Is the big Commodities bull market coming? Why is oil lagging behind?

In May, against the background of the rising prices of non-ferrous metals and precious metals, international crude oil prices did not follow suit, but continued to fall from the high point set in April.

At a time when global monetary policy is about to enter an inflection point of easing, U.S. inflation is resilient, China's economy is recovering moderately, and crude oil is in the same macro environment as other rising industrial products. Why hasn't it risen sharply?

The macro environment is favorable for commodities

In overseas markets, the expectations of central banks turning to easing are very strong, especially the decline in inflation in the United States, which has stimulated the Fed's interest rate cut expectations to heat up again.

The United States released inflation data for April. Whether it is CPI or core CPI, whether it is year-on-year or month-on-month, they have all dropped from the previous value. As the leading economic indicators of the American Conference Board fell by 0.6% month-on-month in April, weaker than expected and the previous value fell by 0.3%, the swap market raised its expectations for the Fed's rate cut within the year. By the September Fed meeting, the probability of cutting interest rates by 25 basis points More than 80%.

The decline in US dollar interest rates is conducive to the rise of commodities. As of May 20, the 2-year U.S. Treasury yield, which is sensitive to monetary policy, fell to 4.82%. It had previously climbed to 4.98% on April 18, the highest record for the year, and it was 3.89% in the same period last year; The 10-year U.S. Treasury yield, which reflects the outlook for U.S. economic growth, fell to 4.44%, after hitting a record high of 4.7% on April 25 and 3.38% in the same period last year.

Crude oil supply contraction less than expected

From the perspective of supply, the Palestine-Israel conflict has little impact on crude oil supply, far less than the contraction effect brought about by the "Russia-Ukraine conflict". In 2024, global oil supply is expected to increase by 580,000 barrels per day to a record 1.027 million barrels per day, with non-OPEC production increasing by 14,000 barrels per day and OPEC production falling by 840,000 barrels per day.

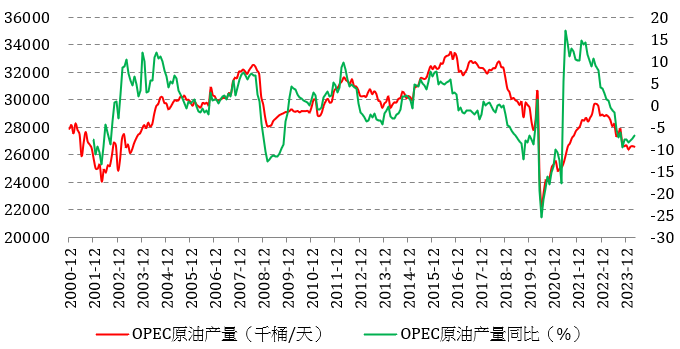

The survey results show that OPEC's crude oil production fell only moderately in April, and the production of some members such as Iraq is still higher than the level stipulated in the production reduction agreement at the beginning of this year, indicating that the implementation of production cuts is still not good. Production increased slightly in Libya and Iraq, while decreased in Iran and Nigeria. Compared with the previous oil production reduction agreements reached, the oil production of Iraq and the United Arab Emirates is still hundreds of thousands of barrels per day higher.

The picture shows the monthly output and growth rate of OPEC crude oil

Russia's crude oil production in April showed that it had not met its quota for production cuts. In April, Russia pledged to cut crude oil production by 350,000 barrels from March in order to reach its target of 9.099 million barrels per day. However, in fact, Russia's crude oil in April was still as high as 9.418 million barrels per day, which was only 219,000 barrels per day lower than in March.

Benefiting from the increase in production, U.S. crude oil exports have increased significantly. The biggest beneficiaries of European and American sanctions against Russia are U.S. oil producers. U.S. crude oil exports hit a record high in 2023, averaging 4.1 million barrels per day, 13% higher than the annual record set in 2022, or an increase of 482,000 barrels per day.

Crude oil demand growth is sluggish

The latest monthly report from the International Energy Agency (IEA) shows that the outlook for global oil demand growth continues to be weak this year due to a slowing economy and a mild climate in Europe.

From the perspective of refinery operating rate, the operating rate of European refineries rose to 81.6% in April, higher than the 80.8% in the same period last year, indicating that the demand for crude oil is slightly better than the same period last year, but lower than that in January-February this year; The operating rate of U.S. refineries rose to 88.6%, but lower than the 90.6% in the same period last year, indicating that U.S. crude oil demand was weaker than the same period last year.

As of May 10, the average daily demand for gasoline in the United States was 8.678 million barrels, a decrease of 4.5% from the same period last year. The demand for gasoline in the United States before the peak summer consumption season was lower than expected.

The growth of China's crude oil demand is relatively moderate. From January to April, crude oil imports increased by only 2% year-on-year, far lower than the 4.6% in the same period last year. In April, China's crude oil imports increased by 5.9% year-on-year, changing the negative growth momentum in March. However, rising fuel prices for transportation may curb crude oil consumption.

To sum up, in 2024, with loose overseas liquidity and accelerated domestic economic recovery, commodities may usher in a wave of bull market, especially mineral metals whose capital expenditures continue to decrease, such as copper, hit new highs due to supply shocks. As the blood of the global economy-crude oil presents different supply and demand patterns, and it is unlikely that the supply will be further compressed. OPEC's production cuts will fall short of expectations; In the short term, demand is facing the impact of economic slowdown in Europe and the United States and consumption substitution brought about by the development of China's new energy industry. Therefore, there is a high probability that crude oil prices will be the last product to rise, that is, destocking needs to be completed.

$NQ100 Index Main 2406 (NQmain) $'$Micro SP500 Index Main 2406 (MESmain) $$SP500 Index Main 2406 (ESmain) $$Dow Jones Main 2406 (YMmain) $$Gold Main Company 2406 (GCmain) $$WTI Crude Oil Main Company 2407 (CLmain) $

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.