Where Is the Stock Market Headed after Red Sea War Breaking Out?

I. Review of Market

1. Performance of US stock index futures

Since December, the market is worried about over-pricing of the US Treasury yields, superimposed non-agricultural employment data exceeding expectations, inflation remains resilient, superimposed hawkish remarks of the Federal Reserve, and the yield of 10-year US bonds has rebounded.

As the market gradually correction its expectations until the Federal Reserve starts to cut interest rates in mid-2024, the marginal impact of negative interest rate will weaken after the revision of interest rate cut expectations, and market sentiment will gradually repair. The three major indexes will fluctuate and rebound, maintaining a high range of volatility, the US Dollar Index will fluctuate and rebound.

fundamental analysis

(1) The Red Sea crisis supported energy prices, the CPI of the United States exceeded expectations in December, and inflation resilience suppressed doves' sentiment.

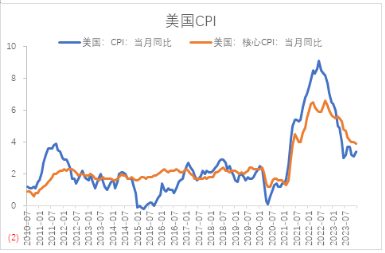

On January 11, Eastern Time, data released by the US Department of Labor showed that the annual rate of CPI in December was 3.4%, the previous value was 3.1%, and it is expected to be 3.2%; After the December quarter adjustment in the United States, the monthly CPI rate recorded 0.3%, the previous value was 0.1%, and it is expected to be 0.2%; In December, the core CPI of the United States recorded an annual rate of 3.9%, compared with the previous value of 4% and the expected 3.8%.

US CPI exceeded market expectations in December, showing resilience. From the year-on-year On the whole, the inflation in the United States exceeded expectations in December mainly due to the increase in energy prices and transportation costs, and other inflation prices also showed strong resilience.

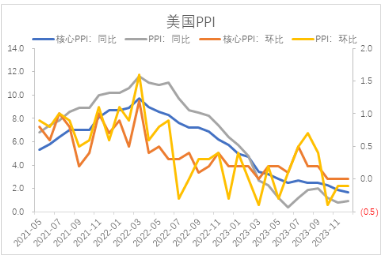

The data released on January 12 showed that the PPI of the United States in December increased by 1% year-on-year, the previous value was 0.8%, and it is expected to be 1.3%; In December, the PPI of the United States decreased by 0.1% month-on-month, the previous value decreased by 0.1%, and it is expected to increase by 0.1%.

Figure 1: US CPI in December

Source: Wind International Derivatives Think Tank

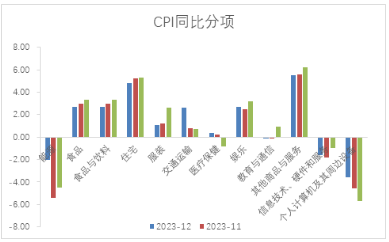

Figure 2: CPI breakdown data of the United States in December

Figure 3: PPI in December in the United States

(2) The number of jobless claims in the United States at the beginning of the week exceeded market expectations, and the job market was resilient.

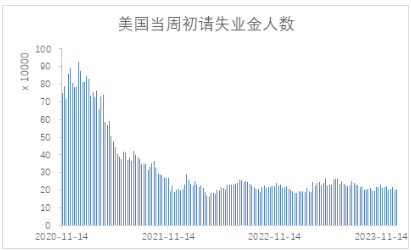

According to the data released on January 11th, the number of jobless claims in the United States recorded 202,000 at the beginning of the week from January 6th, with the previous value of 203,000 and the expected number of jobless claims in the United States exceeding market expectations, indicating that the job market is resilient.

Since November, the number of people claiming unemployment benefits at the beginning of the week has continued to decline. As the impact of auto workers' strikes weakened, workers returned to their posts and the job market was under pressure. At the same time, the labor participation rate declined in December, and the average hourly wage rebounded year-on-year, slightly exceeding expectations month-on-month.

The wage growth rate was repeated, and inflation resilience appeared, which put pressure on the Federal Reserve. Although the manufacturing demand is weak and the consumer industry is gradually slowing down, employment and inflation are more resilient than market expectations, and the probability of a soft landing of the US economy is higher.

Figure 4: Number of jobless claims in the United States at the beginning of the week

Source: Wind International Derivatives Think Tank

At present, the impact of the Red Sea crisis on the energy supply side may last for some time, and it is more likely that crude oil prices will remain volatile. At the same time, the US service industry has not yet fallen into the shrinking range, and the inflation level in the United States is likely to be repeated, which further suppresses the dovish sentiment in the market.

In view of repeated inflation and employment resilience, in order to avoid the risk of secondary inflation, the need for the Federal Reserve to cut interest rates urgently has declined, and it is more likely that the Federal Reserve will maintain a wait-and-see in the first half of the year.

III. Position analysis

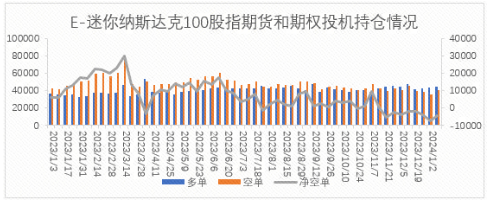

According to data released by the US Commodity Futures Trading Commission (CFTC), as of the week of January 9, the net long positions of speculative positions in E-mini S&P 500 stock index futures and options increased from 77,739 lots to 93,438 ,

From the perspective of positions, the speculative positions of mini Nasdaq index futures, mini S&P 500 index futures and small Dow futures increased by 5,906, 2,167 and 608 respectively;

Figure 5: Changes in speculative positions of E-mini Nasdaq 100 futures options

Source: CFTC official website International Derivatives Think Tank

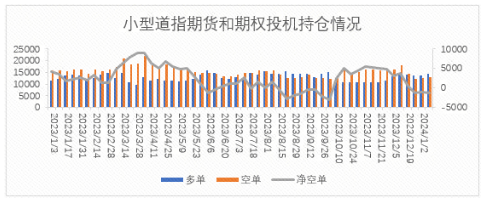

Figure 6: Changes in speculative positions of Dow Jones ($5) futures options

Source: CFTC official website International Derivatives Intelligence

V. Market Outlook

In the first half of 2024, the Fed has a high probability of maintaining wait-and-see and higher interest rates. The driving force of the decline in denominator interest rates has weakened in the short term, and the downward pressure on the numerator economy is approaching.

From the market perspective, the position data shows that since January, the speculative multi-orders of mini S&P and Dow have increased, the short strength of mini Nasdaq index has slightly increased, and the speculative positions of the three mini index futures have diverged.

On the whole, the pressure of fundamental decline and the test of expected revision of interest rate cut have been gradually priced by the market, and there is limited room for continuous correction of US stocks. In the medium and long term, the downward trend of interest rates is basically determined, which supports US stocks. Under the short-term situation of long and short interweaving, it is expected that US stocks may continue the pattern of high range volatility, and it is suggested to deal with it with the range thinking of high throwing and low sucking.

$NQ100 Index Main Connection 2403 (NQmain) $$SP500 Index Main Connection 2403 (ESmain) $$Dow Jones Main Link 2403 (YMmain) $$Gold Main Connection 2402 (GCmain) $$WTI Crude Oil Main Line 2402 (CLmain) $

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.

- DominicBeck·01-24🙌 Amazing insights!LikeReport

- ChrisColeman·01-24Hold on tight, rollercoaster ride! 🎢LikeReport

- Bastian1928·01-18hahshsjjsauaLikeReport