Last week’s macro framework is still working this week, and Trump has kicked off yet another farce: he floated the idea of purchasing Greenland from Europe and also imposed tariffs on eight European countries that opposed him. The situation has become even more turbulent.

Why Trump Threatened 11 Countries in Just Two Weeks: The Dollar on the Edge Tells the Story

This is almost certainly not the last step in Trump’s external provocation, but it is very likely an important move within his broader foreign strategy.Today, let’s take a little time to briefly discuss the logic behind the Greenland dispute.

First, one point must be clarified: why is Trump deliberately stirring trouble in his own “backyard”? One day it’s Venezuela; the next day he picks a fight with Europe—so why doesn’t he dare, like before, to target China and Russia, or create trouble in the Asia-Pacific region?

Why Trump (for now) can’t afford to antagonize China and Japan

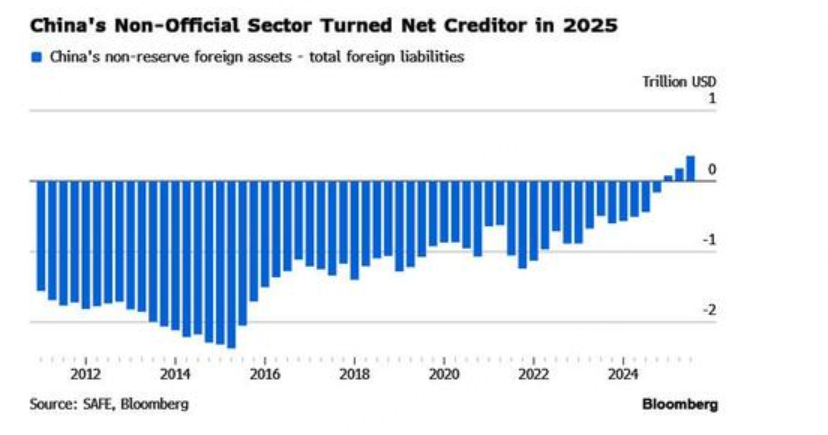

Start with China.An important data point deserves attention: according to the latest data released by China’s foreign-exchange market regulator, “non-official” investors’ overseas asset holdings surged by more than USD 1 trillion in the first three quarters of last year—more than double the average annual growth rate over the past decade.

This suggests that, as China’s trade surplus has grown over the long term, a large amount of surplus funds accumulated in corporates’ offshore accounts has likely been invested. A reasonable guess is that much of this capital flowed into U.S. Treasuries to capture elevated Treasury yields.

$A50指数主连 2601(CNmain)$ $恒生指数(HSI)$ $恒生指数主连 2601(HSImain)$ $恒生科技指数主连 2601(HTImain)$ $恒生科技指数(HSTECH)$ $三倍做多富时中国ETF-Direxion(YINN)$ $MSCI中国A50指数主连 2602(MCAmain)$ $中国大盘股ETF-iShares(FXI)$

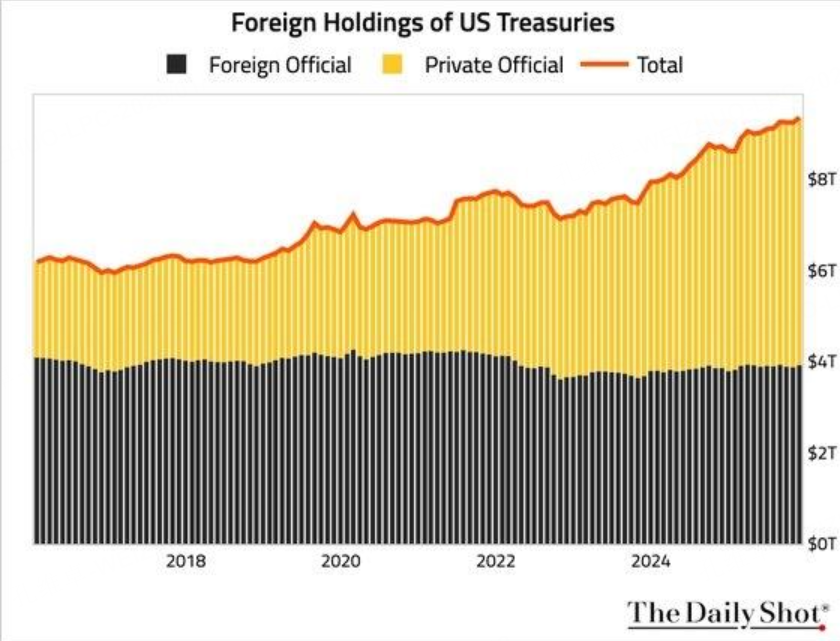

From the most recent Treasury buying patterns, there has been a clear structural shift—“state out, private in”: sovereign accounts are selling Treasury assets, while non-official channels (individuals, households, institutions, and corporates) are accelerating purchases of U.S. Treasuries.

$10年美债主连 2603(ZNmain)$ $20+年以上美国国债ETF-iShares(TLT)$

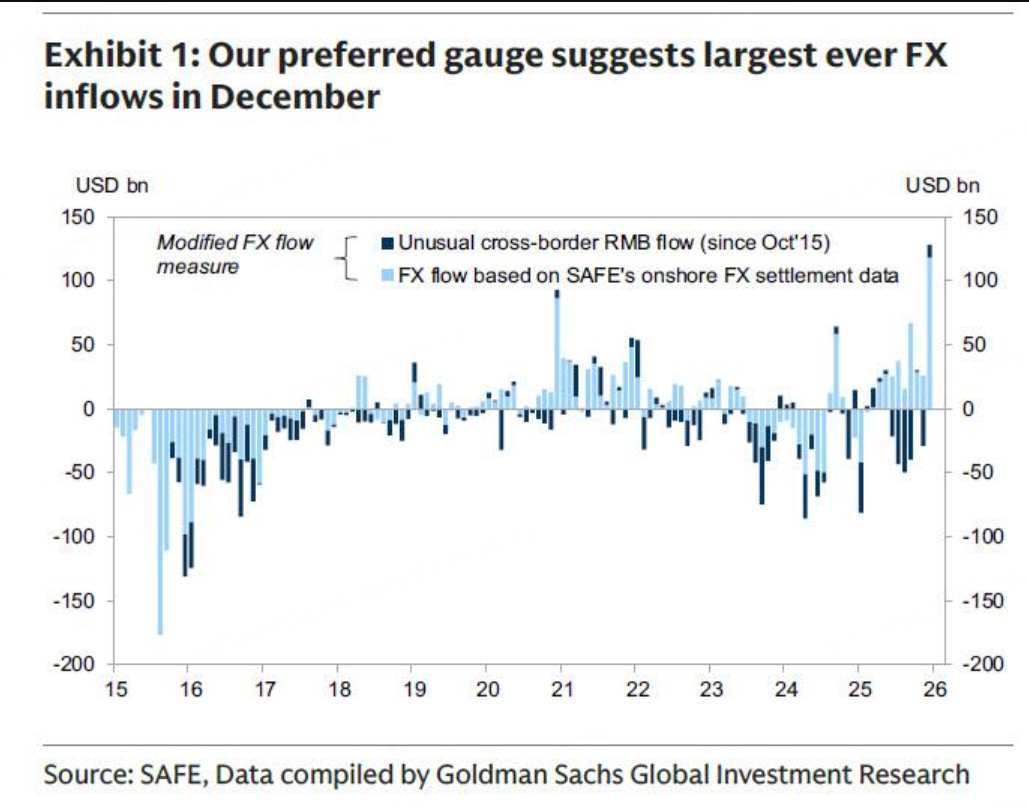

Bloomberg’s statistics show that last year Chinese private investors’ investment in overseas securities (including U.S. equities, European bonds, and mutual funds) jumped by USD 535 billion, and the increase in the first three quarters through September exceeded the same-period increase of any year over the past two decades. This increase was also larger than China’s direct investment used to build factories and warehouses overseas or to expand headcount

Because of the recent appreciation of the renminbi, some of this capital has abruptly begun to flow back.

According to official data released last Thursday, Goldman Sachs noted that China recorded USD 128 billion of inflows in December—the “largest ever” FX inflow on record and the highest level since 2015—mainly driven by a sharp rise in corporates converting foreign currency into renminbi.

So, if China’s economy begins to grow, China’s government bond yields rise, the China–U.S. rate differential widens, and the renminbi continues to appreciate, then it is quite possible that this money will flow back onshore. The result would be further renminbi appreciation and higher domestic inflation.

The impact on China can be set aside for now, but the impact on the U.S. economy would certainly be negative.

And beyond the possibility of Chinese capital flowing back, Japan also faces the same possibility.

The Bank of Japan is currently moving cautiously toward interest-rate normalization—exiting yield curve control and allowing JGB yields to rise.As one of the world’s three most stubborn bubbles, Japan’s bond prices have been weakening continuously.If yields rise too much, if Japanese rates continue to move higher, and if the yen gradually appreciates along that path, then Japan’s overseas investments—more than USD 1 trillion invested in Europe and the U.S.—could begin to repatriate, a logic discussed repeatedly before.

$日元主连 2603(JPYmain)$ $日元ETF-ProShares两倍做空(YCS)$ $日元ETF-CurrencyShares(FXY)$

That would further tighten liquidity in Europe and the U.S., with hot money gradually returning from the West to Asia-Pacific markets. Of course, it is hard to believe the newly formed Japanese government has the nerve to keep hiking rates aggressively,And from the self-interest of both Japan and China, neither likely wants its own currency to appreciate too fast, because that would reduce trade-surplus income.

But from Trump’s perspective, he should be very afraid of the two scenarios above, because by market inertia there is already a broad trend of “the East rising and the West declining,” and only deliberate government intervention can prevent—or at least slow—this trend.

Therefore, Trump’s ability to stir trouble in the Asia-Pacific region has been much more limited lately, because governments in this region may hold core U.S. economic interests in their hands.

So for now, he can only “harvest” his backyard—from Venezuela to Iran, and now to Europe’s Greenland. On the one hand, this is meant to attract more safe-haven buying into dollar assets—especially U.S. Treasuries; on the other hand, it is also part of a strategic resource confrontation and positioning against the major powers in the East.

For example, China and Russia have large reserves of oil, base metals, and rare metals.

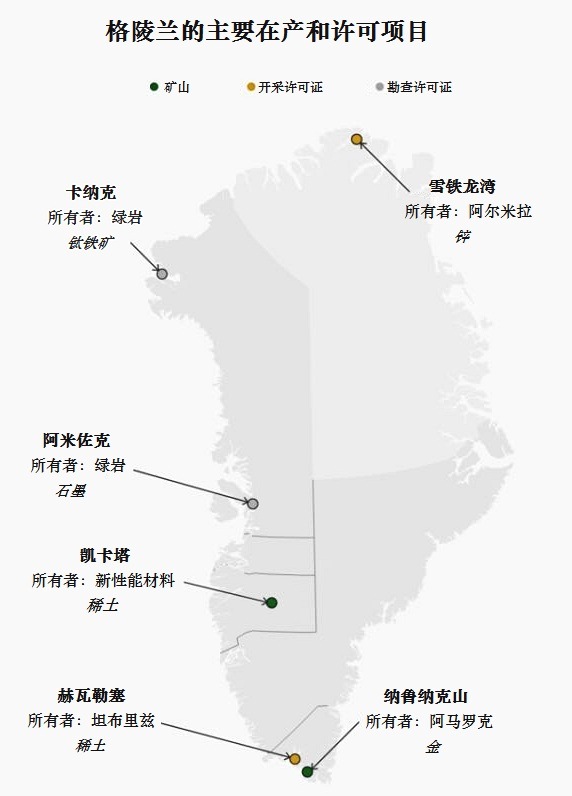

If pricing power over those resources were to be lost, it would be a major blow to U.S. control over inflation, so the U.S. must have tangible, controllable resources—such as Venezuela’s crude oil resources, Venezuela’s silver export resources, and Greenland’s massive rare-earth resources, including rare metals such as neodymium, praseodymium, and dysprosium.

$铜矿ETF-Global X(COPX)$ $COMEX铜主连 2603(HGmain)$ $材料ETF(XLB)$

In addition, strengthening control over Venezuela and Greenland can also improve control over key shipping routes, because Greenland sits at a strategic chokepoint between North America and Europe and is a critical position for monitoring Russian and Chinese military activity in the Arctic. And by controlling Venezuela’s key maritime shipping lanes, the U.S. would systematically weaken the Eastern major power’s presence around the Panama Canal and U.S. West Coast ports.

Under this logic, Canada’s prime minister is already “crying in the bathroom,” because Alberta is also one of the strategic places Trump very much wants to control.

The most critical point is this: if Trump plays it this way, inflows into dollar assets are not at risk. If he were to pick a fight with China and Japan, those two countries could raise their exchange rates and trigger a systemic repatriation of European and U.S. hot money, which would create major trouble for the U.S. economy.

And regardless of whether Europe agrees to the U.S. buying Greenland, the resulting turmoil would still push money invested in Europe to flow into the United States. If the U.S. successfully takes Greenland, it gains a big advantage; if it fails in the short run, it still gains a smaller advantage—either way, it’s a win.

If that logic is clear, the next question might be: why doesn’t Europe dare to resist the U.S. at the root—for example, by directly dumping U.S. Treasuries?

$欧盟国家ETF-iShares MSCI(EZU)$ $欧盟50指数主连 2603(FESXmain)$

The Europe–U.S. economies are intertwined in countless ways, and rising U.S. asset prices are also beneficial for European investors. Historically, the U.S. has not been shy about undermining its allies, but EU power is relatively dispersed; after Merkel, Europe lacks a “Iron Lady”-type leader who can unify the bloc to pursue shared interests. So measures like selling Treasuries, or even military confrontation, are likely to be loud in rhetoric but weak in execution across European countries. Whether Greenland will be sold, or Europe will pay a large “protection fee” to keep Greenland, remains to be seen.

Strategy

First, pay attention to the euro, which may be forming a top in the near term and could continue to decline.

If the euro breaks below the lowest point of the topping structure, it may trigger a weekly downtrend; correspondingly, the U.S. dollar index could stage a comeback rally. As shown in the chart, the neckline of the topping structure is around 1.150; if it breaks below, consider looking long, and if it rallies back up, exit immediately.

At the moment, the probability that the euro is bearish still looks relatively high. or establish a bear spread options strategy; the euro’s current peak at 1.197 is likely difficult to break in the short term.

Silver

Last week it was noted that silver is still in a short-squeeze move; in a squeeze, do not try to call the top. Use the 5-day moving average as the take-profit/exit line for the bullish view—if it breaks below the 5-day MA, exit long positions immediately.

If it breaks below the 10-day MA, a major silver pullback may emerge; at that point, sell the near-month March silver contract while buying the far-month June silver contract, to earn profits from a bear-market calendar spread arbitrage.

U.S. equity index

For U.S. equity indices, it is still believed that in the short term the S&P 500 futures index is unlikely to break below the 20-week moving average. In futures, consider going long S&P futures around the 20-week MA, stop out if it breaks below, and use the S&P futures 20-week MA as the dividing line between bullish and bearish positioning for U.S. equity indices.

$道琼斯指数主连 2603(YMmain)$ $NQ100指数主连 2603(NQmain)$ $SP500指数主连 2603(ESmain)$

Comments

Great article, would you like to share it?