and asset pricing.

At the same time, we should also pay attention to extreme situations such as 2011 when expectations for raising debt ceilings led to a shutdown; prolonged deadlock prompted Standard & Poor's first downgrade of US credit ratings causing financial market turmoil. During this crisis period in 2011, S&P500 fell by 15%, while those stocks with highest dependence on federal spending plummeted by 25%.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.

- Ericdao·2023-04-24TOPAs per the saying, sell in May n go away. Time for a vacation [LOL] [Miser] [Cool]3Report

- YueShan·2023-05-11okLikeReport

- Stockkid·2023-04-25yyyLikeReport

- CYKuan·2023-04-25[Miser]LikeReport

- lyj1999·2023-04-24ooo2Report