Should Tencent Q1 Earning make HK Market rebound?

On May 17th, $TENCENT(00700)$ released its Q1 2023 financial report. It's strange that the market was full of hope for this year's recovery in Q1 and saw real evidence, but due to various reasons, it didn't reflect correctly on the secondary market stock price. In this week, tons of blitz investors positive to Q1 earnings rushed into Tencent, and hopefully the result is good.

Overall, Q1 financial report met expectations of being "better than expected". After more than a year of advocating "cost reduction and efficiency enhancement", Tencent has once again demonstrated its strength in "open source".

Revenue reached RMB149.986 billion, far higher than expected RMB147.2 billion with YoY growth rate at 11%, returning to double-digit growth rate since Q3 2021.

Non-IFRS profit also reached RMB32.5 billion with YoY increase at 27%, slightly lower than expected RMB33.5 billion; adjusted diluted EPS also reached RMB3.36 yuan per share level comparable to that in 2020.

Among all businesses, gaming and advertising remained outstanding and surprising with much higher-than-expected results despite analysts' raised expectations based on their knowledge about economic recovery.

Cost reduction and efficiency enhancement are still effective practices implemented by Tencent as marketing expenses decreased by another YoY drop of 13% while marketing expense ratio dropped to 5%. Administrative expenses fell by a first-ever YoY decline of 7.6% which is likely to further decrease.

Without one-time confirmation fees impact, other income decreased from CNY13.1 billion in Q2 last year and CNY8.6 billion in Q4 last year down to CNY900 million this quarter; however joint venture profits were CNY100 million indicating clear signs of overall economic recovery.

AI is not absent but Tencent is not in a hurry to monetize it. Tencent has invested heavily in building AI capabilities and cloud infrastructure to embrace opportunities brought by basic models.

Stock price remains extremely undervalued, but the largest shareholder's reduction still exerts the greatest pressure on stock price.

Investment highlights

Gaming and entertainment are once again gaining momentum with lows already reached.

Q1 value-added service revenue was CNY79.34 billion, 6% higher than market expectations of CNY74.54 billion, among which gaming business revenue was CNY48.3 billion with YoY growth rate at 10.8%, returning to double-digit growth rate again; domestic gaming business grew by 6% to CNY35.1 billion while new game "Dark Zone Breakout" also brought incremental income demonstrating vitality since license resumption; international market game revenue reached CNY13.2 billion with YoY increase at 25%, creating new high for income contribution since Q3 2019 when separate data were first disclosed; overseas game revenue has now reached 38% of local game revenue becoming Tencent Games' "second growth curve". New games such as "Goddess of Victory: Nikkie" and "Triple Match: 3D" performed well overseas in Q1 while Valorant grew steadily.

Of course, Tencent's biggest regret may be miHoYo because besides Genshin Impact's super competitiveness overseas, both Honkai Impact III and Punishing Gray Raven are frequent visitors on the top ten list of global mobile games by revenues where Iron Saga released on April 26th could have generated over RMB100 million on its first day alone worldwide after all these years without any replacement for whole second dimension track following Tencent's irreplaceable advantage in MOBA and FPS categories.

In terms of video streaming platform sector, due to lackluster content in Q1, Tencent Video's paid subscribers decreased by 9% to only 113 million. However, its hit series "The Longest Day in Chang'an" was launched in April and will be reflected in Q2 financial report. Meanwhile, according to Tencent Music's financial report released yesterday, online music revenue increased by a net addition of 5.9 million users on a MoM basis despite YoY decline due to price increases indicating that Tencent Music has started paying more attention to the role of digital music rather than social entertainment as before. Especially under the current macroeconomic situation, audio-visual entertainment is not strong cyclicality so Tencent's performance is still good.

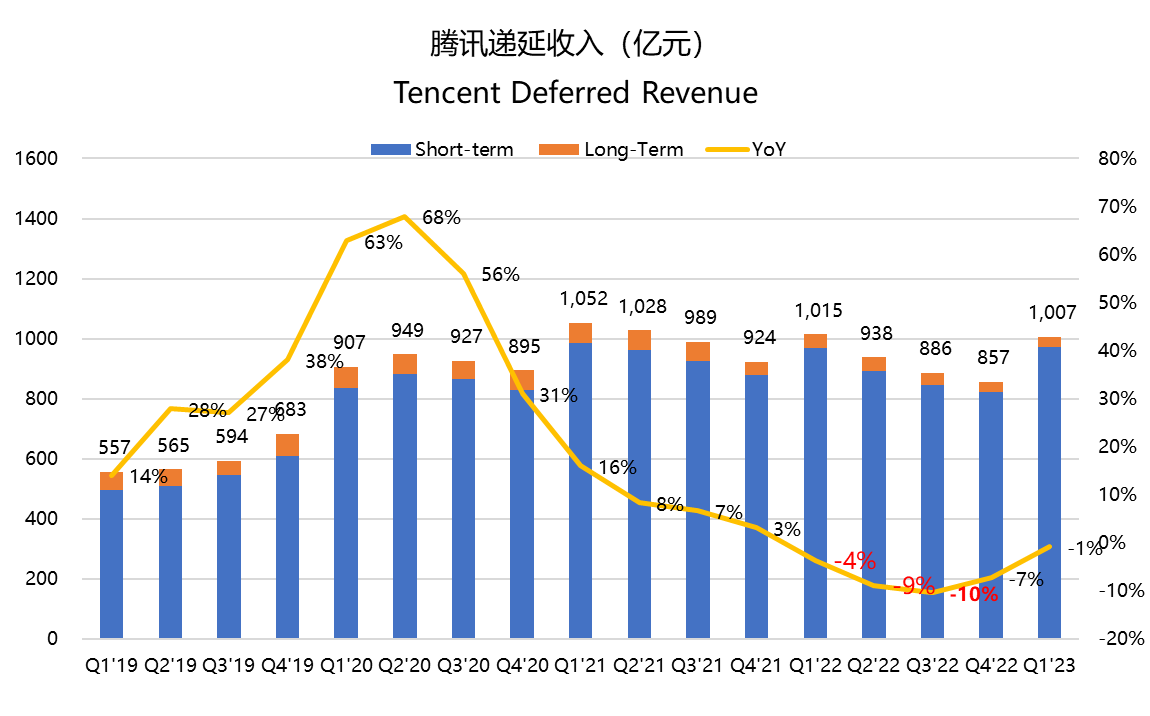

In addition, from Tencent's deferred income perspective, its long-term deferred income has returned to the level at the beginning of 2021 which means there is no need for too conservative expectations for value-added services over next few quarters.

The WeChat ecosystem is the second curve.

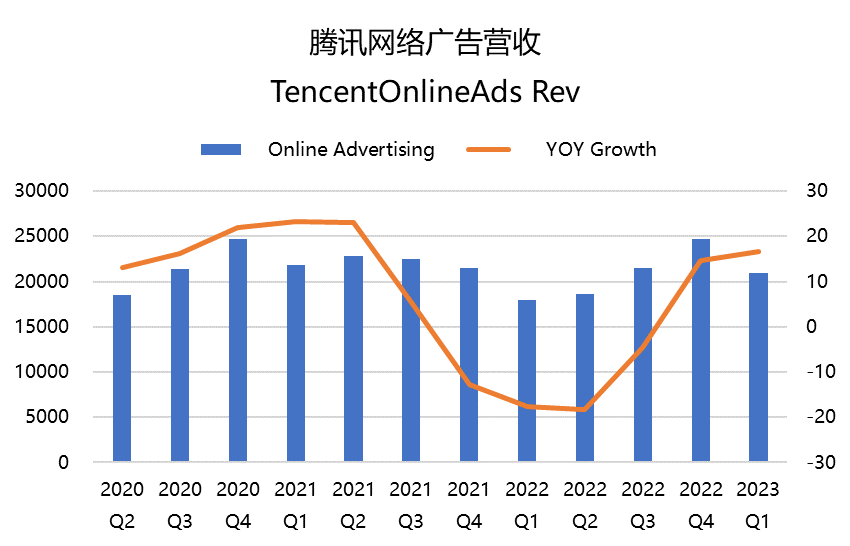

Despite fierce competition with Douyin, the Video Account ecosystem has shown strong growth momentum in the last quarter, with creators who have over 10,000 followers growing three times year-on-year. It's worth noting that Tencent's Video Account has little water content. Therefore, steady expansion of advertising revenue is not surprising. This quarter's advertising revenue was CNY 20.96 billion, a year-on-year increase of 17%, which is basically in line with market expectations.

Meanwhile, after the recovery from the pandemic, there has been an obvious revival in the advertising industry. Of course, Tencent itself has also optimized its strategy and further increased advertisers' efficiency by adding Video Account ads with higher average eCPMs (relative to other short video platforms), converting Video Account content into mini-programs to increase high conversion rate ad inventory and more. As we mentioned before, advertisers are the most sensitive group to economic activity efficiency; therefore releasing commercial potential for Tencent Advertising is also a certain degree of recognition for advertisers on Video Accounts and mini-programs as well as overall value within Tencent's ecosystem - it’s also recognition of Tencent’s channel value. The next step may be promoting e-commerce development.

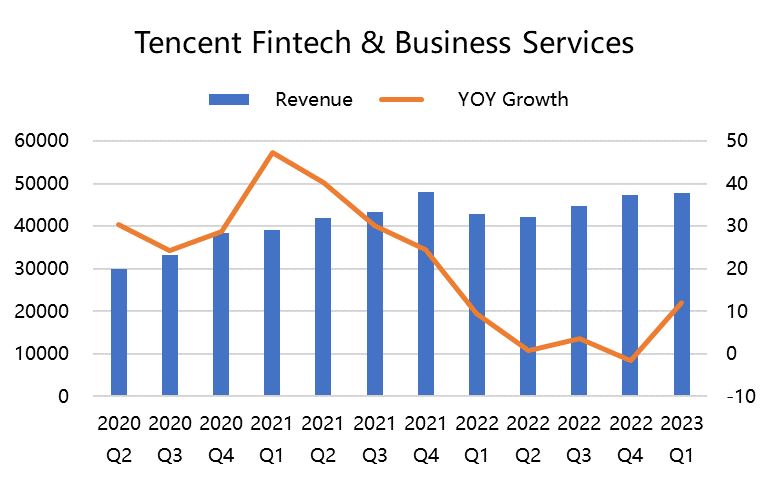

The recovery of offline financial business drives growth while cloud competition becomes normal.

Commercial payment activities grew this quarter along with offline activities’ recovery; total income from fintech and enterprise services reached CNY 48.7 billion YoY up by14%, exceeding market expectations at CNY47.3 billion – indicating that offline commercial activity recovered better than expected.

Cloud service competition is becoming increasingly apparent since expanding overseas presents greater difficulties; currently domestic commercialization remains primary focus for this business area.Tencent Cloud aims to increase monetization capabilities while reducing losses during these two quarters; recent price cuts on some cloud products reflect accelerated commercialization goals too.In addition,Q1 financial reports show that technical services related to Video Account live streaming also brought incremental growth to cloud business. Future monetization growth of Tencent Cloud will still depend on the group's ecosystem.

Profit margins are expected to reach new highs.

Although this quarter did not bring one-time income like selling Meituan and JD.com shares, it is gratifying that the inertia of reducing costs and increasing efficiency continues to boost the company's profit margin.

The company's revenue cost increased by 9% YoY, lower than revenue growth rate at 11%, so gross profit margin further increased to 45.5%, higher than market expectations at 44.0%. Marketing expenses continued to decrease with a YoY decline of 13%; marketing expense ratio has dropped to 5%. We also found that Tencent’s management expenses finally showed a YoY decline of7.6% after rising due overseas expansion in previous periods; this was its first rebound. R&D expenses have also decreased somewhat this period.

Due to the current high interest rate environment in most regions around the world, Tencent's interest expenses and income have increased. Thanks to reasonable asset allocation, its Q1 interest income was RMB 2.96 billion, higher than its interest expenses of RMB 2.65 billion.

In addition, profits brought by joint ventures in this period were RMB 100 million, fully demonstrating signs of other companies' performance improvement after recovery.

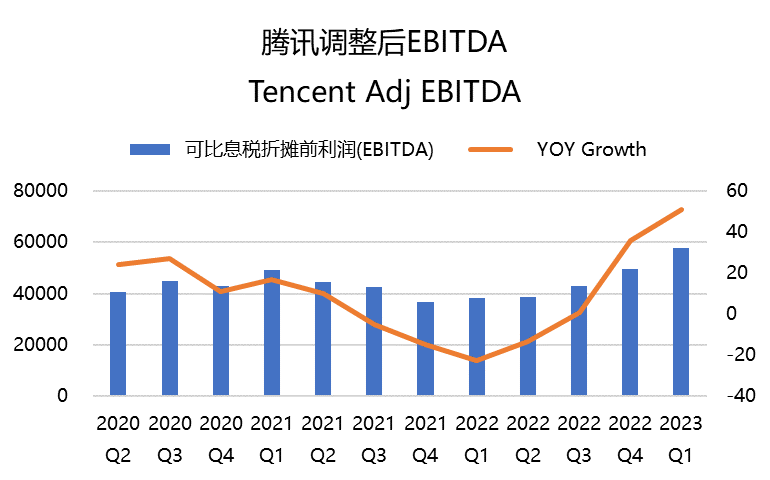

Looking at several profit indicators, comparable profit was RMB 37.9 billion, a YoY increase of 30.5%; net profit for the period was RMB 26.4 billion, a YoY increase of 11%, but adjusted non-IFRS profit was RMB 32.5 billion, a YoY increase of 27%. EBITDA was RMB 52.66 billion, a YoY increase of 37% and an MoM increase of20%; adjusted EBITDA was RMB57.8 billion, aYoY increase of 25% and an MoM increase of 16%. The adjusted EBITDA margin rose from34%inthe sameperiodlast yearto39%.

Valuation and Outlook

Currently,Tencent'strailing P/E ratio over the past12months is15times,farbelowtheaverageleveloverthepast10years.

The term "undervalued" has been talked about for too long.But why doesn't the market give face?

The selling pressure from major shareholders may still be an important reason.Especially during the quiet period before financial reports are released,Tencent stopped repurchasing shares,and only steadfast major shareholders continued reducing their holdings,giving great pressure on market sentiment.Currently,the discount between $Prosus NV(PROSF)$ the major shareholder, and its net asset value is about 35%, which has decreased somewhat compared to before the reduction,but still does not solve the fundamental problem.

However, with the release of financial reports,Tencent can continue to repurchase shares in the secondary market,to some extent offsetting the impact of selling pressure. It also hopes that with this excellent financial report,it can restore market confidence.After all,the rise and fall of Tencent's stock price affects the future of both $HSI(HSI)$ and $HSTECH(HSTECH)$ .

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.

- AcidIce·2023-05-18Then still drop in pricing? So who's shorting it?1Report

- Laughingtong·2023-05-18[财迷][财迷]LikeReport