Is Sea in danger now?

$Sea Ltd(SE)$ released its Q3 financial report for 2023. The three main business segments - gaming, e-commerce, and finance - showed mixed results. While the gaming sector remained profitable, the e-commerce division experienced a significant decline in profits, and the finance segment performed well but relied heavily on e-commerce.

Although the market had already anticipated that Shopee would return to losses and erase this year's profits by focusing on volume over price, it was surprising to see that the losses were even greater than expected. This has raised doubts among investors regarding the growth achieved through this strategy.

As a result, Sea opened at a -12% decline in the US stock market and continued to drop throughout the day, ultimately closing at -22%.

Q3 Report Overview

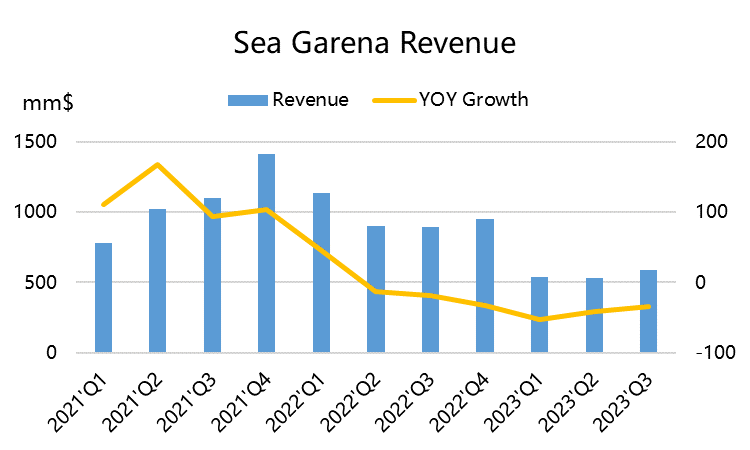

Garena, the gaming division, generated $448 million in revenue, which was relatively stable compared to the previous quarter. GAAP revenue reached $592 million, a 34% decrease compared to the same period last year but slightly higher than the expected $556 million. Adjusted EBITDA was $230 million, slightly surpassing market expectations of $222 million. The gaming business has matured, allowing for effective control of profit margins.

This outcome is due to the decline of Sea's flagship game, Free Fire, and its exit from operating League of Legends in the Taiwan region of China.

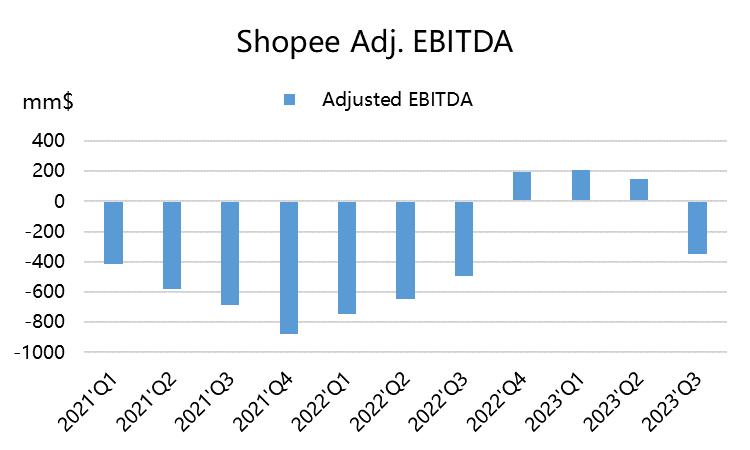

Shopee, the e-commerce business, achieved a 5% year-on-year growth in Gross Merchandise Volume (GMV), reaching $20.1 billion, slightly higher than the expected $17.3 billion. The number of orders increased by 13%. However, Shopee incurred an operating loss of $430 million, significantly higher than the $590 million loss in Q3 of the previous year. Adjusted EBITDA was -$346 million, far below market expectations of -$49 million.

Sea Money, the finance division, continued its high-speed growth with revenue of $446 million, a 37% increase. However, this was slightly lower than the expected $448 million. Adjusted EBITDA was $165 million, surpassing market expectations of $148 million. The outstanding loan balance reached $2.4 billion, a $2 billion increase compared to the previous year, and the bad debt rate for loans overdue for more than 90 days decreased to 1.6%.

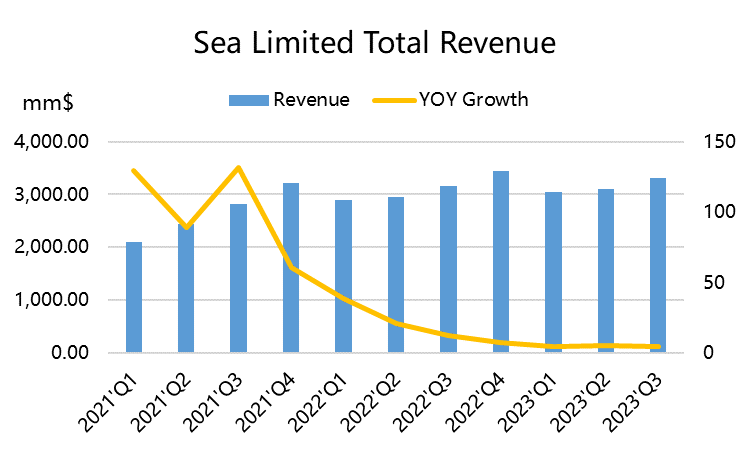

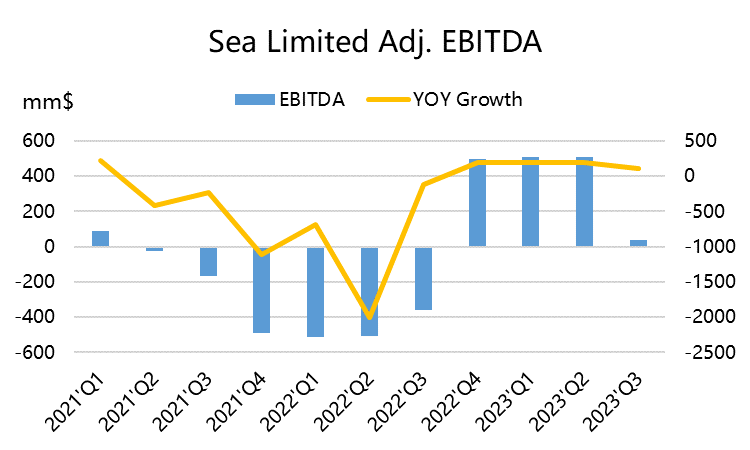

Overall, the company achieved total revenue of $3.31 billion, a 5% increase compared to the same period last year and higher than the expected $3.19 billion. Adjusted earnings per share were $0.06, lower than the expected $0.29.

Investment Highlights

1. Can the e-commerce business make success again?

The unexpected massive loss of $430 million in the e-commerce division indicates unsustainable growth. Sea previously exited the competitive Brazilian market due to its inability to sustain this loss-making model and adopted a lighter operational model with higher profit margins.

However, this quarter's loss was mainly caused by a significant 7% decrease in average order value, indicating that this growth achieved primarily through price reductions is not healthy. Additionally, marketing expenses skyrocketed from $490 million in the previous quarter to $920 million, surpassing even Q2 of 2022. This suggests intense competition in the market.

Currently, both Lazada, which has made a comeback under Alibaba's leadership, and TikTok are strong competitors in the e-commerce sector.

2. The gaming business is still relying on old profits.

Although Q3 revenue and operating profit are significantly better than expected, market expectations have been lowered by a lot, so a year-on-year decline of 34% is not a good result.

But more importantly, the operational data is also performing poorly, with a continued decrease of one million in quarterly active users and a decrease of two million in paying users. We mentioned two quarters ago that "Free Fire" has entered a decline phase, and the previously released new games have not reached such heights yet. The future release of new games will also require some time, and it may not be able to replicate the miracle of "Free Fire". Relying solely on agent games cannot achieve the goal of recovery, so the company is focusing on maintaining the profitability of the gaming business while the active users and revenue decline.

3. The financial business is growing rapidly, but focusing on quality.

The financial business is growing, with a 34% revenue growth rate in Q1. On one hand, it is due to the rapid growth of payment business related to e-commerce, and on the other hand, it is due to lending. As the tight credit cycle follows the tight monetary cycle, loan quality is also a key factor affecting the company's profitability, but the company is performing well.

The balance of outstanding loans at the end of this quarter is $2.4 billion, an increase from the previous quarter, and the bad debt ratio for loans over 90 days has decreased to 1.6%.

However, as a payment business more related to e-commerce, it may also change with the rise and fall of e-commerce business. And currently, there has been a "slightly lower than expected" growth rate in revenue, and high growth may also enter a bottleneck period. The market is now more concerned about profitability.

Outlook

What does the market feedback after the financial report represent?

Mainly insufficient expectations and concerns about the market competition environment. Institutional investors would rather miss out than share risks.

Coincidentally, many funds have recently announced their 13F filings, and we can see that SE's major investors have mostly increased their holdings to some extent in transactions after the Q2 financial report (which is in Q3), including FMR, Tiger Global Fund, and PRICE T ROWE. Among the major institutional investors, there have been noticeable reductions in holdings by BlackRock (BLK) and Capital Research Global.

These institutions that increased their holdings in SE in Q3 are obviously more likely to sell off their holdings in a stepping manner after seeing such a Q3 financial report, which is also an important reason for the 22% significant drop during trading.

Is e-commerce in Southeast Asia profitable or not? Sea still needs to prove it with financial reports, but now insiders will "subsidize billions", and Sea obviously cannot rely on this anymore.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.

- suv·2023-11-15SE was supposedly to take advantage with Tik Tok being banned of ecommerce in Indonesia. Why SE failed? What will happen to SE, if Tik Tok finds a way to do ecommerce there?1Report