How does the "tight credit cycle" affect assets after interest rates peak?

After the release of the lower-than-expected CPI data for April in the United States last Wednesday, the market further believed and priced in the possibility of a pause in rate hikes in June. This means that after what was previously estimated to be the final rate hike in May this year, this rate hike cycle will come to an end.

Under tight monetary policy, credit tightening deserves more attention from investors.

The relationship between monetary policy tightening and credit tightening often follows one another. In addition, since the US banking crisis, both regulation (further scrutiny of systemic risk) and banks (tightening lending conditions) have accelerated credit tightening processes. Therefore, market focus on credit tightening cycles will determine key asset trends in future.

From a bank lending perspective,

the Federal Reserve's Senior Loan Officer Survey shows that since March bank loan standards have tightened further as expected. Large banks are more concerned about deteriorating credit quality expectations, declining collateral values and reduced bank risk tolerance; while small-to-medium-sized banks express greater concerns over financing costs for banks' operational procedures and deposit outflows.

From an enterprise financing perspective,

large enterprises usually have more financing channels to cope with tighter bank credits; for example, when bank loans decrease large enterprises can finance through issuing bonds or other methods instead. Multinational corporations can even adjust their debt levels by placing more liabilities into low-interest-rate countries such as Japan while putting more assets into high-interest-rate countries such as America. However small-to-medium-sized enterprises are relatively more passive, as bank loans remain their main source of financing.

Interestingly, there has been an improvement in consumer lending on the credit side.

Why has there been an improvement in consumer credit demand? The consensus is that increased consumption credit, auto loans and other loan demands have risen. We believe that the impact of rate hikes on the US consumer economy was immediately apparent; rising living costs for residents led to greater demand for consumption-side loans. At the same time, strong labor market conditions and continuous wage growth also support US consumer spending without increasing overall household leverage.

In addition, extra savings from residents due to "water release" since the pandemic still have a surplus. According to estimates by the San Francisco Fed, from when the pandemic began until June 2021 American residents accumulated up to $2.1 trillion in excess savings; by April 2023 households had withdrawn $1.6 trillion but still had $500 billion left unused. Based on current withdrawal rates this can still sustain household consumption until Q4.

All these factors can support enterprise sales and profit levels.

Therefore at current speeds before Q4 these two factors will continue supporting corporate performance: one is expected slowing inflationary pressures which will further reduce enterprise cost expenditures; another is excess deposits not yet used by households.

Of course when it comes down to different industries,

for less price-sensitive industries with lower elasticity if they benefit from price increases during this inflation cycle while industry supply-demand remains balanced and company inventory levels are healthy then they may continue seeing improved profit margins; however for more price-sensitive industries with higher elasticity or those who did not benefit from price increases during this inflation cycle or even suffered losses due to rising prices may continue under pressure.

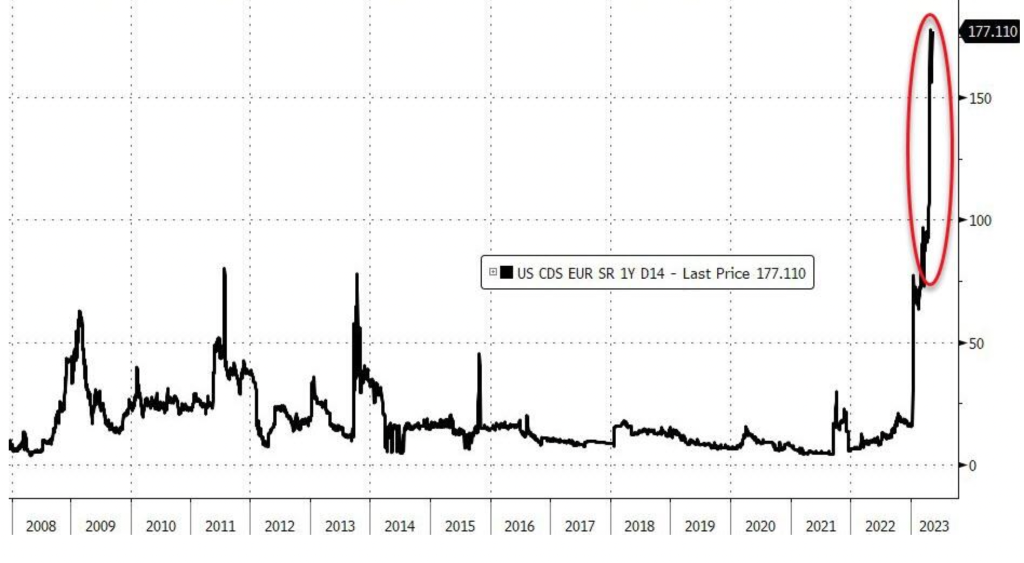

Correspondingly, one-year US CDS hit a historical high point and panic sentiment in financial markets rose slightly.

Last week saw outflows of USD 2.235 billion from US stocks continuing while Europe continued its outflow of USD 1.123 billion; Japan's stock market turned into an inflow of USD 1.109 billion and emerging markets continued to see an inflow of USD 4.3 billion, among which A-shares saw a net inflow of USD 0.039 billion from active foreign investment while Hong Kong stocks saw overseas capital inflows of USD 0.094 billion.

From the industry perspective, technology stocks had a weekly net inflow of $3 billion while financial stocks continued their outflow with $2.1 billion, becoming the most obvious sector for last week's flow in and out.

This week's focus is on concerns over debt ceilings, beware that the market may be too optimistic: "Will panic sentiment rise again? What impact will US debt ceilings have on the market?"

After the release of the lower-than-expected CPI data for April in the United States last Wednesday, the market further believed and priced in the possibility of a pause in rate hikes in June. This means that after what was previously estimated to be the final rate hike in May this year, this rate hike cycle will come to an end.

Of course, although the market is optimistic about expectations of a "rate cut" starting from September, core CPI has been hovering around 5.5% for four consecutive months and its three-month annualized value is still as high as 5.1%, which is close to 5%. This indicates that there is still significant stickiness. Core CPI from May to June may determine whether there can be a smooth transition towards September.

Under tight monetary policy, credit tightening deserves more attention from investors.

The relationship between monetary policy tightening and credit tightening often follows one another. In addition, since the US banking crisis, both regulation (further scrutiny of systemic risk) and banks (tightening lending conditions) have accelerated credit tightening processes. Therefore, market focus on credit tightening cycles will determine key asset trends in future.

From a bank lending perspective,

the Federal Reserve's Senior Loan Officer Survey shows that since March bank loan standards have tightened further as expected. Large banks are more concerned about deteriorating credit quality expectations, declining collateral values and reduced bank risk tolerance; while small-to-medium-sized banks express greater concerns over financing costs for banks' operational procedures and deposit outflows.

From an enterprise financing perspective,

large enterprises usually have more financing channels to cope with tighter bank credits; for example, when bank loans decrease large enterprises can finance through issuing bonds or other methods instead. Multinational corporations can even adjust their debt levels by placing more liabilities into low-interest-rate countries such as Japan while putting more assets into high-interest-rate countries such as America. However small-to-medium-sized enterprises are relatively more passive, as bank loans remain their main source of financing.

Interestingly, there has been an improvement in consumer lending on the credit side.

Why has there been an improvement in consumer credit demand? The consensus is that increased consumption credit, auto loans and other loan demands have risen. We believe that the impact of rate hikes on the US consumer economy was immediately apparent; rising living costs for residents led to greater demand for consumption-side loans. At the same time, strong labor market conditions and continuous wage growth also support US consumer spending without increasing overall household leverage.

In addition, extra savings from residents due to "water release" since the pandemic still have a surplus. According to estimates by the San Francisco Fed, from when the pandemic began until June 2021 American residents accumulated up to $2.1 trillion in excess savings; by April 2023 households had withdrawn $1.6 trillion but still had $500 billion left unused. Based on current withdrawal rates this can still sustain household consumption until Q4.

All these factors can support enterprise sales and profit levels.

Therefore at current speeds before Q4 these two factors will continue supporting corporate performance: one is expected slowing inflationary pressures which will further reduce enterprise cost expenditures; another is excess deposits not yet used by households.

Of course when it comes down to different industries,

for less price-sensitive industries with lower elasticity if they benefit from price increases during this inflation cycle while industry supply-demand remains balanced and company inventory levels are healthy then they may continue seeing improved profit margins; however for more price-sensitive industries with higher elasticity or those who did not benefit from price increases during this inflation cycle or even suffered losses due to rising prices may continue under pressure.

Correspondingly, one-year US CDS hit a historical high point and panic sentiment in financial markets rose slightly. Last week saw outflows of USD 2.235 billion from US stocks continuing while Europe continued its outflow of USD 1.123 billion; Japan's stock market turned into an inflow of USD 1.109 billion and emerging markets continued to see an inflow of USD 4.3 billion, among which A-shares saw a net inflow of USD 0.039 billion from active foreign investment while Hong Kong stocks saw overseas capital inflows of USD 0.094 billion.

From the industry perspective, technology stocks had a weekly net inflow of $3 billion while financial stocks continued their outflow with $2.1 billion, becoming the most obvious sector for last week's flow in and out.

This week's focus is on concerns over debt ceilings, beware that the market may be too optimistic: "Will panic sentiment rise again? What impact will US debt ceilings have on the market?"

Last week Treasury Secretary Yellen once again warned about the impact of debt ceiling issues; Speaker McCarthy also stated that there has been no substantive progress in negotiations between both parties and worries about default are quietly rising. Biden told reporters in Delaware on Sunday that he expects to meet with McCarthy on Tuesday. Currently both parties disagree as Republicans demand significant cuts to

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.

- andree·2023-05-20Great ariticle, would you like to share it?LikeReport

- Bel8680·2023-05-16👍👍LikeReport