Oracle Down 13%? It's an over-estimate correction

$Oracle(ORCL)$ dropped 13% after release of FY24Q1 earnings report as of August 31. The decline was primarily attributed to lower-than-expected cloud licensing revenue, leading investors to question whether the company could meet its AI-related expectations.

However, despite this setback, Oracle has seen a year-to-date increase of over 35%, making it the second-best year since the internet bubble of 2000. It is much like a correction following overly optimistic expectations.

Earnings Overview

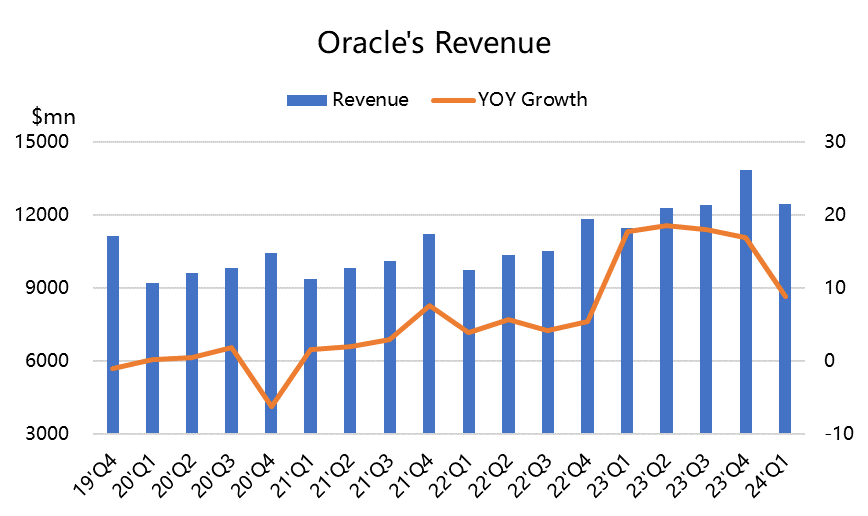

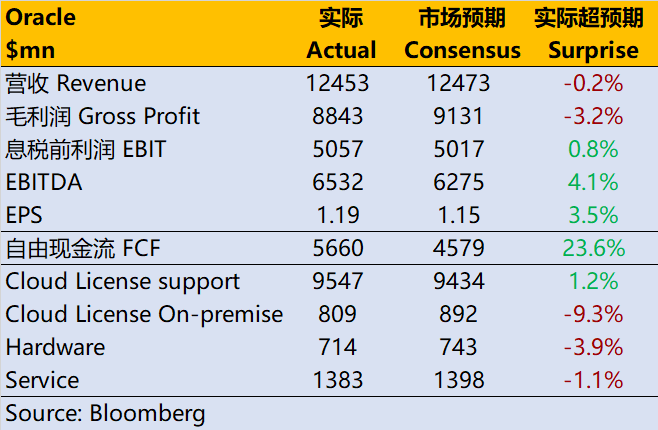

- Revenue: $12.45 billion, a 9% year-on-year increase, slightly below the market's expected $12.47 billion.

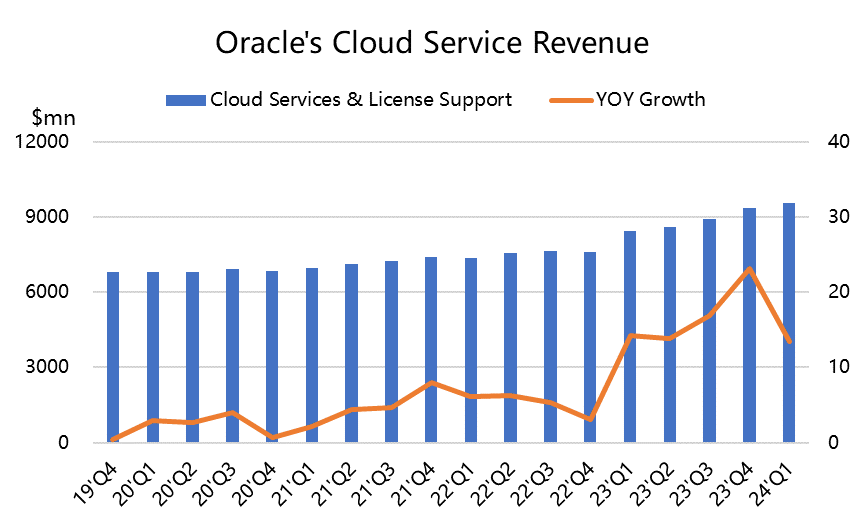

- Cloud revenue: $4.6 billion, a 29% year-on-year increase at constant exchange rates, down from 55% in the previous quarter.

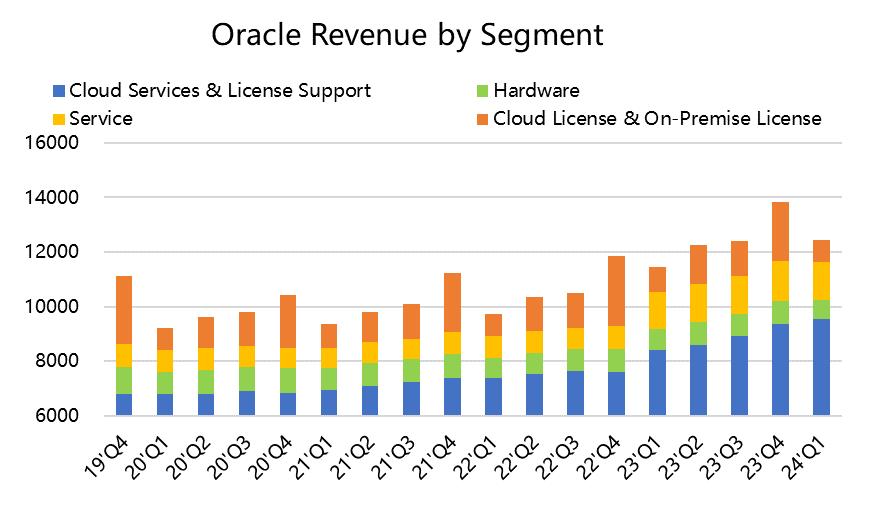

- Cloud services and license support department revenue: $9.55 billion, a 12% year-on-year increase, slightly higher than the market's expected $9.43 billion.

- Cloud license and on-premises license department revenue: $809 million, an 11% decrease at constant exchange rates, lower than the market's expected $890 million.

- Hardware department revenue: $714 million, an 8% year-on-year decrease, lower than the expected $743 million.

- Services department revenue: $1.38 billion, a 1% year-on-year increase, lower than the expected $1.4 billion.

- Gross margin: 71.01%, below the market's expected 73.79%.

- Comparable EBIT: $500 million, in line with expectations.

- Non-GAAP adjusted EPS: $1.19, a 15.5% year-on-year increase, higher than the market's expected $1.15.

Overall, the better-than-expected profit performance was mainly due to cost reduction efforts, while revenue bottlenecks became more evident.

Guidance:

- The company expects revenue for the next quarter, including Cerner, to grow by only 3% to 5% year-on-year at constant currency, below market expectations.

- Cloud revenue is projected to grow by 27% to 29% in constant currency.

- Non-GAAP EPS is expected to be between $1.27 and $1.31 in constant currency, representing a 5% to 9% growth.

Investment Highlights

The disappointment in Oracle's Q1 performance justifies short-term selling. The market may have been overly optimistic about the company's growth in the AI era.

In terms of Q1 performance, Oracle obviously disappointed investors, and short-term selling seems reasonable. The market may be more aggressive toward the company's growth in the AI era.

In fact, upon closer examination, the quarterly year-over-year growth of 40%-50% is obviously unsustainable in the long term, and Oracle's cloud services growth will inevitably return to a normal trajectory. What's more important is that, compared to its giant peers, Oracle's Infrastructure as a Service (IaaS) remains relatively small in scale, and its growth and profitability still depend on its Software as a Service (SaaS) driving factors.

Looking at the stock price, the company reached an all-time high after the last quarter's earnings report and has returned to this position before the current earnings announcement, indicating high market expectations for the company. The market is optimistic that Oracle's generative language models in its cloud services will help it gain a larger market share in the AI competitive era.

According to information from the conference call, AI companies have purchased over $4 billion in Oracle Gen2 Cloud contracts, which is twice the volume booked at the end of FY23Q4 last quarter, thus boosting their organic cloud revenue growth by 29%.

Furthermore, based on the CAPEX outlook as a leading indicator, the company expects CAPEX for fiscal year 24 to be similar to the previous year, thereby lowering expectations.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.

I was puzzled about oracle’s stock price for a long time, it is no longer the tier one or even tier two companies in Silicon Valley, their pay won’t keep the best people /talents in the field. And the competitors of cloud business like Amazon, msft, Google are much better bets from many aspects… and how the stock price becomes this much higher than pre-Covid time, and their PE is higher than many well known companies with real AIs…

Well I was in positive territory. But definitely not now. Hmmmm, what to do next.

They are late to the games, and want to buy your shares as low as they can.