Summary

- Palantir, since its debut in 2020, has attracted the attention of many investors - both bulls and bears.

- The market performance of the company, however, has not lived up to expectations due to several negative developments.

- We believe growth investors should consider Palantir at this attractive entry point because of three main reasons.

This article was written by Nirasha Senanayake, CFA in collaboration with Dilantha De Silva.

Palantir Technologies, Inc. (PLTR), a big data and analytics company, can be best defined by its use cases such as capturing terrorists as well as building mission-critical customized solutions for the public and private sectors, and its stock has been having a rollercoaster ride over the past year. Following its IPO in September 2020 at a price of $10 per share, the stock reached a high of over $39 in February 2021, only to shed most of these gains over the last 12 months. In what was a remarkable year for all major U.S. market indexes, Palantir stock struggled in 2021 and is down more than 28% this year as well. This lackluster market performance prompted us to initiate coverage of Palantir to determine whether Mr. Market is missing something.

Palantir’s complex business structure together with the stock price action as a meme stock attracted the attention of many retail investors in its early days as a public company. While the company has been portraying impressive revenue growth as well as introducing many initiatives to promote future growth, we believe a few negative developments are overshadowing the fundamentals and the potential of the company.

On that note, we believe now is a good time to invest in Palantir stock, and our investment thesis is based on three reasons.

- High-value public and private sector opportunities.

- The changing shareholder composition.

- The attractive price point to initiate an investment in the company.

We will briefly discuss these three reasons below.

The opportunity

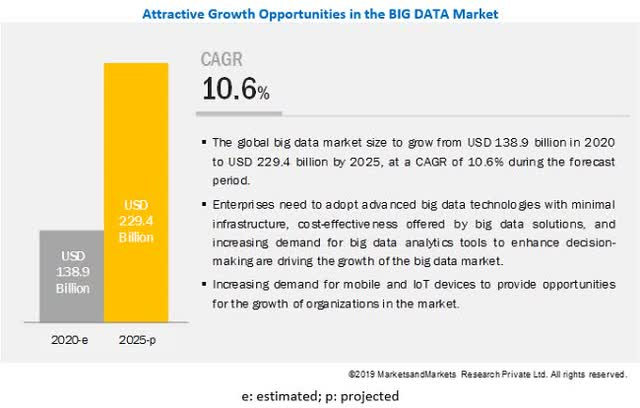

The first reason is the opportunity that prevails in the current market for the services provided by the company. Palantir’s software integrates organizations’ data from diverse sources and allows users to run analytics, identify trends, and make informed decisions using Artificial Intelligence. The two main platforms used by Palantir are Foundry and Gotham. Gotham is mostly used for government applications, whereas Foundry is for the private sector that allows businesses to interpret information feeds. The global big data market is expected to grow from $138.9 billion in 2020 to $229.4 billion by 2025, at a compounded annual growth rate of 10.6%. The major growth factors of the big data market include the increasing awareness of the Internet of Things (IoT) devices among organizations, increasing availability of data across organizations to gain deeper insights to remain competitive, and increasing government investments in various regions for enhancing digital technologies. This is a fast-growing market, as evident by these projections, and we believe Palantir is well-positioned to make the most of this favorable macroeconomic outlook.

Exhibit 1: The global big data market

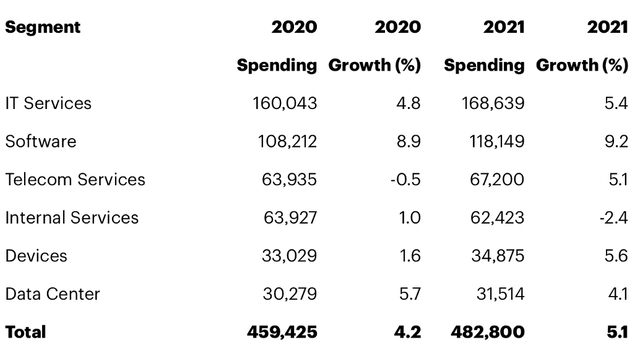

Looking at the recent deals secured by Palantir with Dewpoint Therapeutics and Hyundai Heavy Industries, there seems to be strong commercial potential for Palantir’s technologies. On the government front, off-the-shelf software solutions are given preference over bespoke solutions given the high costs involved in developing bespoke solutions. Gartner, in its worldwide government IT spending report released in February 2021, highlighted that spending will reach $483 billion in 2021, an increase of 5.1% from 2020. The software segment was expected to have the highest growth (9.2%) compared to 2020, which confirms the strong momentum behind government software spending.

Exhibit 2: Government IT spending forecast by segment

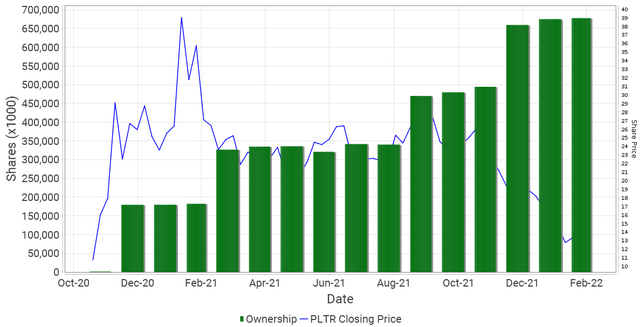

Second, the changing shareholder composition. The strong revenue growth portrayed by the company in the recent past did not receive due recognition in the market, in our opinion. The third quarter of 2021 is widely seen as a disappointing quarter for Palantir despite the company reporting year-over-year revenue growth of 35.5%, and this is mainly because of the decelerating growth of the government sector revenue. Palantir reported 34% YoY growth in the governmental segment revenue compared to 66% in the previous quarter, and this deceleration of growth did not impress the market. The commercial segment, excluding related party revenue, grew 23% YoY, and we believe this segment holds the key to the expected success of the company. Even though Q3 2021 revenue growth decelerated, Palantir continues to grow its topline every quarter, and given the favorable industry outlook as well as market opportunities, we believe the management guidance for 30%+ annual growth through 2025 is easily attainable. After looking at the recent price action in the market, we conclude that the market has always been pricing in higher revenue growth for Palantir in each of the last few quarters, and the otherwise impressive financial performance was overshadowed by these unrealistic growth expectations. Now that the hype is finally fading, we believe Palantir will attract the attention of investors who are in it for the long run, which in return could lead to reduced volatility in the stock while creating a platform for Palantir stock to drive on improving fundamentals.

Exhibit 3: Palantir institutional ownership

Third, the improving margin of safety resulting from the comparatively cheaper valuation. Although the company is making losses, the business is generating positive free cash flow with $320 million in FCF reported for the first three quarters of 2021, a massive year-over-year improvement from a loss of $285 million in the prior-year period. Palantir is currently trading at a P/S multiple of close to 17, which certainly does not make it the most cheaply valued tech company today, but in comparison to Snowflake, Inc. (SNOW) which is valued at a P/S multiple of more than 80, we believe Palantir’s expected growth justifies the current valuation. In any case, the company is more cheaply valued than it used to be just a few months ago – yes, it can get cheaper – and we strongly believe tech companies with competitive advantages will continue to be valued at better-than-average valuation multiples in the long run.

Two risks to monitor

The main red flag we see in Palantir is its excessive stock-based compensation. For a company that has been making losses every quarter and is only reporting profits on an adjusted basis, we feel the company is making life difficult for itself with this compensation structure as it negatively impacts the numbers reported by the company.

Second, we are keeping an eye on Palantir’s concentrated customer base. Already, the intense sensitivity of Palantir’s projects has resulted in investors being unable to forecast and assess the performance of Palantir’s software and its future operational performance. Palantir has only 203 customers in total, of which the top 20 customers account for over 50% of its revenue. This concentrated customer base makes it difficult to project future revenue and also poses a threat to the continued success of the company. Palantir, however, is adding new customers every quarter, and we will monitor these numbers closely to assess whether the company is on the right track to building a diversified pool of customers.

Takeaway

The road to recovery for Palantir is going to be a bumpy ride and investors will have to accept some volatility in the short run. With several government deals in the cards and the commercial segment gaining traction, we believe Palantir is on the cusp of entering a growth phase that would push the company into profitability. Palantir has not been this cheap for quite some time, and as growth investors, we are intrigued by what we are seeing today.