Will SaaS Stocks Rebound?

SaaS has been in the spotlight for years, with the preference of both primary and secondary market. Especially for benchmarks, $Salesforce.com(CRM)$, $Snowflake(SNOW)$ should be the valuation fundamentals, now, half down.

Their quarterly results has proven something.

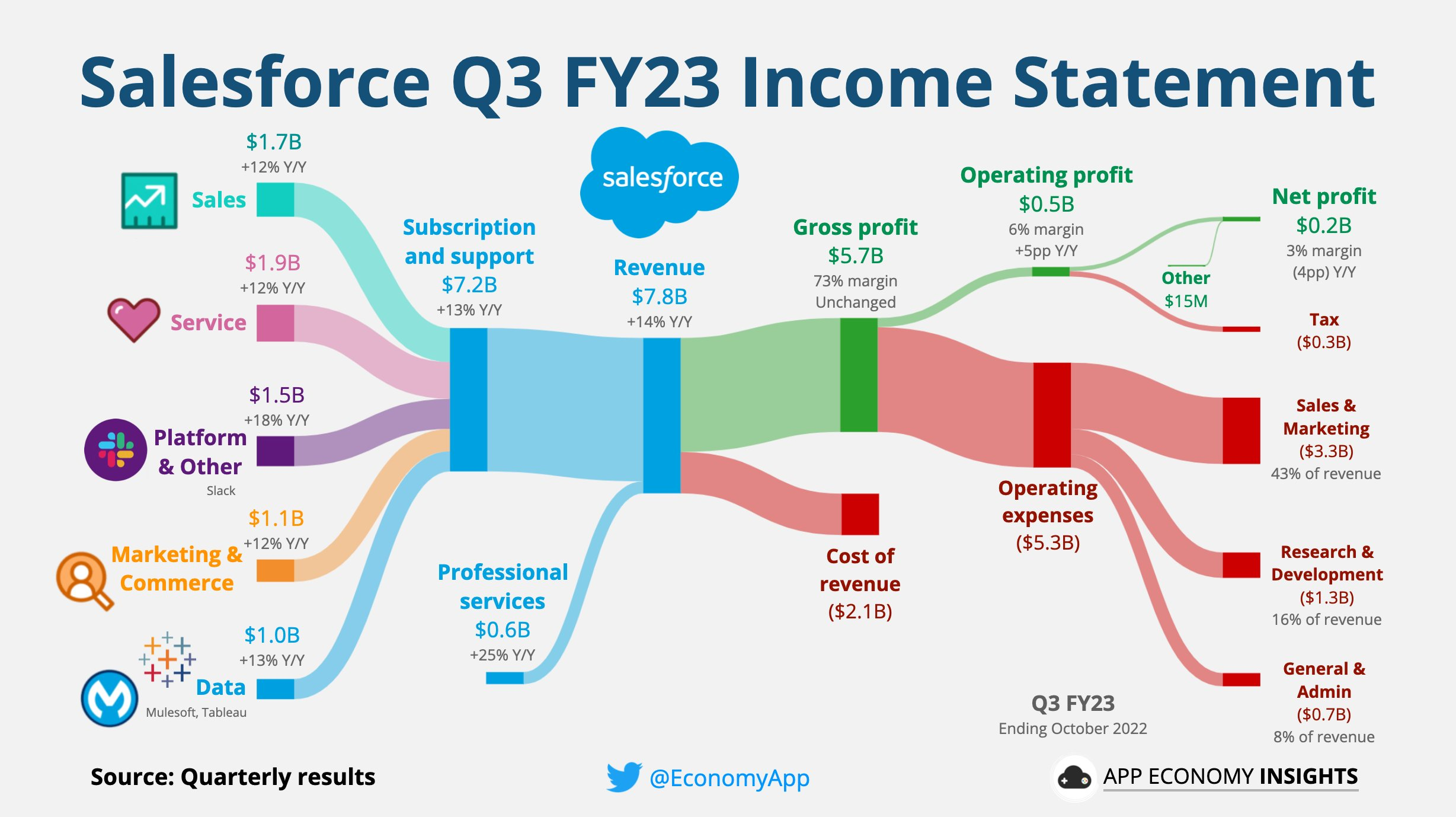

$Salesforce.com(CRM)$

Total revenue in Q3 quarter was US $7.84 billion, up 14% year-on-year, which was the same as expected. Excluding the impact of exchange rate changes, it increased by 19% year-on-year, which was higher than the market expectation of 17.4%. Among them, the subscription and support business revenue was 7.233 billion US dollars, a year-on-year increase of 13%, slightly lower than the market expectation of 7.29 billion US dollars; Revenue from professional services and other businesses was US $600 million, up 25% year-on-year, higher than the market expectation of US $570 million.

It can be seen that the overall income still exceeds expectations, but strong dollar almost erasing the surprise of revenue expectations.

More importantly, the growth of subscription business began to slow down. Among the four major items, the platform has the lowest impact.Marketing has suffered most.This also echoes the fact that companies in the consumer and technology industries are beginning to cut costs.

In the same period, GAAP's net profit was US $210 million, down 55% compared with US $468 million in the same period last year, but better than expected by US $208 million.

There are two things that worry the secondary market. One is the guidance for the Q4 fiscal quarter. The revenue side is 7.93 billion-8.03 billion US dollars, and the median is lower than the market expectation of 8.01 billion; The other is that co-CEO Bret Taylor will leave at the end of January. The sudden departure of the veteran who has been with him for 6 years naturally makes the market afraid.

As a result, CRM plunged 8.3% in December 1.

$Snowflake(SNOW)$

As the leader of PaaS, SNOWFLAKE is the key infrastructure. Q3's total revenue was US $557 million, up 67% year-on-year, higher than the market expectation of US $540 million. Among them, product revenue was USD 523 million, up 67% year-on-year, higher than the market expectation of USD 507 million.

In terms of profit, the diluted loss per share was US $0.63, compared with the net loss of US $155 million in the same period last year, while the adjusted earnings per share was US $0.11, which was higher than the market expectation of US $0.04.

At the same time, the company had 7292 customers at the end of Q3, which was higher than the market expectation of 7212.The net dollar retention rate was 165%, which was higher than the expected 156%.

SNOW's Q3 data is very bright as a whole, and it exceeded market expectations after lowering its guidance and slowing down its growth rate. However, the guidance for the next Q4 has further slowed down. The company expects the product revenue range to be 535 million to 540 million US dollars, an increase of about 49%-50% year-on-year, while the market generally expects it to be 553 million US dollars. Therefore, the market also gave a 14% decline.

$CrowdStrike Holdings, Inc.(CRWD)$

Coincidentally, CRWD, the leading network security company that announced its financial report last week, also fell sharply because of the guidance of lowering Q4. The company expects its fourth-quarter revenue to be between $619.1 million and $628.2 million, which is lower than the market expectation of $634.2 million.

At the same time, the company's Falcon progress is slightly slower than its peers, and terminal security has been facing$Palo Alto Networks(PANW)$And$Datadog(DDOG)$'s competition

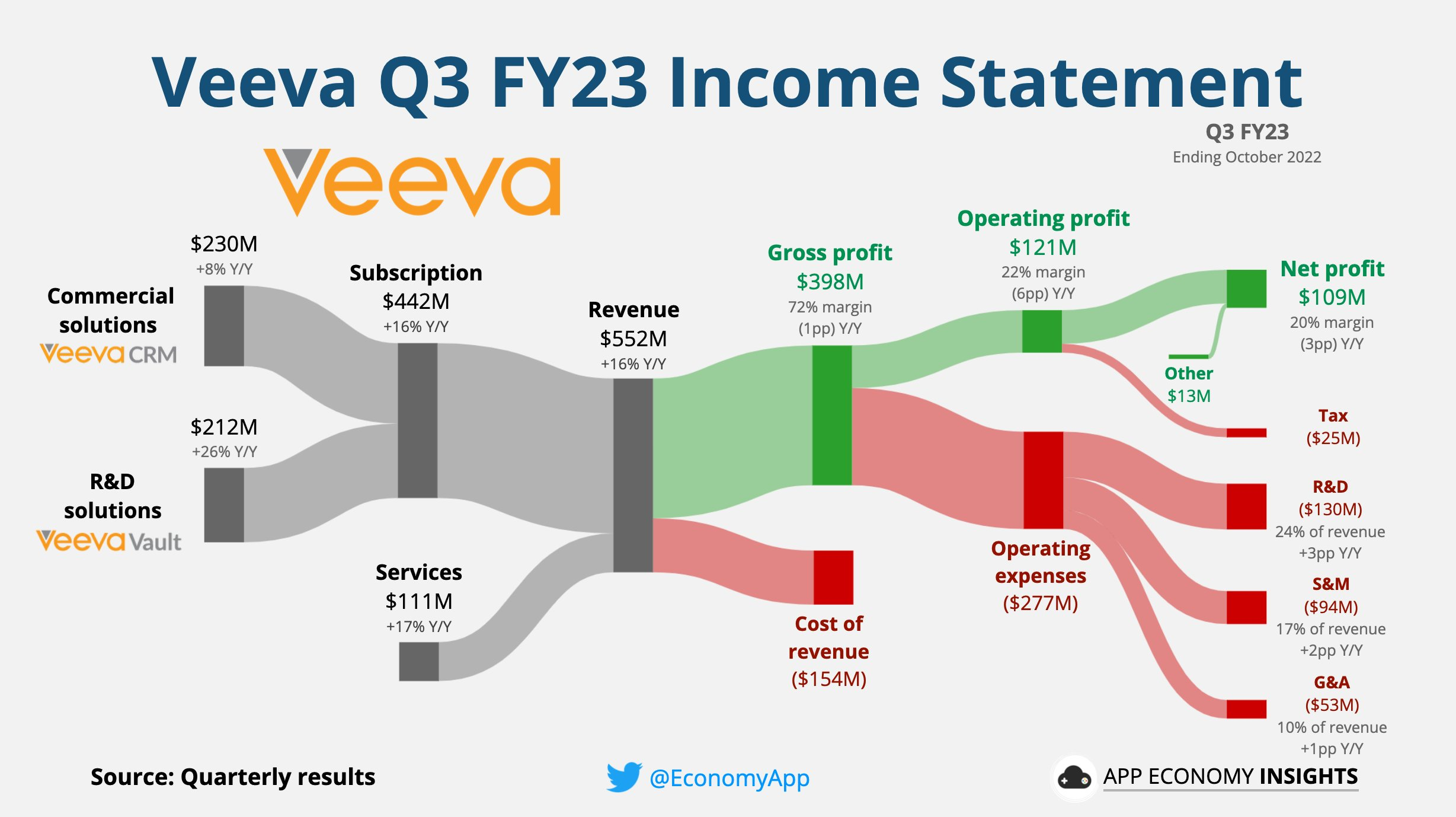

$Veeva(VEEV)$

The same is true of VEEV, a SaaS company of life sciences. In Q3, Double Beat earned $552 million, slightly exceeding expectations, and EPS was $1.13, higher than expected $1.07. But Q4's guidance of $552 million was slightly lower than the market expectation of $557 million.

What are the main reasons for the plummet??

Slowing growth and paying attention to operation also mean that these growth companies have shed the aura of "high growth", so funds with high risk appetite will naturally withdraw.

We all have one thing in common, that is,After lowering the Q4 revenue guide, but raised the profit guides.

CRM's median EPS guidance is $1.36, and the market expects $1.34; SNOW's operating profit margin increased from the previous 2% to 3%, while CRWD's EPS guidance was 0.42-0.45 USD, which was higher than the market expectation of 0.34 USD.

This shows that even industry leaders have begun to improve operational efficiency, moving from the previous expansion to efficiency, from growth to value.

Is it possible that risk-on mode return again?

Yes.

Recently, another SaaS company rose sharply after announcing its financial report, which was also considered by the market as a risk "replenishment".

$Okta Inc.(OKTA)$It is the first stock of ID authentication platform, which fell by 33% when Q2 performance fell short of expectations and guidance was poor this year, but it also rose by 26% after Q3 performance exceeded market expectations, Q4 was raised and guidance in 2023 was raised.

Although it can't bring the stock price back to its original position once and for all,However, it also proves that the market still has demand for growth stocks with high risk appetite.

Generally speaking, SaaS industry is the vane of growth stocks in recent years, and the performance of SaaS leading companies is the guide of industry strength. At present, the market is not only leaving the market to wait and see, but also betting and rebounding. What is more important is to look at the company's performance expectations and the final landing situation.

As more and more speculative chips are withdrawn, more risk-on funds can return.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.

- jethro·2022-12-03thanks for sharing23Report

- tancheeyuen·2022-12-03[微笑] [微笑]21Report

- Adestein·2022-12-03Like all those stocks9Report

- JeffLeeyt·2022-12-04thanks for sharing5Report

- SirBahamut·2022-12-03My SaaS all got burned :(9Report

- MO75·2022-12-04where to get these chart?6Report

- ValuInvestor·2022-12-02These companies have solid business fundamentals and will be around after any recession that might appear. They will likely return to their hyper growth states in 18-24months5Report

- Richest Princess·2022-12-04wow thanks6Report

- LohYK·2022-12-04nice sharing4Report

- An Long·2022-12-04[smile] [smile]4Report

- yaozong7·2022-12-04In salesforce we trust?4Report

- Cklew·2022-12-04thanks for the info packed post [Like]4Report

- CharlesW·2022-12-03Those with FCF should be able to survive and grow4Report

- Quantum Leap·2022-12-05Confirm up on lah. my ceca and angmo manyers can kiss my arse goodby by then. All in shoe hand2Report

- GREEDisGOOD·2022-12-04thanks for sharing3Report

- BabokSong·2022-12-04thanks for the info2Report

- dhf1354·2022-12-09coolLikeReport

- NicNic·2022-12-08IkLikeReport

- sst9383·2022-12-08。1Report

- Allen Chin·2022-12-07666LikeReport