4.2% Dividend Yield and 7-10% Growth for Comstock Resources

- 4.2% dividend yield.

- Growing production reached a record high of 1,400 MMcf/day.

- Sustainable EPS and FCF (Free Cash Flow) growth.

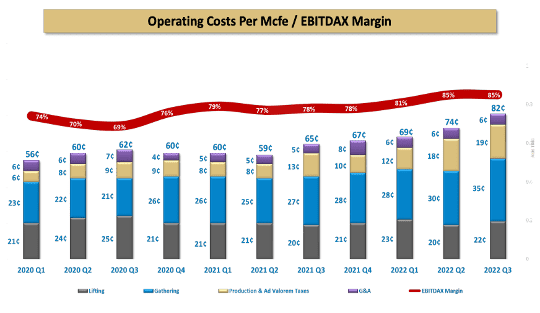

- Lowest-in-the-industry cost structure which helps generate 80% EBITDA margins.

- Huge FCF growth of 218% to $286 million for 3Q22.

- Delevering program to reduce Debt-to-EBITDA to 0.9x.

Investment Thesis

Comstock Resources$Comstock Resources(CRK)$ is a Haynesville Basin pure-play natural gas producer closely located to the Gulf Coast corridor and near several large LNG (Liquified Natural Gas) terminals. CRK operates 1,600 wells across 372,000 acres with an average lateral length of 8,520 feet.

In 3Q22, CRK generated the highest quarterly free cash flow in the company’s history, amounting to $286 million in FCF, which is $1.92 per share. CRK additionally operates the industry’s lowest operating cost structure, which drives its very high 80% EBITDA margin. By FY23, CRK could surpass $1 billion in yearly free cash flow.

Due to its high FCF generation, growth, and low costs, we believe that CRK is a good choice for dividends and capital appreciation.

Estimated Fair Value

EFV (Estimated Fair Value) = E24 EPS (Earnings Per Share) times PE (Price/EPS)

EFV = E24 EPS X P/E = $4.25 X 5.0 = $17.60

We have used a low-end PE within the 4-10x range that oil and gas exploration companies usually fall. However, with its growth, CRK could easily trade at the high end.

| Comstock Resources (CRK) | E2023 | E2024 | E2025 |

|---|---|---|---|

| Price-to-Sales | 1.3 | 1.2 | 1.2 |

| Price-to-Earnings | 2.3 | 3.3 | 2.7 |

Operations

Oil and gas sales increased 76% year over year, including realized hedging losses. Production was at 29 MMcf/d (Millions of Cubic Feet per day) of Natural gas. While this is only a 1% increase year over year in production, far more favorable pricing environment allowed much better financial results.

CRK is an advantageous geographic location, with direct access to gulf coast markets, selling approximately 70% of natural gas in the local geographic area. This includes 15% of production is directly sold to LNG shippers.

For the first 9 months of FY22, the average lateral length of wells was 9,797 feet. Total drilling and completion costs over the same period were $652.6 million. 4Q22 guidance is expected to be higher than the yearly average of 1,400 Mmcf/d, at approximately 1,470 Mmcf/d. All in costs are expected to be equivalent to FY22, which were $1.63 per Mcf (thousands of cubic feet). Well-level cash operating costs are $0.82 per Mcf.

Natural Gas Prices

Freeport LNG terminal being closed after an explosion damaged it over the summer has hurt export volume and US domestic natural gas pricing. The Freeport terminal accounts for around 20% of US LNG Exports. While re-opening was expected to restart in early February,the two first loads have been canceled.As a result, the prevailing sentiment now is that Freeport will not be at fullexport capacity again until 2H23.

We expect natural gas prices to recover by the end of this year, 2023. We estimate a price at or above$5.00/MMBtu with seasonal surgesas the weather gets colder in the latter part of the year. Global demand for LNG is surging but growth in LNG transport capacity will be limited in comparison toprevious years.

As a result, FY23 expansion to the global LNG chain is expected to be the lowest since 2013, adding only 1 Bcf/d in capacity. At the same time, domestic consumption of natural gas is expected to surge to record highs in January of 2024. The EIA estimates a domestic demand of 50 Bcf/d of natural gas as it remains roughly 40% of US electricity generation in 2024.

US LNG is in demand as a result of the European Energy Crisis. LNG exports have reached global highs, with an average of 11.8 Bcf/d (billion cubic feet per day). This is a 10% increase from 2021 and a 70% increase from 2019. In January of FY23,Europe experienced historically high winter temperatures, significantly dampening natural gas demand.

This dampening pushed gas prices back down to what they were before the invasion of Ukraine. However, LNG exports are nonetheless expected to increase yet again as the war in Ukraine drags on and as an additional 8-10 Bcf/d of US LNG capacity comes online by 2026. This demand should create a strong backdrop for natural gas prices. The US has also experienced a warm winter and lower-than-normal heating degree days.

Financials

In 3Q22, CRK generated the highest quarterly operating cash flow in the company’s history, amounting to $286 million. This increase in FCF allowed CRK to retire $250 million in debt and reduce leverage to under the 1x debt-to-EBITDA. The remaining debt on the books matures in 2029.

Limited hedging of only 50% of production and favorable pricing allowed CRK to participate in the natural gas price surge midyear. In 3Q21, the average realized price was $3.79 per Mcf. In 3Q22 this was $7.72 per Mcf. Year over year, FCF increased by 218% and EPS by 237%. However, pricing now is much lower than the middle of the year and FCF will probably decline in 2023.

Risk

Risk

Price is the most glaring risk as the natural gas price per MCF has fallen to an unfavorable level below $3. If the price were to stay at these levels as hedges roll off, FCF would get crushed resulting in slow or no debt repayment and potential dividend cuts.

Historically when companies had high prices and lots of cash flow they invested heavily and with leverage. The past couple of down cycles bankrupted lots of companies and made the survivors more conservative. Hence in the aggregate, there is not enough capital going to development, meaning supply will not overshoot demand and high prices are more sustainable.

An adverse regulatory environment has also starved the industry of capital. Higher prices are the result and will make the industry less boom and bust. Dividend payments instead of Capex are drawing the ire of Washington but are favorable to shareholders as the use of capital for dividends makes high prices more sustainable and thus the dividends more sustainable than past cycles.

Competitive Comparisons

$Southwestern(SWN)$ $Ranger Oil Corporation(ROCC)$ $Ovintiv Inc.(OVV)$ $Civitas Resources(CIVI)$

| Comstock Resources (CRK) | Chesapeake Energy (CHK) | Southwestern Energy (SWN) | Ranger Oil (ROCC) | Ovintiv (OVV) | Civitas (CIVI) | |

|---|---|---|---|---|---|---|

| Dividend Yield (FWD) | 4.20% | 2.60% | 0.00% | 0.71% | 2.16% | 3.08% |

| Price-to-Earnings (FWD) | 3.90 | 6.89 | Neg | 4.05 | 4.12 | 4.71 |

| Price-to-Sales (TTM) | 0.82 | 0.75 | 0.40 | 0.83 | 0.84 | 1.49 |

| Price-to-Book (TTM) | 1.72 | 1.62 | 4.15 | 1.83 | 1.76 | 1.05 |

| Price-to-Cashflow (TTM) | 2.29 | 3.12 | 2.15 | 1.04 | 3.09 | 2.7.0 |

| Return on Total Capital (TTM) | 35.63% | 26.17% | 19.30% | 22.68% | 25.13% | 26.81% |

https://buildingbenjamins.com/stock-thoughts/4-2-dividend-yield-and-7-10-growth-for-comstock-resources/

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.

- Helen1229·2023-02-13👍🏻👍🏻👍🏻👍🏻👍🏻👍🏻12Report

- xiaobaii·2023-02-13like & comment please9Report

- AricLo·2023-02-16thanks for sharingLikeReport

- ongcjeric·2023-02-17HhLikeReport

- Cory2·2023-02-16ThanksLikeReport

- Simonnov·2023-02-16IcLikeReport

- HHHA·2023-02-16Like!LikeReport

- JTC·2023-02-16ok1Report

- HENRYCSC·2023-02-14K1Report

- Maverick253·2023-02-14Ok1Report

- eeth·2023-02-14👍👍1Report

- BlueDragon·2023-02-14ok1Report

- Yor·2023-02-14Good.. 4.2%LikeReport

- Magdalene89·2023-02-14Latest1Report

- Worpeng2002·2023-02-14ok1Report

- JIll·2023-02-14LIIE3Report

- 有梦想才是动力·2023-02-14[贱笑]5Report

- Fayedea·2023-02-13Great4Report

- HighFly168·2023-02-13[Anger]4Report

- LimCI·2023-02-13👍5Report