Is Disney worth a Buy after its earnings?

Since the last financial report, $Walt Disney(DIS)$ stock price has been fluctuating due to market observation of the effects of its leadership change in streaming media. Therefore, there was little volatility before the release of Q2 FY23 earnings on May 10th. However, it seems that the announcement of the financial report has set a general pattern for the entire streaming media industry.

Although it fell by 4% after hours, it only erased gains from previous days.

FY23Q2 Earnings Overview

Overall, current performance met expectations.

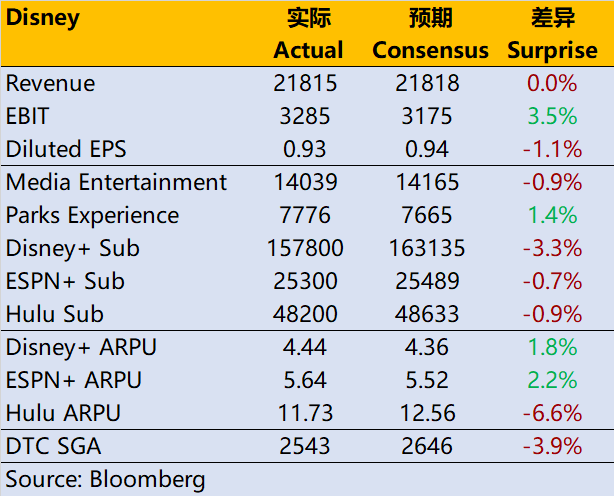

Revenue was $21.815 billion, up 13.3% YoY and in line with market expectations;

Non-GAAP operating profit was $3.285 billion, down 11.2% YoY but slightly higher than market expectations of $3.175 billion;

Adjusted EPS was $0.93 per share, slightly lower than market expectations of $0.94 per share.

In terms of operational data, total subscribers were 231 million which is lower than expected at 237 million;

Disney+ had 158 million subscribers which is lower than market expectation at 163 million and decreased by net four million users; however ARPU (average revenue per user) was $4.44 which is higher than expected at $4.36;

ESPN+ had approximately 25.3 million subscribers which almost met expectations;

Hulu had approximately 48.2 million subscribers compared to an expected number of around 48 .63 million; however ARPU was $11 .73 which is lower than expected at $12 .56.

Therefore, from a streaming media perspective since Disney+ launched new ad subscription packages and increased costs for ad-free subscriptions by38% to USD11 last year causing another decline in subscriber numbers but increasing revenue brought about by each individual user so overall income performance within media and entertainment sector wasn't affected negatively.

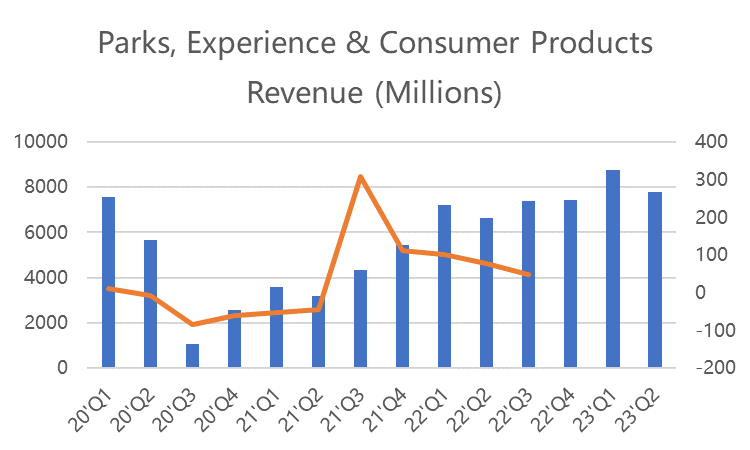

On the other hand, the park and experience business continued to maintain a good recovery momentum. After achieving 73% in FY22, it continued to grow at double-digit rates in the first two quarters of FY23 with Q2 growth rate at 16.9%. With the continuous recovery of Shanghai and Hong Kong parks, it is expected that there will still be improvement in park business performance for H2 FY23.

Investment Highlights

Subscriber numbers have declined for two consecutive quarters and the streaming media market pattern has roughly formed.

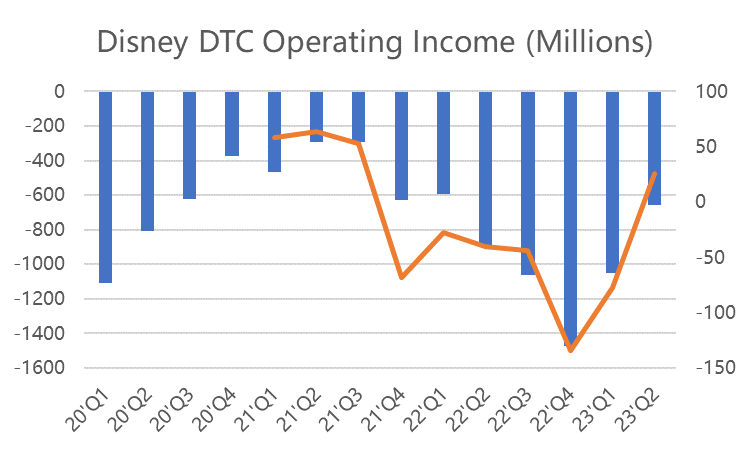

Since Bob Iger returned to Disney as CEO his primary focus was on "reducing costs and increasing efficiency", so he focused mainly on the loss-making streaming media department which included: 1. layoffs; 2. price increases; 3. increased advertising revenue; 4.balancing content distribution across different channels and markets.So we can see that DTC (Direct-to-Consumer) business operating losses decreased by $394 million YoY to $659 million which greatly exceeded expectations.

At the same time, increasing Disney+'s monetization ability means that user growth is no longer a priority, so once it reaches around 160 million subscribers then decline begins.This still leaves some gap between Disney+and Netflix's current market size.However,the content emphasis of both platforms are not exactly alike.Neflix also no longer focuses solely on subscription growth but instead develops more paths towards monetization.This is why we say that the general pattern of streaming media industry has taken shape. $Netflix(NFLX)$

Margins may show results in 2024.

Iger believes cost-cutting measures are progressing smoothly,and this year's budget reduction target of USD5 .5 billion is very likely to be achieved.Disney will launch an application integrating Disney+and Hulu in2023,further increase prices for non-advertising members,and continue international expansion efforts.

On the other hand,different from previous large-scale content investments,this year Disney will appropriately reduce content production and balance content distribution across different channels and markets.The most concerned Marvel Universe series among users may not have more powerful box office blockbusters this year after the unexpected reputation of "Guardians of the Galaxy 3" in recent times and global box office revenue of USD340 million as of May 5th.More TV shows such as "Loki2" may be launched on Disney+after summer.However,2023 remaining seasons and 2024 will be a test for Disney's content side.

Shanghai and Hong Kong will become key growth drivers for park business.

Disneyland achieved explosive growth due to its reopening in mid-2022,becoming a "key growth driver" that boosted company performance.Iger said he was particularly satisfied with the international area performance of Disneyland,and stated that Disney will continue to build capacity and promote long-term growth. This implies greater expectations for overseas park business this year.Shanghai Disneyland and Hong Kong Disneyland could become key drivers for park business.

The fomer CEO who previously said "Disney can achieve good results even without China" has stepped down, but Iger remains friendly.

Is Disney worth a buy?

Due to the losses in its streaming media division, the company's overall P/E ratio is still affected by this headwind. Its current dynamic P/E ratio is 42 times, higher than the industry average of 25 times and also higher than Netflix's 39 times.

However, due to expectations of cost reduction and efficiency improvement, the market expects Disney's P/E ratio for fiscal year 2023 to be around 24.5 times, slightly higher than the market average of 21 times but lower than Netflix's 30 times. In fiscal year 2024, it is expected that normal profit margins will return and the P/E ratio will fall back to 18.6 times, which is on par with the industry average.

If cost reduction and efficiency improvement exceed expectations, there may be positive news as normal profit margins could be achieved earlier. However if these measures negatively impact subscription user base or if declining demand for entertainment or advertising revenue affects performance expectations then it may take longer for profit margins to return to normal levels.

Therefore after being hit hard by COVID-19 pandemic and undergoing business transformation through streaming media reformations; Disney aims at completing its transition by year-end of FY2024. Until then investors can expect more guidance from quarterly reports providing them with more insight into progress.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.

- YueShan·2023-05-11Will improve soon ⭐⭐⭐3Report

- Abangadik·2023-05-13buyLikeReport

- Cathy Live·2023-05-12Nice1Report

- Brando741319·2023-05-11Ok3Report

- AuntieAaA·2023-05-11will improve2Report