How Arm became the largest IPO in three years?

August 21st, Arm Holdings, the British semiconductor IP giant under $Softbank Group Corp(SFTBY)$ , officially submitted its IPO documents to the U.S. Securities and Exchange Commission, revealing its financial details and initiating the IPO process.

The company will trade under the code "ARM." Previously, it was reported that Arm had hired 28 brokerage firms to act as underwriters for its IPO. Established in 1990 as a joint venture between Acorn Computers, $Apple(AAPL)$ , and VLSI, Arm went public on the $LONDON STOCK EXCHANGE GROUP PLC(LSE.UK)$ and the $Nasdaq(NDAQ)$ from 1998 to 2016.

In September 2016, it was acquired and privatized by Japan's SoftBank Group for $32 billion. In 2020, SoftBank attempted to sell Arm to $NVIDIA Corp(NVDA)$ for $40 billion, but the deal fell through in February 2022 due to excessive pricing.

Company Introduction

Arm is a leading semiconductor technology company focused on designing, developing, and licensing high-performance, low-cost, and energy-efficient CPU products and related technologies. As of December 31, 2022, the company's energy-efficient CPUs powered over 99% of global smartphones, with more than 250 billion chips driving devices ranging from small sensors to powerful supercomputers. Arm's CPU products run the majority of software worldwide, including smartphones, tablets, personal computers, data centers, network devices, vehicles, smartwatches, thermostats, drones, and industrial robots with embedded operating systems. The company's energy-efficient CPU IP and unparalleled technology partner ecosystem allow any company to manufacture modern computer chips, achieving cost-effectiveness through a flexible business model. Each CPU product can be licensed to multiple companies, enabling economies of scale.

With the exponential growth in CPU design complexity, no company has successfully designed modern CPUs from scratch over the past decade. The company has been at the forefront of computational technology innovation for decades and has established crucial relationships with companies driving the future of various industries.

As of the fiscal year ending on March 31, 2023, over 260 companies have shipped Arm-based chips, including major technology companies like $Amazon.com(AMZN)$ , $Alphabet(GOOG)$ leading semiconductor chip suppliers such as $Advanced Micro Devices(AMD)$ , $Intel(INTC)$ , NVIDIA, $Qualcomm(QCOM)$ , and $Samsung Electronics Co., Ltd.(SSNLF)$ , established automotive companies, leading automotive suppliers, and IoT innovators.

Arm’s Products and Service

Arm's solutions encompass a wide range of products, offers the world's most widely used CPU architectures, including:

Arm CPUs. At the core of the company's offerings are market-leading CPU products that utilize the company's versatile and scalable ISA to meet a wide range of performance, power, and cost requirements.

Graphics Processing Units (GPUs). The company provides a range of GPU products, delivering optimal visual experiences for various devices.

System IP. Complementary design components empower designers to create high-performance, low-power, reliable, and secure chips.

Compute platform products. Arm's CPUs, GPUs, and system IP are integrated into a foundational compute platform optimized for specific end markets.

Development tools and software. The company's tools and software support the development and deployment of its products.

The company continually expands the scope of its product offerings, investing in more comprehensive designs tailored for end markets, extending beyond subsystem design. Recognizing the complexity of developing chips using state-of-the-art manufacturing processes, the company is heavily investing to better support an increasing number of OEMs in developing their customized chips.

Furthermore, the company nurtures an extensive ecosystem of third-party hardware and software partners to support its customers.

Partners include leading semiconductor technology suppliers, such as semiconductor foundries like $GLOBALFOUNDRIES Inc.(GFS)$ , $Intel(INTC)$, $Taiwan Semiconductor Manufacturing(TSM)$, $United Microelectronics(UMC)$, as well as EDA vendors like $Cadence Design(CDNS)$ , $Synopsys(SNPS)$ , and $Siemens AG(SIEGY)$

The company also invests in its software ecosystem, collaborating closely with firmware and operating system providers, such as Amazon Linux, Canonical Ltd., Google LLC, $Microsoft(MSFT)$ , $Red Hat(RHT)$, $VMware(VMW)$, Wind River Systems, Inc., game engine suppliers like $Unity Software Inc.(U)$ and Epic Games, software tool providers including Green Hills Software LLC, IAR Systems AB, and Lauterbach GmbH, as well as application software developers like $Adobe(ADBE)$ , $Electronic Arts(EA)$ , King.com Ltd., and others.

The breadth of the company's solutions combined with its software ecosystem, used by millions of chip design engineers and software developers, creates a virtuous cycle. Software developers write software for Arm-based devices due to its vast market reach, while chip designers choose Arm processors because of the extensive software application support.

Advantages of Arm CPU products include: High Performance, Low Power Consumption, Scalability.

Financial Performance

Since its inception, Arm has shipped over 250 billion chips and boasts more than 15 million software developers.

According to IPO documents, Arm estimates that around 70% of the global population uses products based on Arm architecture. In the fiscal year 2023 ending on March 31, 2023, Arm's chip shipments exceeded 30.583 billion, a growth of approximately 70% compared to the fiscal year 2016.

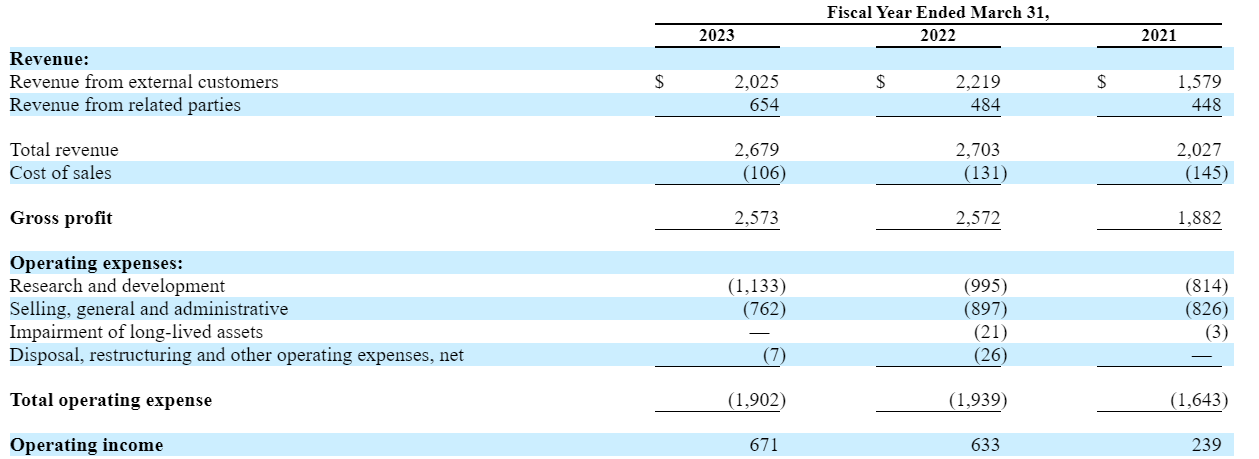

For the fiscal years 2021 to 2023, Arm's annual revenues were $2.027 billion, $2.703 billion, and $2.679 billion, respectively. During the same period, the gross profit margins were 93%, 95%, and 96%, while the net profits were $388 million, $549 million, and $524 million, respectively. Research and development expenses accounted for 40%, 37%, and 42% of the respective annual revenues during the same period. The decline in revenue in the fiscal year 2023 was mainly influenced by the global decrease in smartphone shipments. In the latest fiscal quarter ending on June 30, 2023, Arm's quarterly revenue decreased by 2.5% compared to the same period last year, reaching $675 million, and net profit decreased from $225 million in the previous fiscal year to $105 million.

From a geographical perspective, during the fiscal years 2021-2023, revenues from mainland China accounted for approximately 21%, 18%, and 25% of Arm's total revenue respectively. In the Chinese region, there exists Arm China (AnMou Technology) company, which is directly controlled by SoftBank, and Arm does not possess voting rights.

Looking at customer distribution in the fiscal year 2023, the top five customers contributed to 57% of the total revenue, while the top three customers accounted for 44% of the total revenue. The largest customer represented 24% of the total revenue, the second and third largest customers contributed 11% and 9% of the total revenue respectively.

In terms of revenue sources, the two business models of licensing and royalty differ in their approaches. Royalty income is predominant, constituting 50%, 40%, and 55% of the total revenue in the fiscal years 2021-2023. The licensing model involves payment based on the number of IP authorizations, essentially a one-time product authorization fee, whereas the royalty model is based on the number of manufactured chips, with costs tied to sales volume.

Opportunities and Challenges

Arm's Total Addressable Market (TAM) encompasses various sectors including smartphones, personal computers, digital televisions, servers, automobiles, and network devices such as main controller chips. It was estimated to be around $202.5 billion in 2022 and is projected to reach approximately $246.6 billion by 2025 at a compounded annual growth rate of 6.8%.

Apart from the mobile application processor market, there is potential for more growth from Internet of Things (IoT) devices and the cloud computing market.

Given the critical role of CPUs in all AI systems, efficient handling of AI workloads, whether through co-processor integration, large language models, generative AI, or low-power acceleration in emerging fields like autonomous driving, is of paramount importance. Consequently, Arm has incorporated new features and instructions into its latest ISA, CPU, and GPU designs to accelerate future AI and machine learning algorithms, thus aiming to expand its market share in the AI industry.

Of course, the complexity of cutting-edge solutions also translates to continuously increasing costs for the company, as substantial resources are required for the development of advanced products.

As process technology nodes continue to shrink, there has been a sustained exponential growth. According to market research firm IBS, the IC design cost for 7nm chips is approximately $249 million, while the IC design cost for 2nm chips is around $725 million. Design partners are enhancing innovation and boosting customer competitiveness by reducing the complexity, risks, and costs of critical development phases and thereby advancing their market position.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.

Great catch! ARM is largely news anyway - RISC-V processors are the future. The licensing revenue will continue to dwindle. This IPO is really just there to improve SoftBank's terrible marks.

Softbank’s current market cap is 65 billion. They fully own ARM. They want to list it at a value between 60 and 70 billion. If they succeed, they could sell shares in ARM and buyback their own stock, basically taking back the ARM shares and doing free buybacks on the rest of the company.

could have a massive run up once ARM ipo's next month. SFTBY will ipo 10% of their owned shares to bring back into Softbank's cash flow.

let's go, intel. back to all time highs and make everyone use your services. u better start making ARM chips!

If SoftBank is selling it means doomsday. I will stay away from this. Thanks