What Makes Microsoft and Google's Q2 Divergence?

Abstract

The recession expectations makes the market's outlook for first-half advertising revenue rather pessimistic, making it easier for advertising performance to beat.

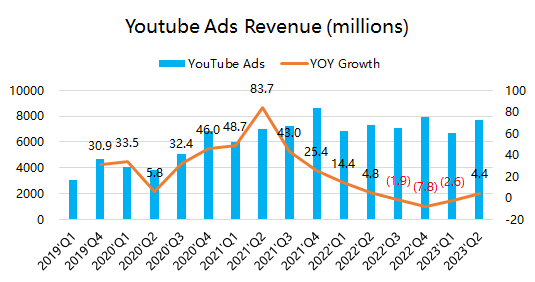

$Alphabet(GOOGL)$ YouTube business has experienced growth under short video competition, affirming the rise in Shorts' market share.

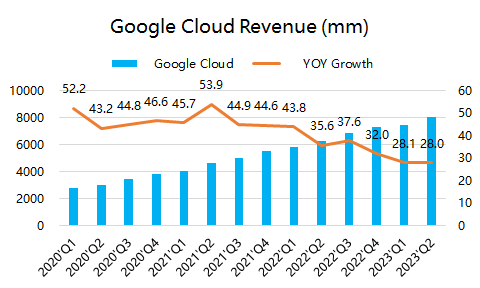

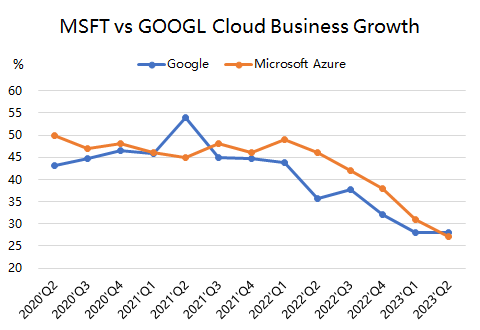

Google Cloud maintains a relatively high growth rate, surpassing Microsoft Azure's single-quarter growth rate for the first time since Q3 2021.

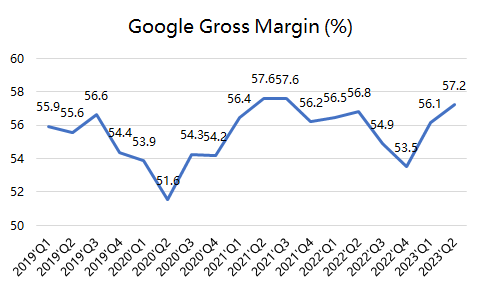

Margins have reached new highs due to cost reductions and increased efficiency, with gross margins peaking at 2021 levels, leading to an improved annual outlook.

The market perceives that Google may monetize AI earlier than Microsoft.

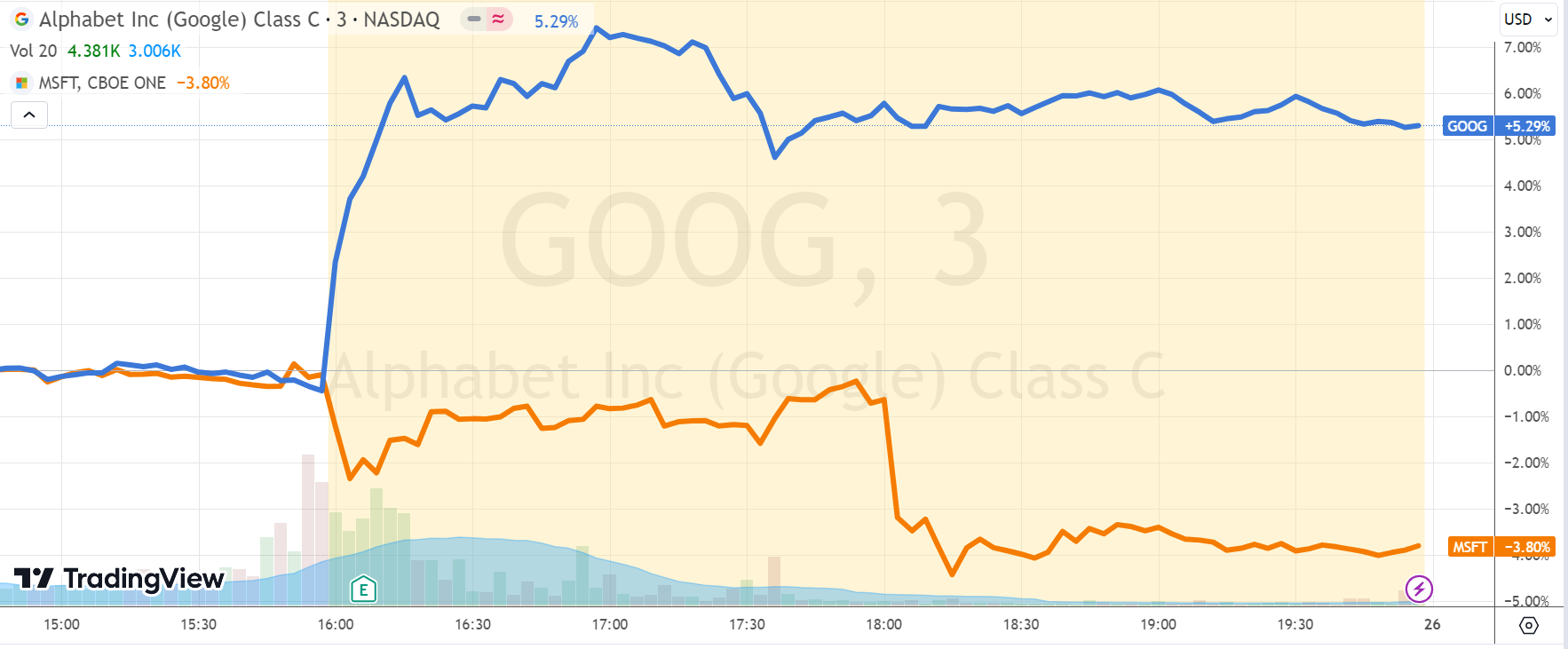

July 25th, after-market trading, $Alphabet(GOOG)$ and $Microsoft(MSFT)$ simultaneously released their financial reports, providing an opportunity for a direct comparison of the two AI giants. Google's stock surged 7% after reporting results significantly above expectations, while Microsoft, though also beating market consensus, experienced a 2% drop. Is there a double standard in the market's evaluation?

We believe that it's premature to directly compare Google and Microsoft's financial reports, and the contrasting post-market trends are a result of "expectation comparisons" in the market.

Why did Google's financial report significantly exceed expectations?

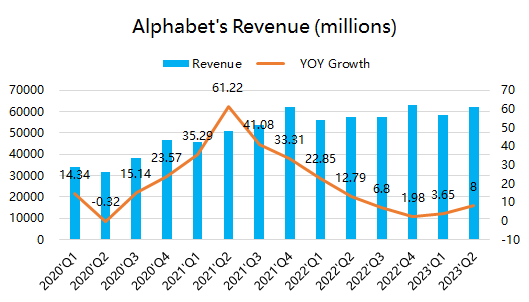

In Q2, the revenue reached $74.604 billion, far surpassing the market's expected $72.77 billion, with a year-on-year growth rate of 8%, the highest since Q2 of the previous year, rebounding after recession expectations.

Google's service revenue, including advertising, search, maps, YouTube, hardware, Android, Chrome, and Google Play, reached $66.285 billion, growing by approximately 5.5% YoY. As known to all, Google's main source of revenue is advertising, and in Q2, Google's advertising revenue returned to growth, with a YoY growth rate of 3.3%.

YouTube's advertising revenue, which has been increasingly focused on short videos, reached $7.665 billion, showing a growth rate of 4.4% YoY, rebounding after three consecutive quarters of decline. The market had expected growth to be only 1%.

In addition, the cloud business, with the highest growth rate, generated $8.031 billion in revenue, continuing the nearly 30% high growth rate, higher than the market's expected slowdown, with its operating profit rising from $191 million in Q1 to $395 million.

Overall, the company's profit has rebounded, with a gross profit margin of 57.2%, basically returning to the level of 2021, and administrative expense growth has decreased due to layoffs. The diluted EPS was $1.44, higher than the market's expected $1.32.

We believe,

1. Advertising business surpassed expectations, dispelling market concerns about ChatGPT's impact on Chrome's market share and the decline in advertising under recession expectations.

2. YouTube's advertising rebound proved its continued advantage in the competition with short videos.

3. Cloud business maintained a high growth rate, leading to higher expectations for its further acceleration in the AI era.

4. Cost reduction efforts exceeded market expectations, supporting the company's valuation in terms of profit multiples.

Google's phone conference emphasized AI as the company's top innovation priority.

The company has been at the forefront of artificial intelligence for seven years and knows how to better integrate AI into its products. Key points include the use of large language models like PaLM2 and upcoming models like Gemini to reimagine products, particularly search, due to the "very positive" feedback on the Search Generative Experience.

The company is also testing and improving ad placements and formats, providing advertisers with AI-generated tools. Android 14, the latest operating system, will also incorporate AI tools.

What makes Microsoft plunge, Google surge?

Microsoft's Q2 performance also exceeded expectations on various levels. After integrating GPT into Bing Search, there was obvious growth, but the direct impact of AI on revenue in Windows and Office is yet to be fully demonstrated. This is likely one reason why Microsoft priced Office Copilot at $30 per month.

We believe that the market's response is mostly a reflection of "expectations

1. Expectations for Google were too low, and expectations for Microsoft were too high. Both Google and Microsoft are far from mature AI monetization in Q2, and the market's valuation on this factor is premature, with Microsoft receiving a more thorough evaluation.

2. Direct comparison of cloud business. This quarter marks the first time since Q3 2021 that Google Cloud's growth rate surpassed Microsoft Azure's. While maintaining a growth rate of over 20% as the largest cloud service provider is challenging, the market will still make comparisons.

3. From the conference call's expectations, Google will focus more on applying AI to its advertising business. Given Google's large advertising base and the fact that advertising is one of the most profitable businesses, the market may believe that Google, although lagging behind Microsoft in LLM, will monetize earlier.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.

Same same but different