Wil UPST break-even be in advanced?

$Upstart Holdings, Inc.(UPST)$ surged nearly 40% after hours, bringing hope for second-tier growth to turn the tide.

In addition to Q1 financial results slightly exceeding expectations, the company unexpectedly released Q2 guidance indicating that it will achieve "break-even" ahead of schedule, while the market generally expected this to happen in Q3 or Q4 of this year.

Regarding Q1 performance, although revenue reached $103 million, slightly higher than the market's expected $100 million, GAAP net loss was $129 million overall and consistent with market expectations. The company's adjusted EPS was a loss of $0.47 per share, slightly higher than the expected loss of $0.82 per share.

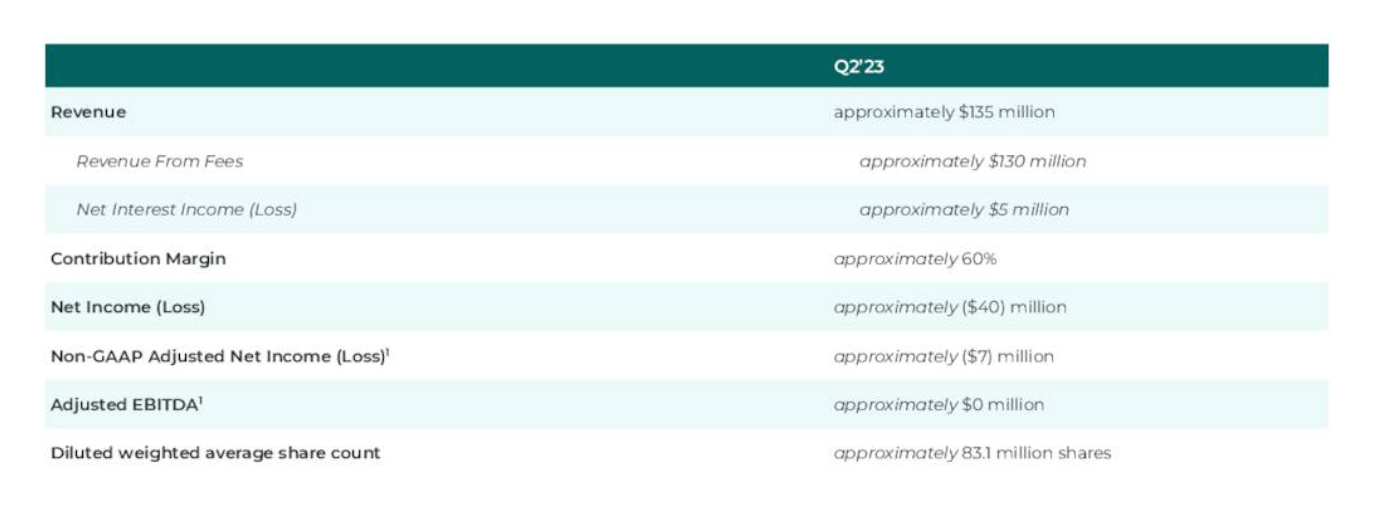

The biggest highlight is still on the conference call where they stated that Q2 revenue will reach $135 million which is higher than current market expectations of $126 million and adjusted EBITDA will be positive meaning they are turning losses into profits earlier than anticipated.

We believe that since investors currently expect high-growth stocks like UPST to turn losses into profits early; once achieved there may be some reward from the market. Previously several major Wall Street banks had low expectations for UPST even after their Q1 earnings report and rated them as underperforming or sell-off stock.

Currently high-interest rates are not favorable for lending businesses but instead surprisingly helped increase UPST’s forecasted earnings. As an intelligent intermediary company they do not directly hold debt but help enterprise customers increase risk control levels and reduce default rates.

Regional bank defaults may provide an opportunity for companies such as UPST because more banks and other financial institutions need to increase their own risk control levels compared with developing their own systems; UPST provides a more direct product at lower cost.

Similarly Fintech newcomers $SoFi Technologies Inc.(SOFI)$ $Affirm Holdings, Inc.(AFRM)$ , $LendingClub(LC)$ and other companies are more affected by interest rates.

In terms of valuation, UPST's EV/Sales TTM is 2.02x, slightly higher than the industry average of around 1.6 times but lower compared to SOFI at 4.65x and AFRM at 2.75x.

However, overall for a Fintech company investors still value profitability; when it can truly convert into positive cash flow and continuously create returns for shareholders it will attract institutional investors to enter the market.

Currently Wall Street's ratings and target prices for UPST are not optimistic.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.

Wall Street banks underestimated UPST, but now they might have to eat their words as profits roll in

The conference call was a game-changer! UPST's Q2 revenue is projected to surpass market expectations

UPST exceeded expectations with Q1 results and surprised everyone with early break-even projections for Q2

UPST surged 40% after hours! Finally, some hope for second-tier growth to make a comeback