FOMC June meeting, How to determine the trend of assets in H2?

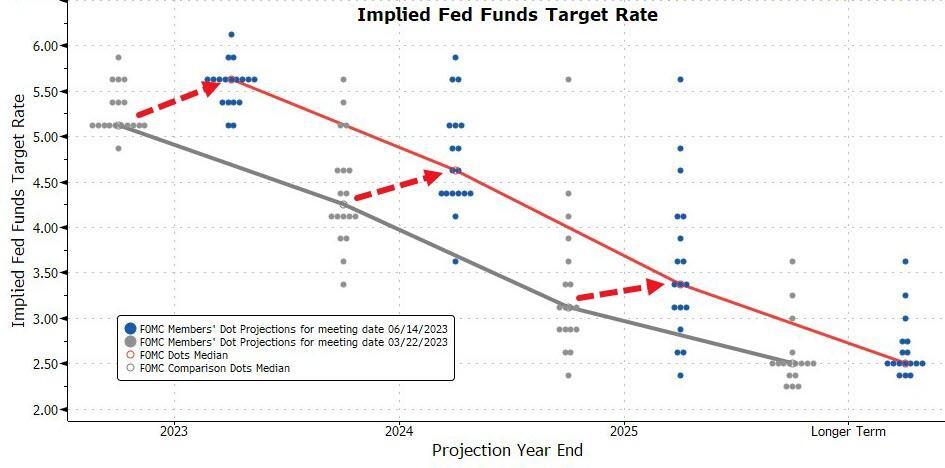

The Federal Reserve maintained its position and met market expectations during the June meeting. However, the major change was a significant upward adjustment in the dot plot, with the Fed now expecting two more interest rate hikes within the year, which exceeds market expectations.

This hawkish stance is driven by the resilience of the US economy and persistent inflation, especially stubborn core inflation, which has compelled the Fed to consider raising interest rates. Nonetheless, the Fed doesn't want to hike too quickly, hence they have chosen a "steady progress" approach for now and refrained from raising rates in June.

Overall, we believe the Fed has a strong inclination to continue raising rates if the upcoming data remains stable. For instance, if GDP, unemployment rate, and other data perform better than expected, the Fed will lean towards further rate hikes and is likely to continue raising rates in July. From another perspective, if credit tightening measures are insufficient, monetary tightening will require additional measures. Therefore, there is a high probability of the Fed continuing to raise rates in July as long as the data remains favorable. The Fed may still lean towards progress and continue raising rates in the second half of the year.

Why was there a significant upward adjustment in the rate hike guidance? The reason lies in the resilience of the US economy and the persistence of core inflation.

Since the beginning of this year, the US economy has outperformed expectations, and core inflation has shown strong resilience. In response to this, the Fed has raised its economic growth forecasts in this round of economic projections, and the adjustments made were substantial, indicating reduced concerns about a recession.

Regarding inflation, although the Fed slightly lowered its forecast for year-end PCE inflation, it raised the forecast for core PCE inflation. This also explains why the Fed needs to raise policy rates to higher levels, and rates are expected to remain at high levels for an extended period of time.

However, why didn't they raise rates at this meeting? One explanation is that the Fed intends to slow down the pace of rate hikes. As the effects of rate hikes become apparent in interest rate-sensitive sectors such as real estate and banking, the Fed doesn't need to raise rates as rapidly and aggressively as it did last year. "Skipping" a rate hike at this June meeting is precisely to slow down the pace of rate hikes, which also helps reduce financial risks. However, Powell emphasized during the meeting that slowing down rate hikes does not mean they won't raise rates anymore; it is done to gain clearer insights and make more precise decisions.

Another reason is the substitution relationship between credit tightening and monetary tightening. Despite the significant rate hikes by the Fed since the second half of last year, financial conditions have remained accommodative, and the suppressive effect of rate hikes on the economy, especially consumer spending, has not been evident. In the first half of this year, three banks, including Silicon Valley Bank, filed for bankruptcy. This event could have triggered a spontaneous credit tightening in the market. However, the Fed promptly intervened to provide support, and financial conditions did not further tighten. If credit tightening measures are insufficient, more monetary tightening may be necessary.

Regarding growth and inflation, Powell stated that they only see early signs of a slowdown in inflation, and the tightness in the labor market is gradually easing but still needs to be sustained. Powell said, "The labor market has remained very strong in the past few months." Meanwhile, Powell also maintained his belief in a "soft landing" scenario where inflation moderates without a significant downturn.

Considering that the effect of US credit tightening may accelerate in the third quarter (corresponding to a year-on-year contraction in commercial loans and a slowdown in consumer loans), it becomes the main driving force suppressing demand.

However, slow release of excess savings (expected to be completed in the first and second quarters of 2024) will prevent a "cliff" in demand. Consumer demand still shows resilience. Under the pressure of low-income individuals struggling to make ends meet and a sharp decline in self-employment, supply growth may rapidly close the employment gap and suppress wages. The core and overall CPI are expected to approach 3% in the third quarter and reach 3% by the end of the year, pushing the unemployment rate close to 5% by the end of the year.

Most analysts in the market assume a "soft landing" for the second half of this year. Overall, the tone of this meeting is leaning towards hawkishness, reinforcing the expectation that interest rates will remain high for a longer period. This helps to keep financial conditions in a relatively tight range and puts some pressure on overvalued areas of the gold and stock markets. Economists believe that the FOMC needs to take more aggressive actions than expected to curb inflation, and it is expected that there will be at least two 25 basis point rate hikes this year. Among the 42 economists surveyed from June 5th to June 7th, 67% of them predict that the federal funds rate will peak between 5.5% and 6% this year, an increase from the previous survey's 49%.

The macro and policy paths may become clearer after Q3, with the main theme being a rapid decline in inflation but resilient growth, gradually halting rate hikes (or a nonlinear acceleration of rate cuts, directly avoiding rate hikes). In Q4, the pressure on growth may increase, and overall inflationary pressures in the fourth quarter may be greater, until the expectation of rate cuts becomes clear.

US Stocks: As growth pressures gradually increase in the second half of the year, the current high valuations and low risk premiums suggest that there may be disturbances under the pressure of subsequent growth, but not a trend reversal. Certain industries and concepts with significant potential, such as AI and chips, will still receive "safe haven-like" favor from investors. $NASDAQ(.IXIC)$ $DJIA(.DJI)$ $S&P 500(.SPX)$

US Bonds: Short-term rates are around 3.8% and may decrease after expectations of easing intensify. The reasonable level of the 10-year Treasury yield in the short term may be between 3.5% and 3.8%. Considering that the Treasury Department will need to issue new bonds to replenish the TGA account after resolving the debt ceiling, the increase in short-term bond supply may provide upward momentum to US bond yields. $iShares 20+ Year Treasury Bond ETF(TLT)$ $US Treasury 3 Month Bill ETF(TBIL)$ $iShares 0-3 Month Treasury Bond ETF(SGOV)$ $iShares Short Treasury Bond ETF(SHV)$

Gold: Safe-haven and rate-cut expectations have been partially adjusted, with expectations leaning towards the bullish side, awaiting the next catalyst of recession and rate-cut expectations. $SPDR Gold Shares(GLD)$ $Gold - main 2308(GCmain)$

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.

Interesting insights on the future path of macro and policy. I'll keep an eye on inflation and growth.