Summary

- Nvidia's earnings and guidance were nothing short of what investors have come to expect from it over the last year.

- But even with stellar guidance, the stock led the way in a red market on Thursday.

- The reason lies in the market's outlook for relatively slower growth over the year and the inability of Nvidia to maintain mid-double-digit revenue growth.

- I outline a new buy zone and where the stock is fairly valued in a year based on this recalibration of sales expectations.

It's become a pretty dull firework show with Nvidia (NVDA). Earnings beats and guidance raises are the norm, and the latest earnings report shows that's not changing anytime soon. But this quarter-after-quarter firework celebration is confusing investors as they watch the stock tumble further after already being sent into beaten-down territory the last several weeks. And to add insult to injury, there's nothing in the earnings report or the expectations for FQ1 to focus on negatively. In fact, things are coming along better than expected. However, the problem is the market facing down slowing FY23 and FY24 revenue growth and correlating it to a new valuation.

I'm not saying the party of Nvidia's shares is over, butI am sayingit's not going to be the lively dance club it once was. Even when management executes a quarter with $7.64B in revenue against a consensus for $7.42B and guides for a face-ripping quarter of $8.1B against estimates for $7.29B, it's not enough to overcome the ultimately slowing yearly sales growth.

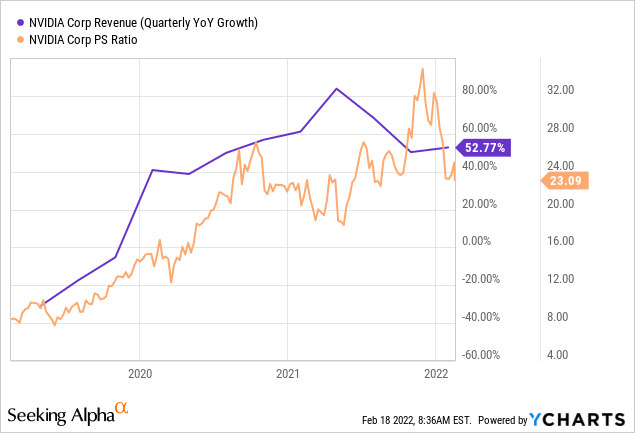

This is something I mentioned in my last article when I said I'd wait to add to my position due to the inability to achieve the growth the market was expecting at higher valuations. Shares traded just below $280 when I published the article. Some commenters didn't expect the stock would get to my buy zone at $264 even when I applied a forward price-to-sales multiple of 20 on the stock. But, as we know, the stock reached $264 and even less in the weeks following.

So what's this have to do with earnings?

Wednesday's earnings proved Nvidia - while able to crush estimates and guide significantly higher each quarter - cannot achieve the growth necessary to sustain the high valuation it once fetched.

The market pays for growth. If there isn't sustainable growth (read: the same level), there isn't a high(er) valuation awarded. The market also looks six-to-eight months out. This puts the view squarely at the end of the company's FY23.

Of course, estimates will rise - how could they not with an 11% guidance raise - but they won't be able to justify the 61% revenue growth 2021 just reported. Right now, estimates are predicting 28.5% revenue growth ($34.6B). This is higher than the 17% they expected two months ago, but this recalibration is now much closer to the real number after FQ1's guidance set the stage for the year. To achieve 60% growth, it would have to bring in $43B - about $9B more than the current estimate, basically a fifth quarter of the year.

Now, my take would be defensible if the stock was trading at the former high of $346. But, surely, the market can't be pricing in 60% growth for this year with the stock trading at $245.

And it's not.

But, the market perception is now shifting to a new valuation, one for 29% growth ($8.65B quarterly on average this fiscal year). This, however, is still 19 times forward sales. Of course, that's down from 26 forward sales, but 19 is still relatively high when growth is slowing and lapping high double-digit growth.

The question becomes, what does the market pay for an Nvidia with no Arm (ARMH) acquisition and slowing revenue growth amid a supply constraint semiconductor market? In a year where the next generation of gaming GPUs are likely to be launched, how will the company supply the demand it can't even fulfill for its current RTX3000 series? It's literally tapped out of supply, and incremental revenue will only be found with incremental wafer supply.

Therefore, the best bet on Nvidia is a bet on semiconductor shortages easing. But this is likely to come slowly and over time, not allowing for a spike in revenue to occur in any one quarter.

That being said, a historic valuation consistent with 30% revenue growth is more dependable and gives investors a chance to let the market recalibrate. This puts the stock closer to atrailing19 or 20 times sales.

This also means the market may ease it into the valuation over the next few months, as the hangover of 60, 70, and 80 percent growth rates fade into the rearview mirror. Using the current quarter (FQ1 '23) as a quarter in my calculation gives us $29.35B multiplied by 20 for a market cap of $587B, translating to a share price of $230 - 6% downside from Thursday's close.

This isn't a price target for a year out, but it's a fantastic risk-reward target to accumulate shares with a much lower level of risk.

Now, if we're going to discount the growth over the next two years closer to 20% (FY24 of $42B) and ease the multiple down to 18 or 19 (I'll use 18.5), the stock price comes out to $305, or 24.5% upside.

But this is going two years out, and estimating a discount the market may or may not be willing to grant it. But remember, the market will discount FY24 at the beginning of FY23, so while it's a two-year-out revenue estimate, it's a year-out price target.

And, if you're wondering about earnings and PE ratios, the growth rates are estimated to be nearly the same as revenue growth, implying margins aren't going to go any higher.

Add in the company didn't see "outperformance" on its gross margins, which some have pointed to as the "sole" reason the market sold off the stock on Wednesday's earnings, and it's fair to say there may not be anything left in the tank at this time for Nvidia to push the outperformance envelope to the level necessary for a return to all-time highs.

Nvidia not only has to continue to perform at the level it has (11% guidance raises and a beat on top of it at report time) but has to find an inflection in its business again; a new product or technology breakthrough. This is Nvidia, so this is very possible and even likely. However, any misstep will see the stock cut down in an instant at current valuations.

This isn't to say I don't like Nvidia; I'm happily long the stock and will continue to be. But detach your emotions for a few minutes, study what the market is doing to the stock and why, and you can recalibrate your mindset to be where the market will be in a year and not where it is today. Because today, the market is discounting the relatively slower growth eight months from now, and buying at risk-averse levels - $230 and below according to my calculations - you'll have a much larger position with a company growing revenues into FY24 and FY25 in the low 20s and high teens, at minimum.