Summary

- Objectively, the likelihood of a significant correction in the stock market now deserves attention.

- In the recent past, Apple and Microsoft have responded differently to a significant decline in the stock market.

- Apple and Microsoft tend to be undervalued in terms of future cash flow, and overvalued in terms of potential dividends.

- In the event of a hypothetical correction, Microsoft's potential for falling is lower than Apple's.

As an introduction...

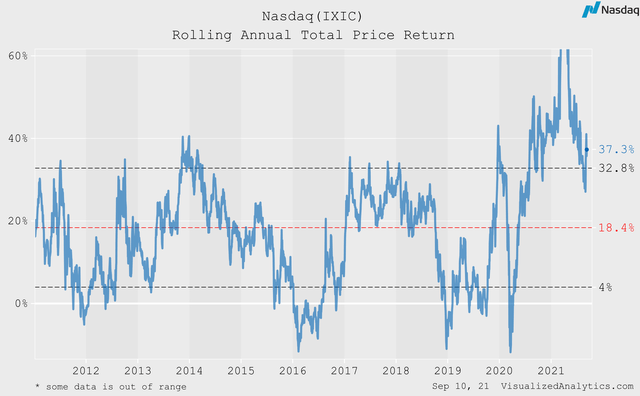

Since the last major correction in the US stock market ended in March 2020, the Nasdaq index has risen nearly 170%:

For a year and a half, this is a very strong result, considering that the average annual total price return of the index over the past decade does not exceed 20%.This fact alone makes us estimate the likelihood of a new significant correction in the stock market higher.

In addition, there are other factors that make us wary of the current price level of the market.

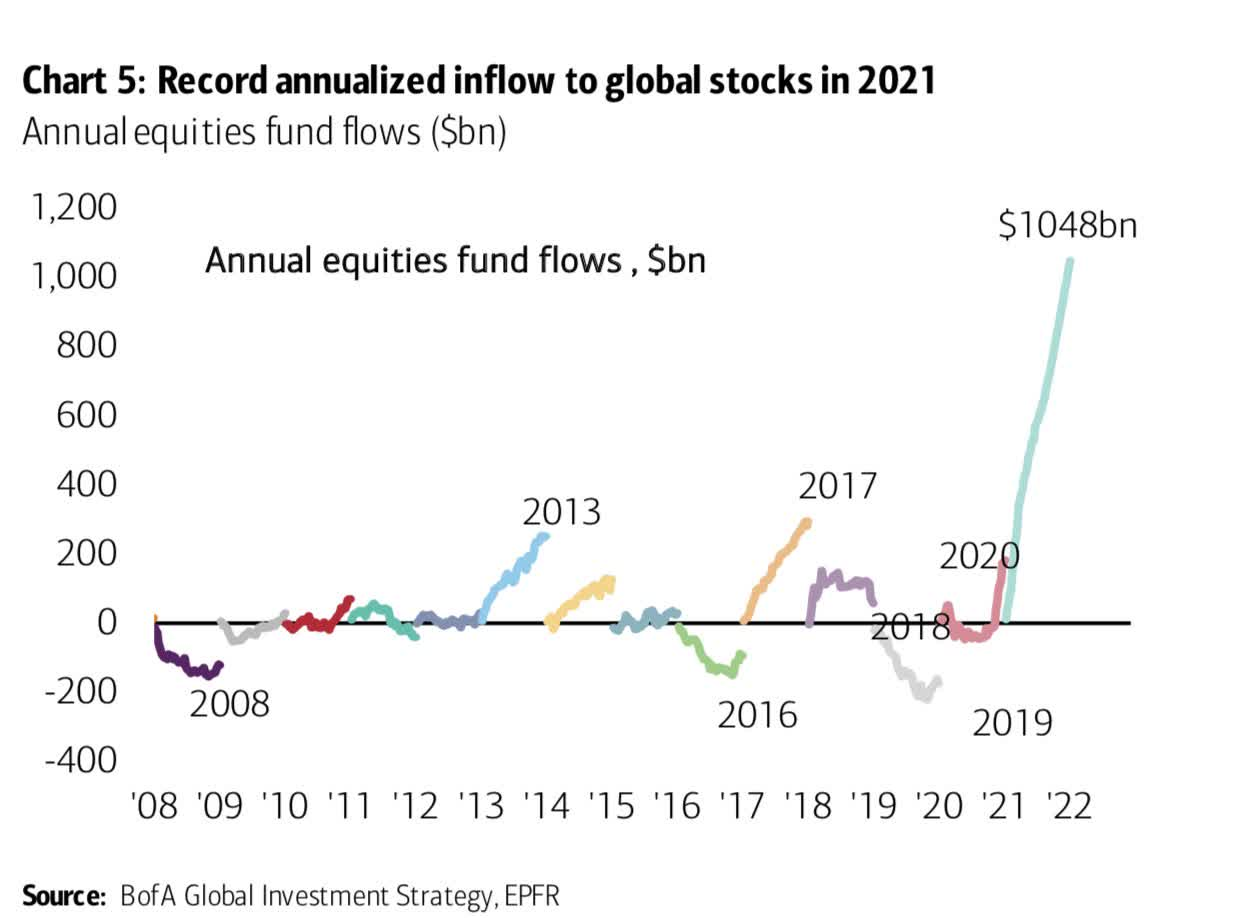

First, this year there is a record inflow of liquidity to the stock market. I'm not talking about the reasons now, they are obvious. But this fact alone makes the market extremely volatile:

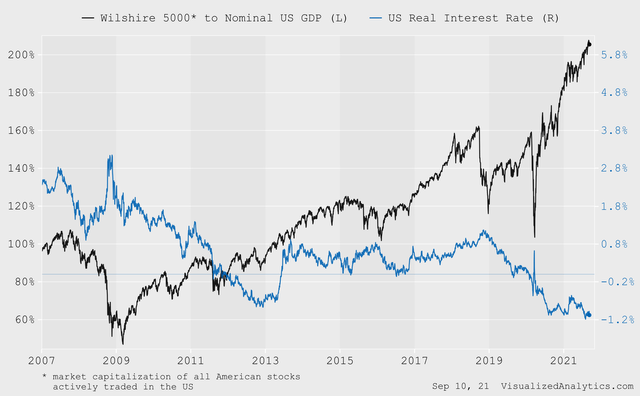

Second, the relative size of the US stock market has exceeded 200% of nominal GDP. In principle, this is not a fundamental limit. But it was the ultra-soft monetary policy that allowed the US stock market to reach its current record level. And most likely, in this context, a reversal is already outlined.

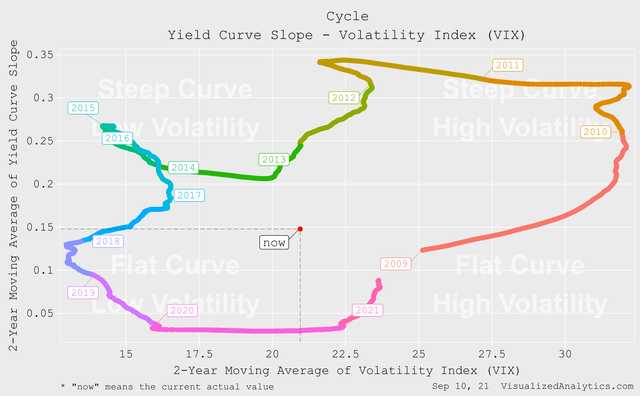

And finally the third. The macrocycle also allows us to expect the market to enter a phase of increased volatility and tightening of monetary policy:

So, objectively, the likelihood of the next correction of the stock market at least deserves attention. And in this context, I propose to answer the question:in case of a correction, which company is inclined to fall harder - Apple (AAPL) or Microsoft (MSFT)?

Why Apple vs. Microsoft?

The decision to compare exactly these two companies was dictated by two factors.

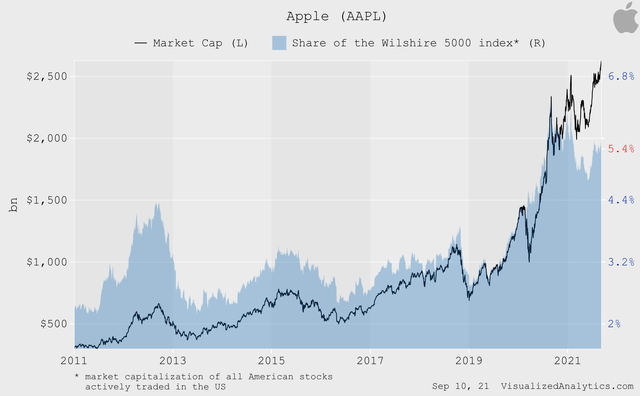

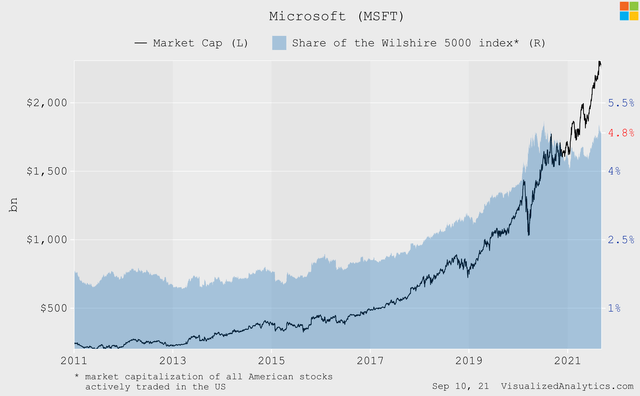

Firstly, these are the two largest companies in the tech sector, together accounting for more than 10% of the total capitalization of the US stock market. These companies are so large that, in principle, their dynamics alone can cause a new wave of correction:

Secondly, both companies pay dividends. In matters of fundamental valuation, this factor plays a significant role.

Some Statistics

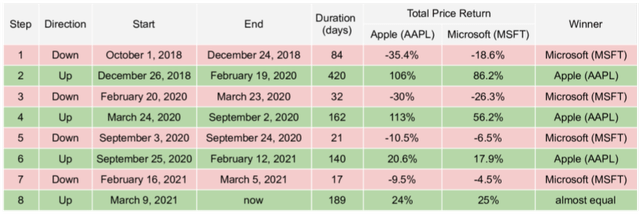

To begin with, let's take a look at what price dynamics both companies have shown during strong market fluctuations in the recent past.

To do this, I have broken the three-year span into eight periods of market movement:

Here are the results that companies have shown in each of the periods:

At first glance, the statistics are unambiguous:during periods of correction, the price of Microsoft tends to decrease less than that of Apple.But on the other hand, Apple has consistently performed better during periods of market growth. And in this case, the result obtained can simply be explained by the technical factors of the market behavior.

But in the current period of growth, both companies demonstrate approximately the same return. And therefore, here we do not find a clue to our question...

Fundamentals

Exclusively in an investment context, the price of a company's share can be viewed from two points of view.

On the one hand, the price reflects the present value of the company's future cash flow. On the other hand, the price is the present value of the sum of all potential dividendsthat the company will pay in the future. Let's model these prices for Apple and Microsoft. And for this I will build, respectively, the Discounted Cash Flow Model and the Dividend Discount Model.

In order for the models to be less subjective, I will take as a basis the average expectations of analysts regarding the revenue and EPS of the companies in the next decade.

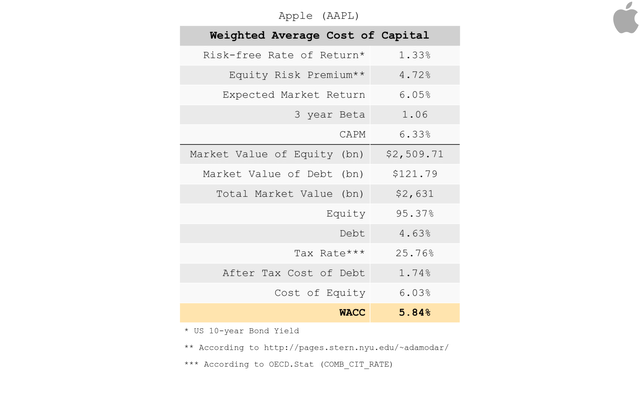

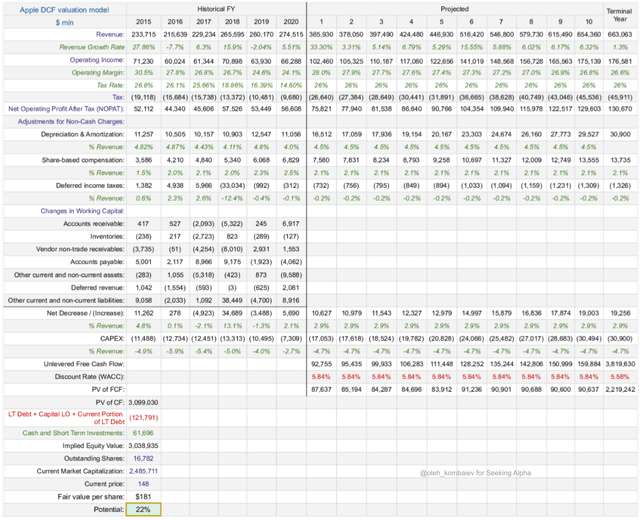

Let's start with Apple. Here is the calculation of the Weighted Average Cost of Capital:

Notes:

- In order to calculate the market rate of return, I used values of equityriskpremium (4.72%) and the current yield of UST10 as a risk-free rate (1.33%).

- I used the current value of the three-year beta coefficient. For a terminal year, I used Beta equal to 1.

- To calculate the Cost of Debt, I used the interest expense for 2020 divided by the average debt in 2019 and 2018.

Here is the DCF model:

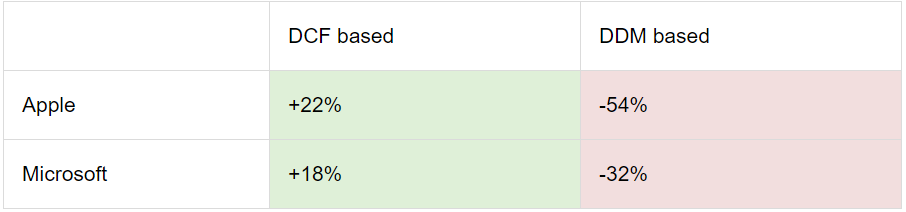

The DCF-based target price for Apple's shares is about $181 (+22%).

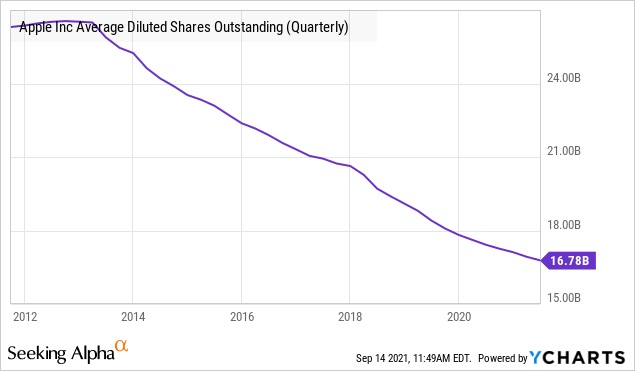

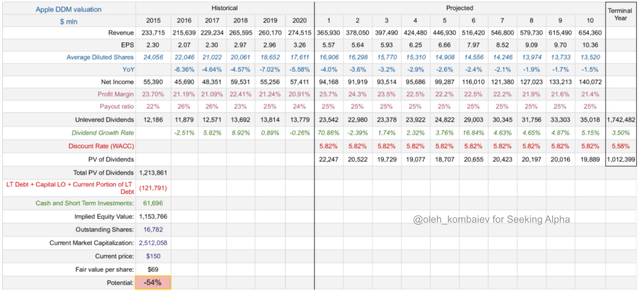

In the case of Apple, when building the Dividend Discount Model it is also necessary to take into account the fact that the company continues to actively buy back:

Continuing the current dynamics, the model assumes that by the terminal year the number of diluted shares will be reduced to 13.5 billion.

Apple spends an average of 25% of its net income on dividends. I assume that the payout ratio will remain at this level.

Here is the Dividend Discount Model itself:

The DDM-based target price for Apple's shares is $69 (-54%).

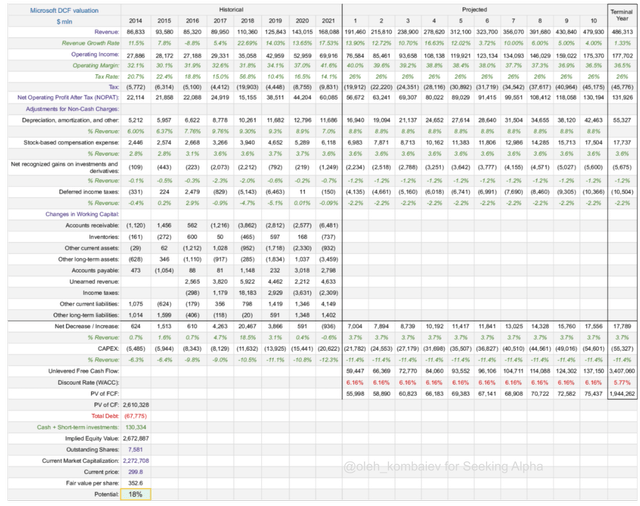

Now let's take a look at Microsoft.

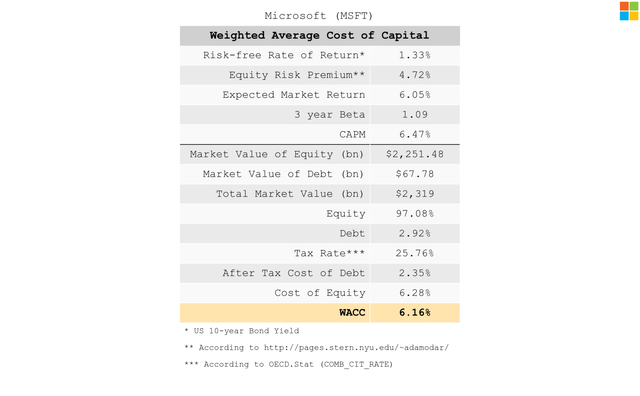

Here is the calculation of the WACC:

And here is the DCF model:

The DCF-based target price for Microsoft's shares is about $353 (+18%).

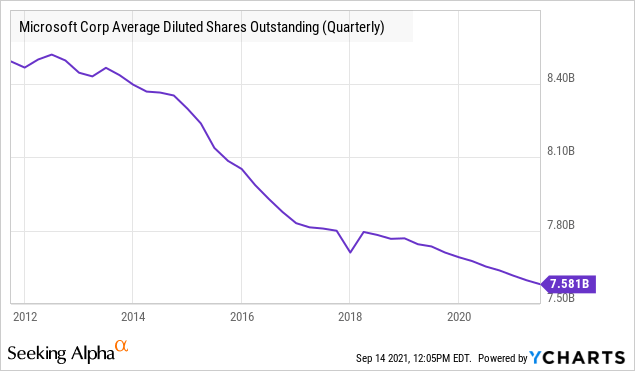

Microsoft is also actively buying back shares:

I proceed from the assumption that the dynamics of the last two years will continue, and by the terminal year, the number of diluted shares will be reduced to 7.2 billion.

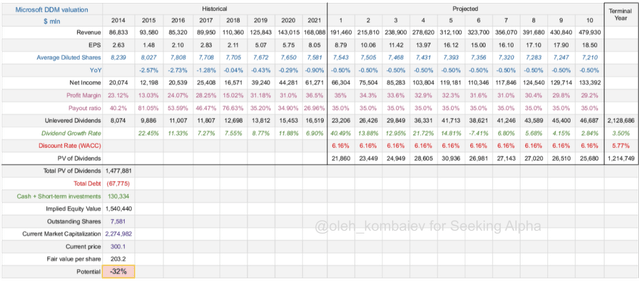

Here is the Dividend Discount Model:

The DDM-based target price for Microsoft's shares is $203 (-32%).

Let's summarize:

It is worth noting that I have already been observing similar results in the case of these companies for a long time. I mean, Apple and Microsoft tend to be undervalued in terms of future cash flow, and overvalued in terms of potential dividends.

This suggests that during periods of market growth, investors are not particularly inclined to pay attention to dividends. Moreover, most likely dividends are perceived simply as a bonus.

But during periods of market correction, the present value of potential dividends is the minimum level below which it is difficult for the price to fall. And in this context, I think Microsoft is in a better position than Apple.

Bottom line

At the current stage of the market cycle, when the likelihood of a correction has gone beyond formal, in my opinion, investing in Microsoft is less risky compared to Apple.