At this point, it finally feels possible to roughly tell what Trump is trying to do.

He first took the extraordinary step of seizing Venezuela’s president, threw Venezuela into turmoil, and wrecked its economy. He then threatened to launch military strikes against Iran, and just the day before yesterday issued a security alert telling all U.S. citizens in Iran to leave immediately, building momentum as if a real military operation were about to begin. A simple tally of the countries Trump has threatened or actually acted against since the start of January 2026 is startling: in just half a month, the U.S. president has made threatening statements or taken coercive actions targeting 11 countries/regions.

So what is he trying to do? The answer lies in the U.S. Dollar Index standing at the edge of a cliff.

Unusual behavior always has a reason. The macro logic underneath can be summed up in one sentence: Trump is trying to create buyers for U.S. Treasuries—or more precisely, for U.S. dollar assets—by destabilizing other countries’ economies and disrupting the global flow of capital. By stirring up chaos in global markets, he aims to pull large amounts of speculative “hot money” into dollar assets for safety, thereby holding up the U.S. Dollar Index, which is on the verge of breaking down and accelerating lower

$美元指数(USDindex.FOREX)$ $做空美元指数-PowerShares(UDN)$ $美元ETF-PowerShares DB(UUP)$ $USD Index(USDindex.FOREX)$

If the Dollar Index can stabilize and rebound at this critical technical level, the U.S. economy may be able to transition smoothly and provide a favorable environment for Trump in the 2026 midterm elections. If the Dollar Index instead accelerates downward, the loss of buyers for U.S. Treasuries would push yields sharply higher again and create selling pressure at elevated levels in U.S. equities.

Most importantly, inflation could spiral out of control. Under Trump’s open influence, the current Federal Reserve has already moved toward a fully dovish stance, making two 50-basis-point rate cuts in 2026 a high-probability scenario regardless of what happens. If inflation cannot be contained at that point and “goes into runaway mode,” the Republican Party could lose public support in the midterm elections.

Against that backdrop, You should consider why Trump wants to pin inflation on Powell and has threatened to pursue Powell’s criminal liability, and why Trump has actually stepped in to strike at the Venezuelan regime and control Venezuela’s oil resources. It offers two stated reasons: first, to prepare to increase U.S. oil output later and control energy prices to manage inflation; second, to throw smaller countries’ economies into disorder so capital that would have gone to those countries instead flows into the United States.

these countries’ currencies are depreciating sharply, while the Dollar Index has gradually begun to rebound,

$新兴市场ETF-Direxion三倍做多(EDC)$ $新兴市场美元债ETF-iShares(EMB)$

The Dollar Index historically has a “smile curve” theoretical foundation :

when global geopolitical risk rises, dollar assets are usually the preferred safe haven for most capital because the U.S. economy is stable and the dollar has the function and status of a global reserve currency; when global order is in turmoil, the Dollar Index often rises.

But the situation is now somewhat different: the dollar’s share in global reserve currency usage has been falling continuously; Trump has been heavily intervening in the Fed; and the U.S. debt and fiscal deficit ratios are high, together repeatedly damaging confidence in the dollar. As a result, a large amount of international “hot money” no longer dares to treat dollar assets as its only safe-haven pool

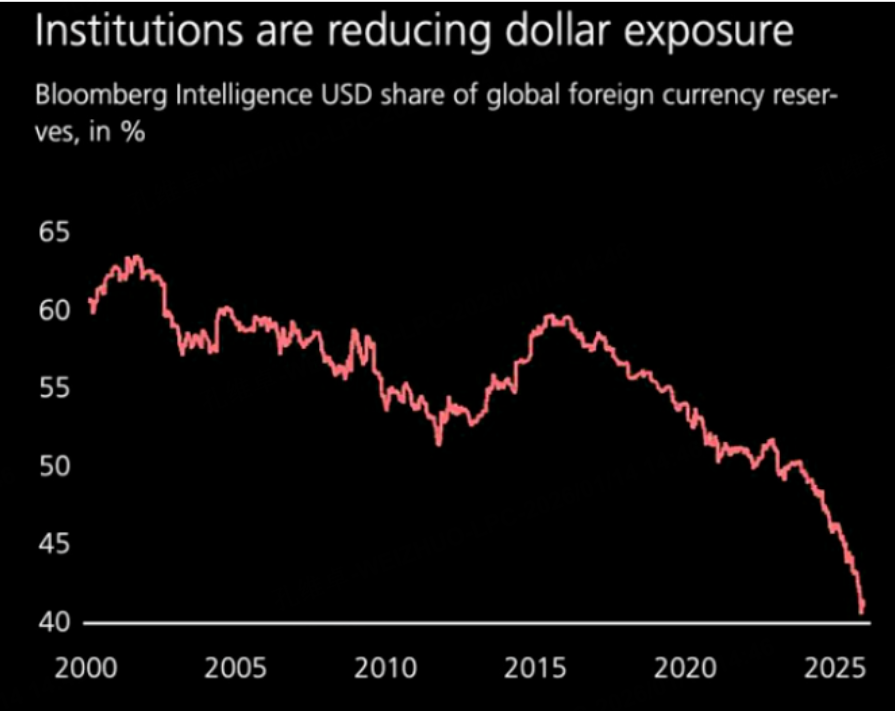

Over the past 25 years the dollar’s share of foreign-exchange reserves has steadily declined, and that the decline has accelerated in recent years

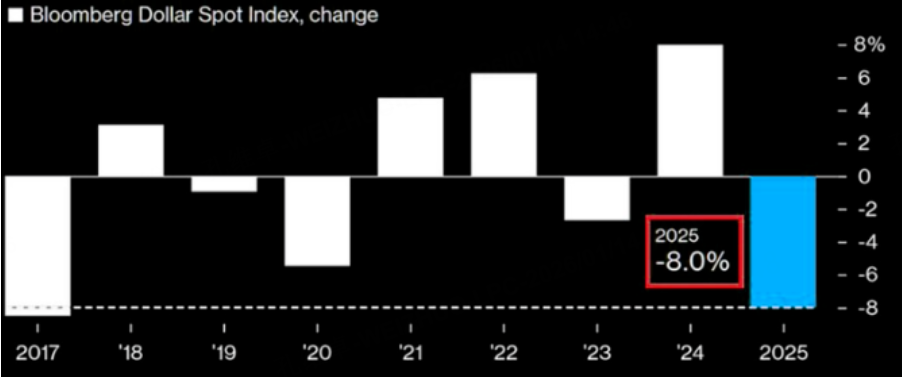

In 2025 the Dollar Index fell 8%, a very large drop

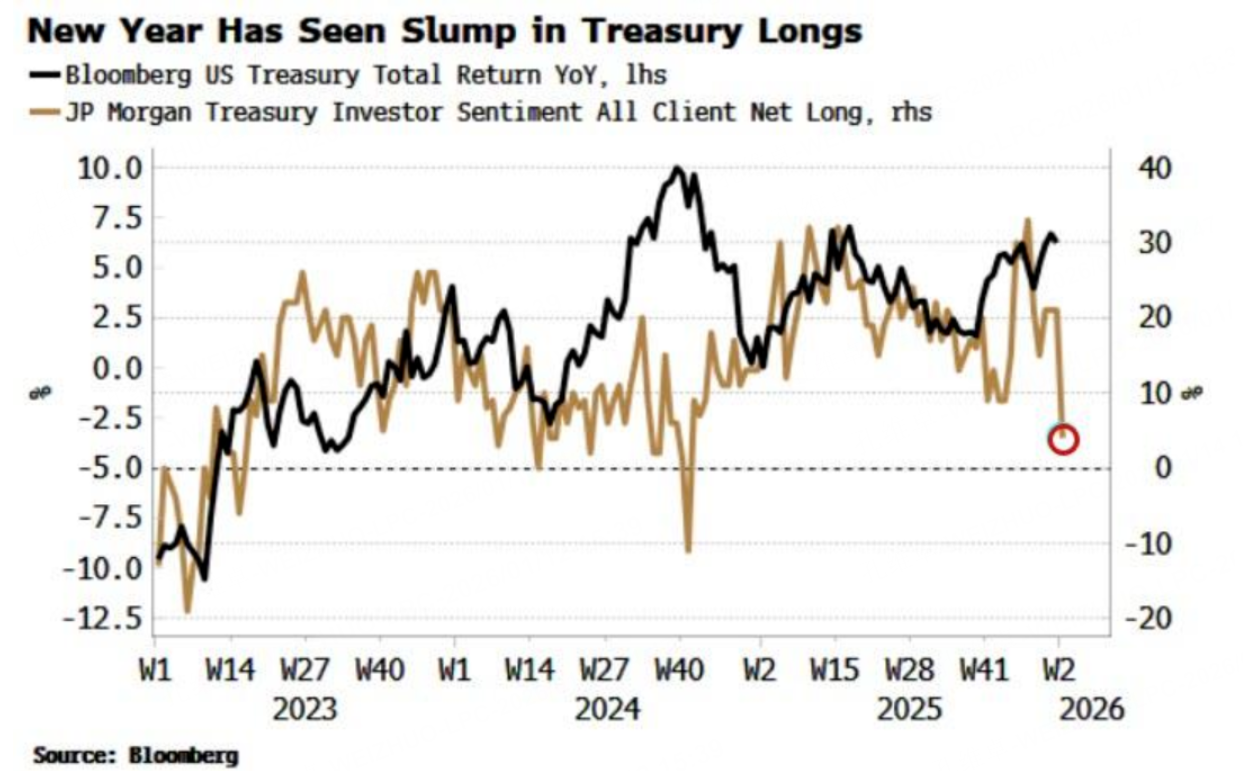

As a JPMorgan client survey, saying that selling pressure in U.S. Treasuries is strengthening and that clients’ net long positions in Treasuries have fallen sharply, $10年美债主连 2603(ZNmain)$ $20+年以上美国国债ETF-iShares(TLT)$

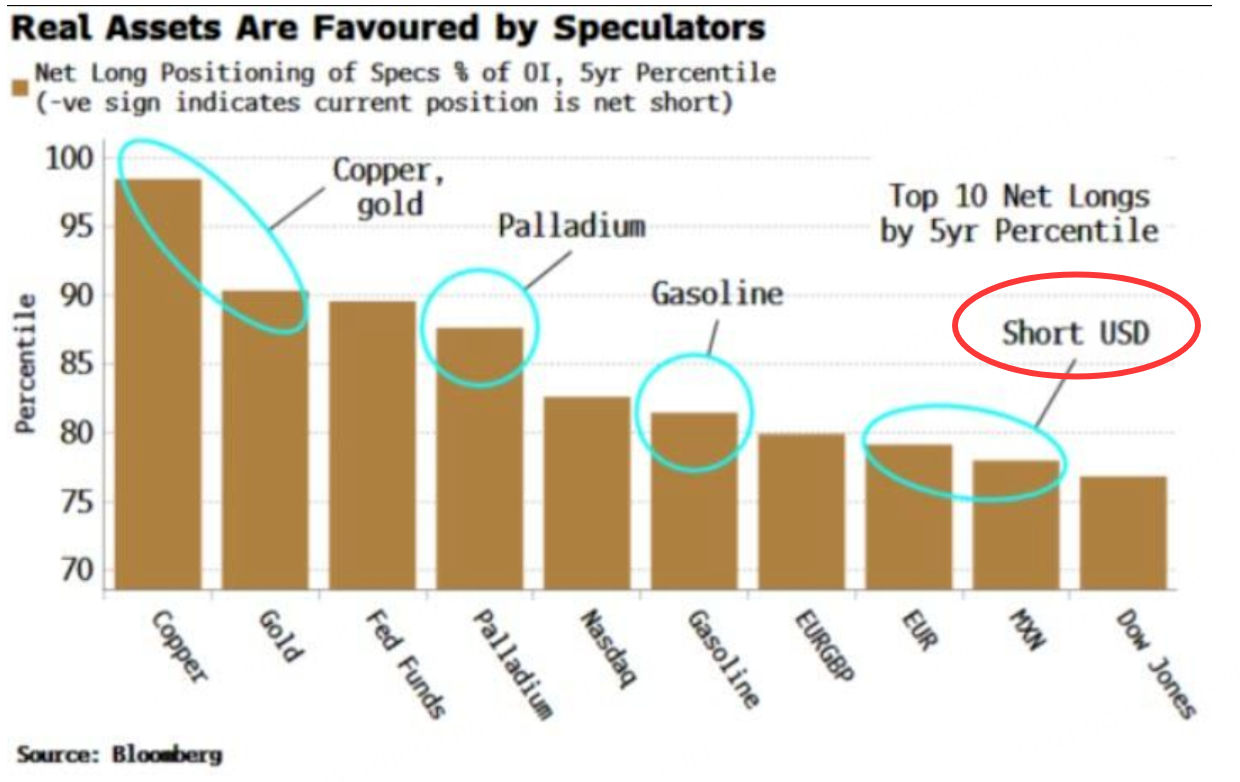

While the share of active clients taking short positions has risen, The latest COT (Commitments of Traders) data, saying net long positions in non-dollar currencies have risen noticeably,

$欧元主连 2603(EURmain)$ $欧元ETF-ProShares两倍做空(EUO)$ $欧元做多ETF-CurrencyShares(FXE)$ $日元主连 2603(JPYmain)$ $日本ETF-iShares MSCI(EWJ)$

That is why, when the dollar’s haven monopoly weakens, the destination of defensive flows shifts. Gold and silver become the obvious alternative. Hong Kong and China A-share markets become a natural destination as well, and the surge in these markets—especially the explosive run in Hong Kong/A-share nonferrous metals—aligns with that safe-haven reallocation logic.

There is also a liquidity macro tailwind. Both the U.S. and China are likely to remain accommodative in 2026: the U.S. is navigating midterms, while China is pursuing growth and resisting deflation. Growth itself is uncertain, but China’s M2 growth is real, and policy objectives emphasize boosting consumption and lifting CPI. In that environment, cyclical sectors—nonferrous metals, commodities-linked cyclicals, and raw-material names—retain upside possibility.

Positioning then becomes conditional on the Dollar Index. If Trump succeeds and the Dollar Index rebounds hard off weekly support, the current “mini bull market” in Hong Kong/A-shares faces pullback risk. If the Dollar Index breaks down from that level and accelerates lower, the Hong Kong/A-share uptrend can continue.

Strategy discussion: U.S. equity indices, crude oil, and silver

The current approach remains to sell put options on Nasdaq-related futures below the 20-week moving average (using QQQ as a substitute), and that puts have been sold on a rolling basis for several weeks and all ended by collecting the full premium. The outlook for U.S. equities is relatively stable and this strategy can continue to be considered.

On crude oil, because of Trump’s confrontational stance toward other countries, geopolitical-conflict expectations have stimulated oil prices, pushing them above the 60-day moving average and breaking above the 100-day moving average;

This move looks very similar to the last impulse-type move. In the short term, if Trump’s externally provocative posture does not change, crude may push into an impulsive upswing, but because supply is expected to increase and demand has not shown clear growth, the view is that oil’s move is an impulse-style rise followed by a pullback. We could consider a strategy: go long Near-month contract and short Far-month contract to capture spread expansion during the impulse move, with a stop-loss at a break below the 60-day moving average, and it treats an easing of U.S.–Iran tensions as the take-profit inflection point.

Silver’s rise may still be smaller than the last monthly bull-market move, and that there may still be considerable upside room for a continued short squeeze. The previously discussed spread-arbitrage strategy of selling the near month and buying the far month is only suitable after silver confirms a large pullback; the trigger is when silver pulls back and breaks below the 5-day moving average.

Therefore, as long as price remains above the 5-day moving average,silver price remains bullish; those who want to capture profits from the uptrend can consider an options strategy on a silver-related ETF, or buy micro silver futures lightly on dips, using a break below the 5-day moving average as the stop-loss.

$白银主连 2603(SImain)$ $迷你白银主连 2603(QImain)$ $2倍做多白银ETF-ProShares(AGQ)$

Comments