BIG TECH WEEKLY | 2024 Preview: Big techs in interest rate cuts (2)

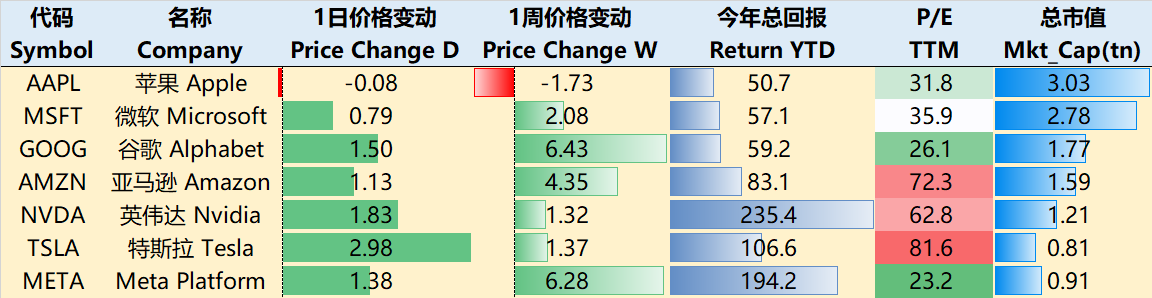

Big-Tech’s Performance

Last two weeks of 2023, market continued new highs, with big-techs taking turns to perform. Meta and Amazon reached new highs for the year this week.

As of the close on December 21st, the performance of major technology companies in the past week showed the following changes: $Alphabet(GOOGL)$ $Alphabet(GOOG)$ +6.43%, $Meta Platforms, Inc.(META)$ +6.28%, $Amazon.com(AMZN)$+4.35%, $Microsoft(MSFT)$ +2.08%, and $NVIDIA Corp(NVDA)$ +1.32%, $Tesla Motors(TSLA)$ +1.37%, $Apple(AAPL)$ -1.73%.

Big-Tech’s Top Newsfeed

- Apple will stop selling the latest version of the Apple Watch in its U.S. retail stores and is exploring a "rescue operation" to save the $17 billion Watch business.

- Apple is ramping up production of Vision Pro in China and plans to launch it in February next year. IDC predicts a 46.4% year-on-year increase in AR/VR headset shipments in 2024, driven mainly by Meta's Quest 3 and Apple's Vision Pro.

- The Information revealed that Google plans to restructure its advertising sales department on a large scale.

- Intel has released the Gaudi 3 processor, claiming that its performance exceeds Nvidia's H100.

Big-Tech’s Key insights

How will Big-Techs perform in 2024?

Bloomberg's consensus forecast: Revenue for 2024 is expected to be $342.249 billion, with a year-on-year growth rate of 11.96%; EBIT profit margin is expected to increase by 16.76% to a new high of 28.90%.

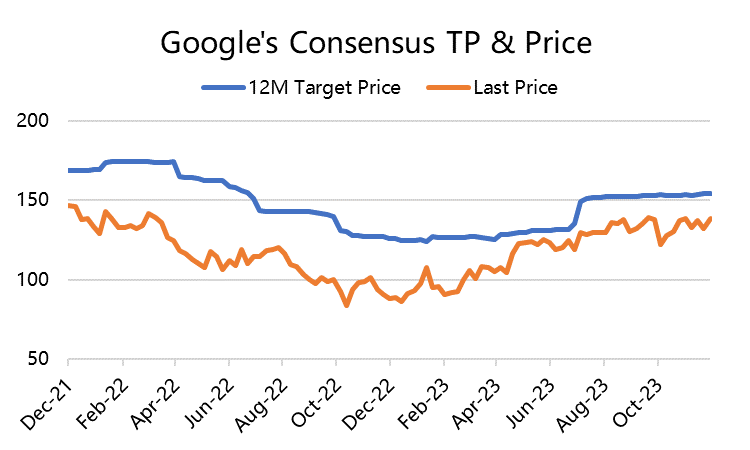

The target price expectation is $154.31, with a 9.96% premium over the current price of $140.42. If it weren't for the 9% drop after the Q3 financial report, it would likely have reached a new high for the year.

Google's main source of revenue is advertising, which was greatly underestimated in the first half of 2023 under conditions of high inflation and economic pessimism, resulting in consistently exceeding expectations after the financial report. The strength of Google's advertising revenue is not only due to the "soft landing" of the macro economy, but also several key factors:

1. YouTube's position is unshakable, and it has successfully responded to competition from short videos such as TikTok and Reels by launching Shorts.

2. The Chrome browser did not lose market share due to the emergence of ChatGPT; instead, it improved advertising monetization efficiency through AI business.

3. Advertisers who fear losing market share due to price increases are actually competing within the most efficient channels, giving Google a competitive advantage.

In 2024, if inflation declines and the economy achieves a soft landing, the advertising business is expected to further recover. Although Google's high base may limit growth, a potential major restructuring of the advertising department could further improve profit margins.

In addition, investors are more looking forward to the progress of AI business. After launching the Gemini large model, it is expected to be further promoted outside its own system, and the competitiveness of its cloud services is also expected to improve. The growth rate of Google's AI business compared to Microsoft and Amazon in cloud business may be an important indicator for investors to consider "which company has a brighter future in AI."

The current P/E ratio is 25.66 times, and the corresponding forward P/E ratio for the average expectation for the next two years is 19.6 times.

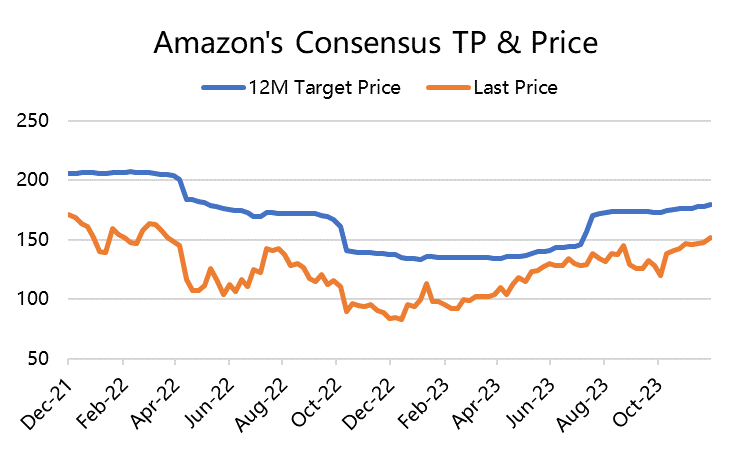

Amazon

Bloomberg consensus expectations: The revenue for 2024 is expected to be $636.893 billion, with a year-on-year growth rate of 11.03%; EBIT profit growth rate is 44.29%, and the profit margin has risen to 7.15%, both reaching new highs. The target price is expected to be $179.69, with some room for growth from the current price.

After a year of inflation, the retail business is expected to continue its recovery in 2024. However, Amazon's e-commerce business is currently facing two major challenges:

1. Market share challenges from low-cost e-commerce platforms such as Temu and Tik Tok Shop.

2. The excess savings accumulated by U.S. residents during COVID-19 may be depleted.

Of course, Amazon's logistics system may become its most important competitive advantage. On the other hand, AWS has achieved stable growth with the largest market share and has made significant progress in AI applications in the future. In addition, the incremental growth shown in the advertising business in the past few quarters will greatly increase its profits.

The market expects a profit forecast for 2025 to be 33 times, which is more reasonable relative to the current valuation, provided that the profit normalizes.

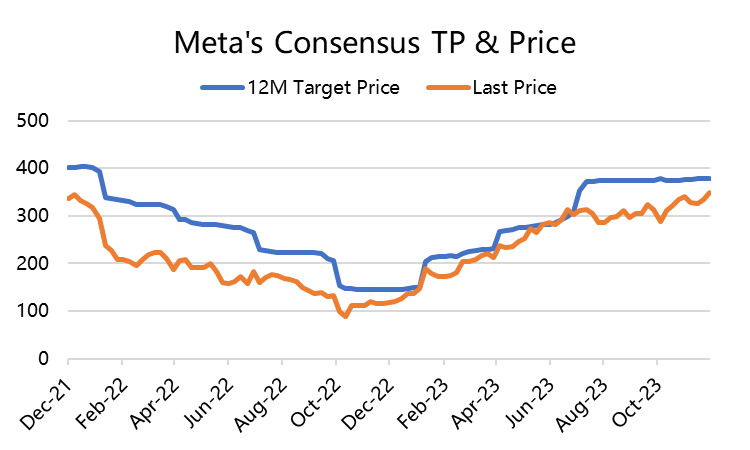

META

Bloomberg consensus expectations: The revenue for 2024 is expected to be $151.22 billion, with a year-on-year growth rate of 14.8%; EBIT profit growth rate is 23.53%, and the profit margin has risen to 36.11%, both reaching new highs. EPS is 17.52, with a growth rate of 21.83%.

The target price is expected to be $379.24, with some room for growth from the current $365.93.

Meta's social media matrix is already unshakable, and in 2023, faced with strong competition from Tik Tok, its own short video platform Reels has developed rapidly. Compared to live streaming e-commerce, social media in the United States is more focused on advertising efficiency, so, like Google, the undervalued part of the advertising business has been restored in the first half of the year.

With the expectation of a soft landing in 2024, the outlook for the advertising business remains positive. In addition, although the growth of Threads is slow, it may also become another source of advertising revenue after the overflow of X (formerly Twitter) users, further increasing the company's advertising revenue.

The VR headset is still there, and the initial "metaverse" hype, which was criticized by investors mainly because it was difficult to achieve in the short term, is now not emphasized by Meta itself, but is constantly being iterated on in terms of products. Although the Quest 3 in 2024 will face competition from Apple's Vision Pro, it may also gain overall incremental growth due to industry exposure once again.

Meta's biggest advantage is its strong asset quality, and its cash reserves and strong cash flow are enough to support its continuously "slow bull" valuation. Based on the expected EPS for 2024, Meta trades at a P/E ratio of about 19 times. If its future EPS growth remains in the range of 15-20% or higher for the next few years, it may support its stock price breaking through $500.

The Big-Tech Portfolio

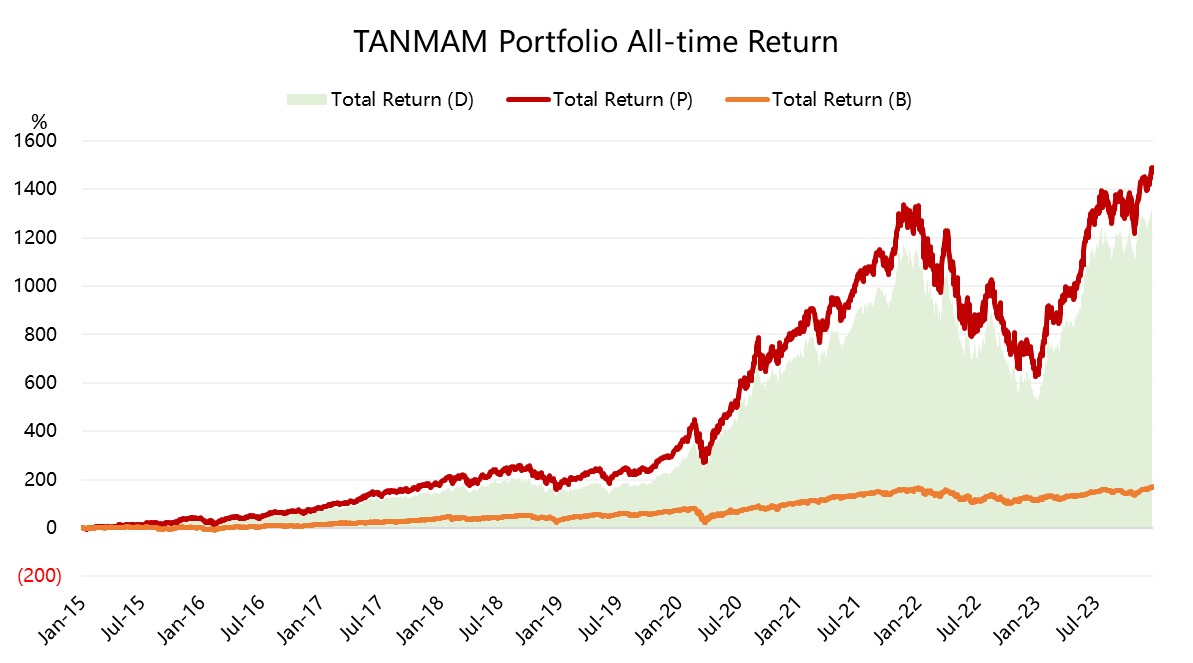

We will combine the seven companies with the highest weight into an investment portfolio called the "TANMAM" portfolio. By the end of the year, the excess return of the big tech portfolio reached a new high.

By backtesting this portfolio using an equally weighted, quarterly rebalanced approach, the performance since 2015 has far exceeded the S&P 500, with a total return of 1489.9%, setting a historic high. Meanwhile, the $SPDR S&P 500 ETF Trust(SPY)$ achieved a return of 170.51% during the same period, reaching a new annual high.

The year-to-date return is at 110%, which is higher than SPY's 25.5%. The Sharpe ratio is 4.4, compared to SPY's 1.7 during the same period.

The weekly return for the portfolio is 2.9%, while SPY's return is 0.6%.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.

Great ariticle, would you like to share it?