CRM has another 66% upside potential, after its fantastic Q4 earnings

$Salesforce.com(CRM)$ just reported strong FY23Q4 earnings after March. 1st close, pushed its share price to new YTD high with a 16% surge, and YTD return soars to 46%, way better than benchmark $S&P 500(.SPX)$$NASDAQ(.IXIC)$ index. In 2022, the company just experienced a 48% downward.

Key points of Q4 Earnings.

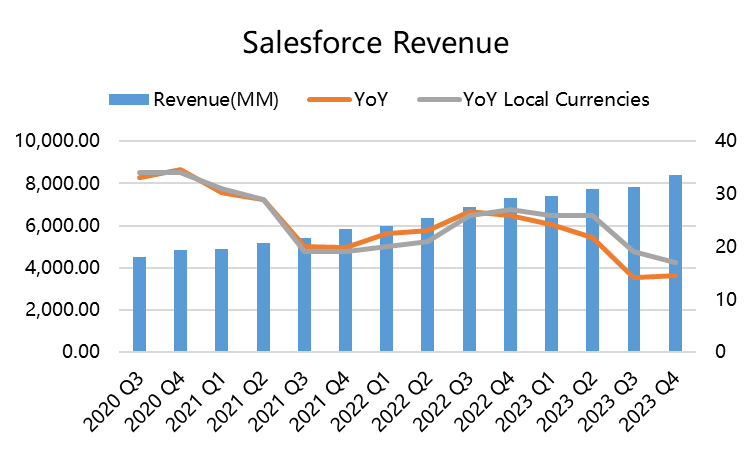

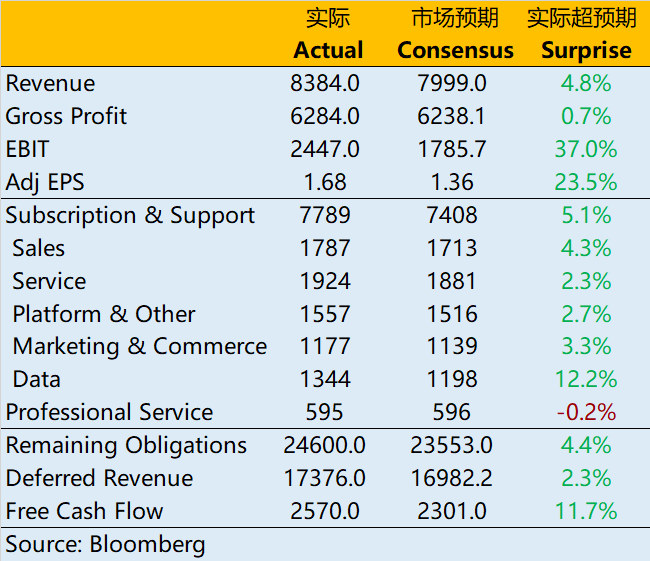

- Revenue $8.38 billion, YoY+14%, beat consensus of 9.2%. Currency neutreal YoY+17%, beat consensus of12%

- By segments, subscription revenue was $7.79B, up 14% YoY, beating market consensus of $7.47B, of which data service revenue $1.34B, beating market consensus of $1.2B by as much as 12%.

- Company software bill reached $14.57B, up 12% YoY, rising from 5.7% in the last quarter to double digits, and also beating market consensus of $13.73B.

- Remaining obligations $48.6B, +11% YoY, beating market consensus of $45.9B.

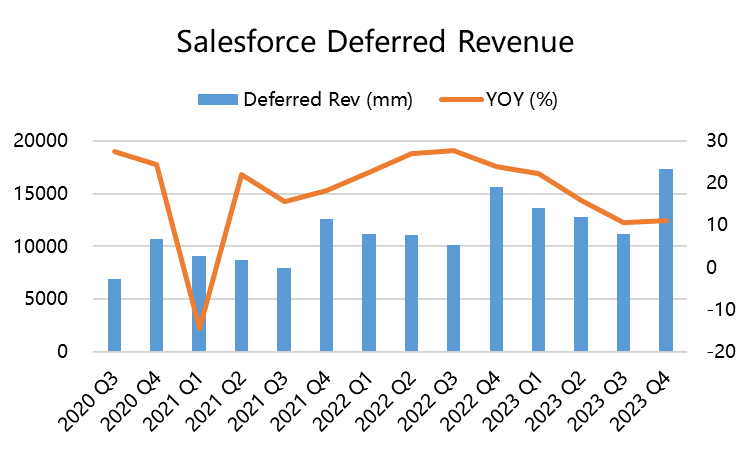

- Software deferred revenue $17.38B, up 11% YoY, beating market consensus of $16.98B.

- In terms of profit, comparable EBIT $2.45B, which doubled YoY 123%, beating market consensus of $1.79B. Adjusted operating profit rate also reached 29.2%.

- Free cash flow $2.57B, significantly beating market consensus of $2.30B.

- Adjusted EPS $1.68, beating market consensus of $1.36.

Guidance for FY2024: revenue o34.5-34.7B US dollars, beat consensus of 34.05B; Non-GAAP operating margin 27%, which is significantly higher than market consensus of 22.4%.

Good performance surprised investors with a sustainable prospect, Notice that,

First, company has experiences in recession. Salesforce experienced the Internet bubble in early 2000 and the crisis in 2008, all pass successfully.

We have a recession playbook. We know how to transform the company, company executives said in the conference. They (probably better than other companies) know how to cope with the recession cycle.

The company has increased the size of its stock repurchase program to $20B

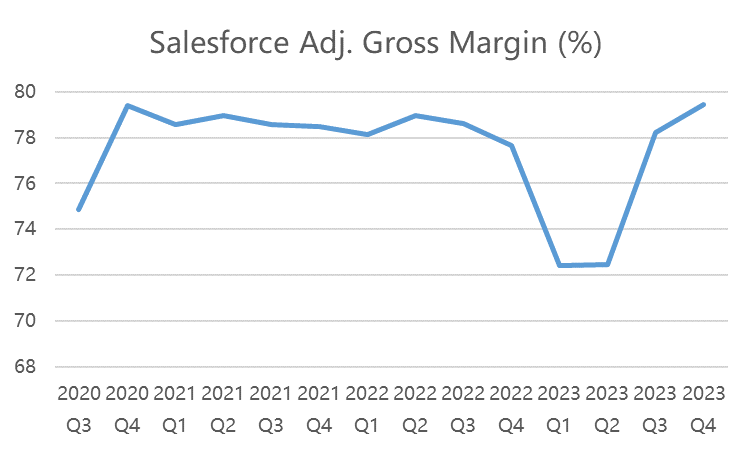

Second, switch from growth to profitability, there is still a lot of room. Adjusted gross margin of the Company has been maintained between 72% and 79% for a long time. In 2022, affected by the appreciation of the US dollar and changes in the supply chain, the gross profit margin of the Company also dropped to 72%. 23Q4 it come back to 79.45%, exceeding market expectations and providing a basis for the improvement of profit margin.

At the same time, it reduced operating expenses, reduced expenses, and laid off employees like other companies in the industry, which controlled operating costs and further improved operating profit margin. These operations doubled the EBIT (pre-tax profit) of the company.

The guidance given by the company for fiscal year 2024 also raised the operating profit to 27%, which means that the optimized operating efficiency improvement will continue.

Third, market expectations management. Although the profit rate declined for a period of time in 2022, the company exceeded expectations after each financial report was released in the past two years, mainly because the guidance to the market was very clear and the overly radical target was lowered in a timely manner. Before Q4 financial report, the general market growth rate will drop from the platform of about 25% to single digits. Although the actual value is only 14%, it is still far better than the single digit growth rate.

At the same time, this performance of the company also reflects the economic activities in the downstream market. As a leading enterprise, especially a company with decades of service history, it is often favored in the expected cycle of recession.

Fourth, active investors prompted the company to change faster. Since September 2022, at least five activist investors, including Elliott Capital Management and Starboard Value, have invested in Salesforce. Before activist investors took a stake, Salesforce aimed to achieve an operating profit margin of 25% by 2026, but after they entered, the target operating profit in fiscal year 2024 reached 27%.

Of course, activist investors may have a bigger goal. The company changed its board members, laid off 8,000 employees for the first time, including many senior executives, and recently laid off employees in the second wave. Elliott Capital Management, meanwhile, is in the process of being added to its board, with more aggressive moves likely in the future, including mergers and acquisitions.

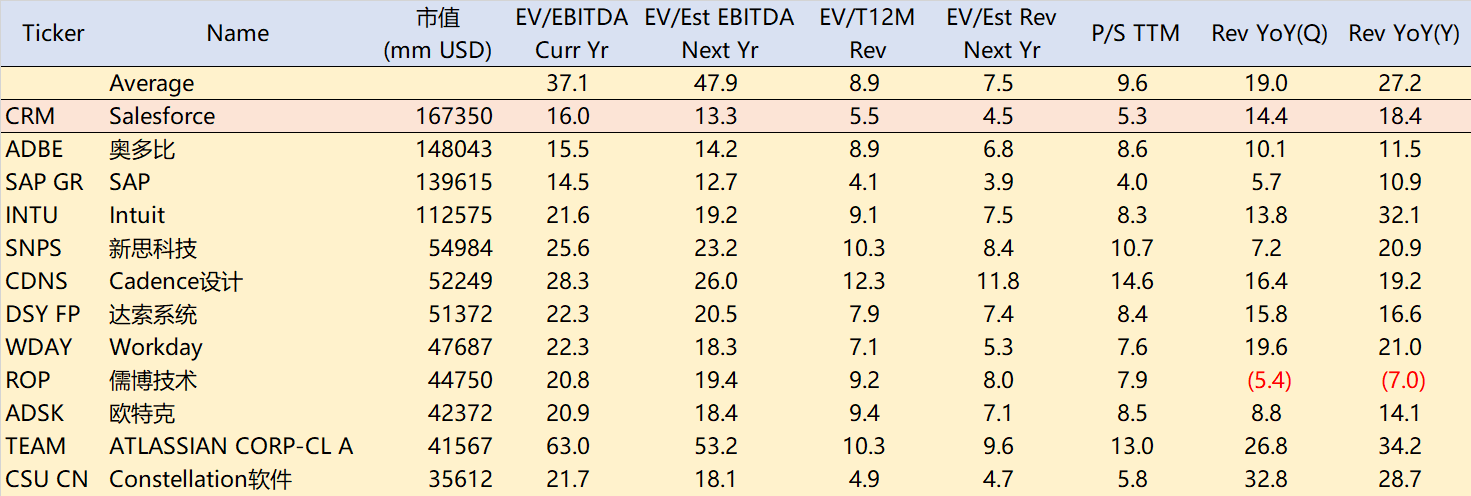

Valuation

CRM multiples are still in middle and low level in the industry. If the company can maintain the current growth rate and profit rate, there is still room for upward mean regression.

Industry average 7.5x EV/Sales, which means CRM still +66% upward

Industry average 22.5x EV/Ebitda (MV>$30B),which means CRM still +66% upward too.

This is also an important reason for the company's increase of 15% after hours.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.

- suthanb4u·2023-03-02CRM will be a wonderful short idea at $198. Thanks.2Report

- suthanb4u·2023-03-02Bro, you must be kidding. Index is nose diving in couple of weeks and there is no sign of landing at all.. Here you are talking about going to moon. 😆 Wow...!?!2Report

- Tigaroo·2023-03-02Strong fundamental outlook. Not sure if it is enough to sustain short term share price increase amidst rate hikes.2Report

- TKPK·2023-03-02thanks for sharing3Report

- Svengers19·2023-03-03Thanks for sharing2Report

- polenkoutside·2023-03-02Great ariticle, would you like to share it?2Report

- CET 789·2023-03-05[Cool] [Cool] [Cool]1Report

- Kellytan·2023-03-07ok1Report

- Nlatykislove·2023-03-05[Smile][Smile][Smile][Smile]LikeReport

- KY56·2023-03-05Nice.👍LikeReport

- Cing·2023-03-04👍LikeReport

- huaer8497·2023-03-03[微笑]LikeReport

- LiTeng24·2023-03-03GoodLikeReport

- FK1234·2023-03-03💪LikeReport

- 建稳的朋友·2023-03-03🙏🙏1Report

- Alvis89·2023-03-03Go od1Report

- Tyanak·2023-03-03👍🏻1Report

- Gemstone·2023-03-03Gfff1Report

- chang168·2023-03-03up1Report

- chinks29·2023-03-03Like1Report