Tech Earnings: Who would like to hold SNAP?

$Snap Inc(SNAP)$ just got another miserable Q4 earnings again. Its shares tumbled 13% after hours after its fourth-quarter earnings report showed flat revenues and the company predicted a first-quarter drop of 2-10% in sales.

Since the whole communication industry is not a good choice for long-term holding, how should we invest SNAP?

Q4 Earnings Takeaways

The stagnation of revenue growth makes the growth of users inefficient.

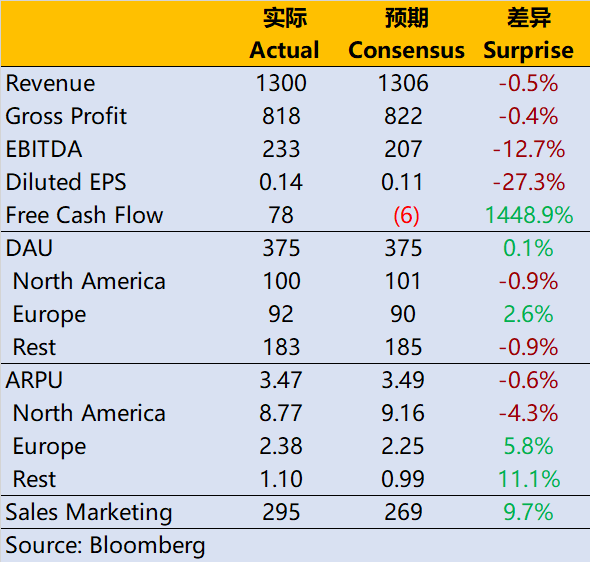

- Revenue 1.3 billion US dollars, an flat YoY of 0.14%, which was slightly worse than the consensus of 1.306 billion;

- EBITDA US $233 million, a year-on-year decrease of 29%, higher than the market expectation of US $207 million;

- DAU was 375 million, up 17% year-on-year, which was flat with the expected 374.7 million.

Why miss again??

Unlike $Netflix(NFLX)$'s snvestors, who pay more attention to subscriptions. Investors of SNAP are not sensitive to active users anymore. Even DAU is nearning 400 million, with a growth rate of 17%, investor didn't buy it.

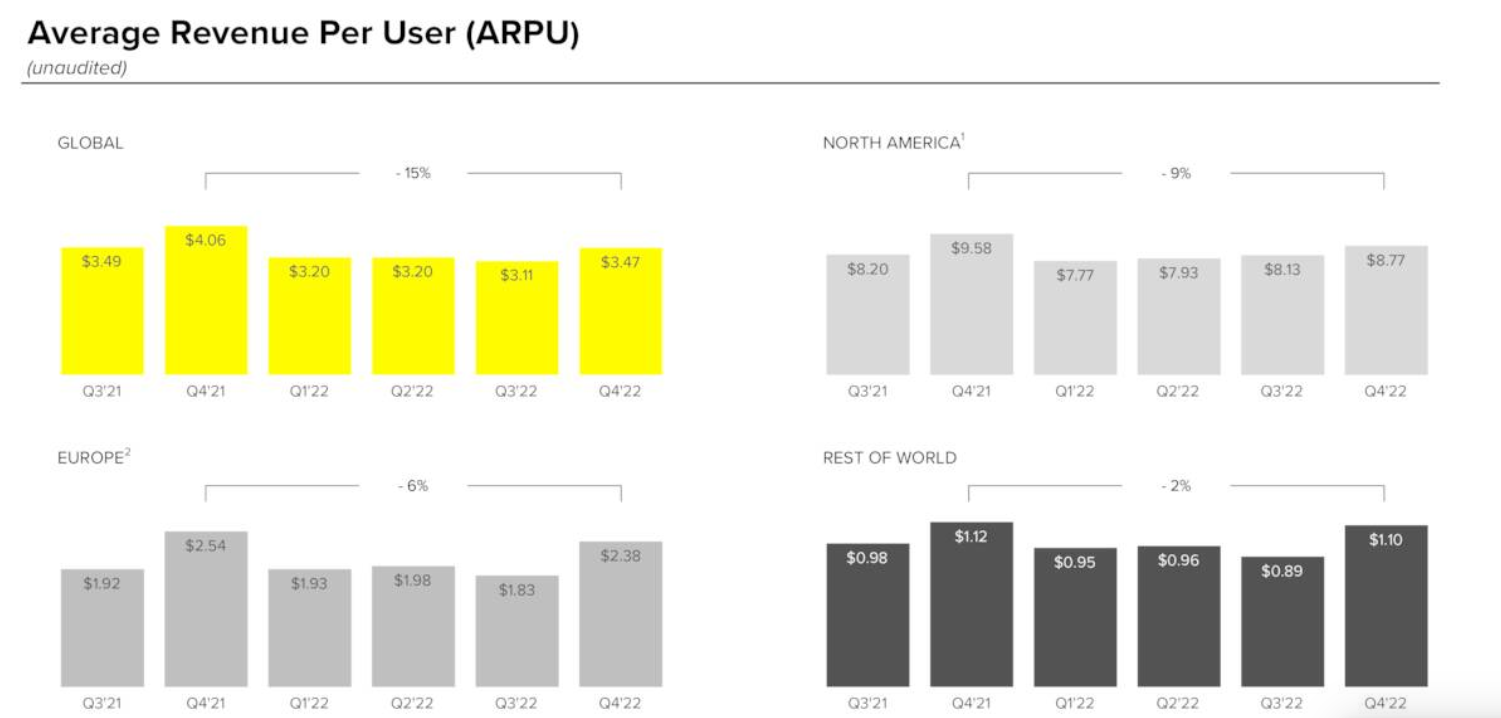

Market pays more attention to its monetization ability.

In the rapid growth period, profit margin was not very important, as long as the Top Line grew rapidly (even reaching triple digits year-on-year). Since investors' risk appetite changes, the ability of profits counts.

Companies of ads industry should have higher profit margins, such as Facebook.

Due to high marketing and administrative expenses, expenditures are still greater than market expectations. In other words, there is still room to continue to reduce costs.

Stagnant revenue is probably the most worrying thing for investors.

- Recession expectation rises, the advertising market has a serious impact;

- Unique revenue structure makes it no surprise for future growth;

- Vulnerable in industrial competition, short video could grab the market share easily.

SNAP did not give the next Q1 guidance, and the executives revealed in the telephone conference.Revenue may decrease by 2-10% year-on-year.This is a rather pessimistic signal.

What should investors pay attention to?

SNAP is an active trading ticker, but more in individuals.

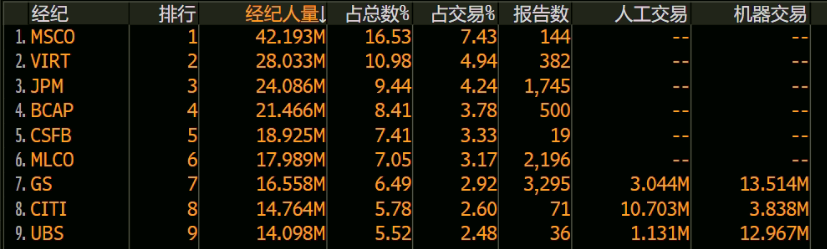

Its largest institutional investor, which many investors may not have noticed, is actually $TENCENT(00700)$, who holds 17% of the shares, in addition, private equity funds holds a lot. But the banks, for example$Goldman Sachs(GS)$,$JPMorgan Chase(JPM)$,$State(STT)$ does not have high proportion holdings.

According to Goldman Sachs and UBS,The proportion of machine transactions is large. This shows that a high proportion of quantitative investors are trading, which is also a key factor for SNAP's good liquidity.

At the same time, individuals could have disaddvantages dacing those quants.

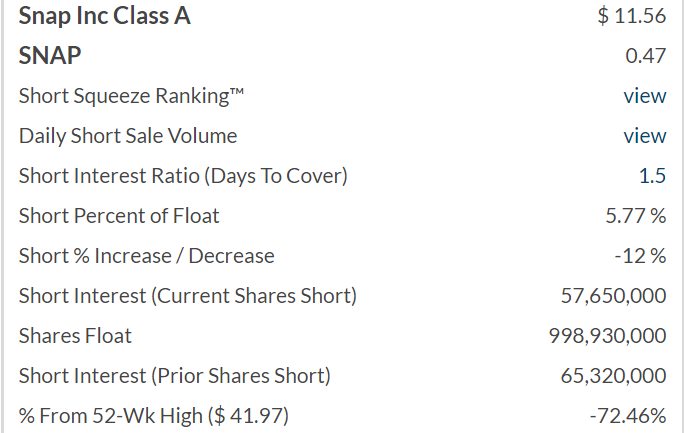

As for short selling, the recent short interest is 5.7%, which cannot be said to be very high, but it is not very low. However, it has retreated from the high point by 72%, and there is still short selling in this proportion, indicating that short sellers still feel that the company is overvalued to a certain extent, or that they are not optimistic about the future.$Meta Platforms, Inc.(META)$It is also this industry, and there are many short positions, but the short ratio is about 1.2%.

Besides, active investors like Cathy Wood, just close almost all positions last month. If active investors don't want to hold it, who will do?

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.

Interesting