Earnings Season Landmines - Option Buyers Gutted!

While examples of trading losses from mistimed earnings bets abound, today I'll highlight a situation that was an absolute disaster for option buyers - one better avoided when possible.

On the flip side, it was a windfall for option sellers who essentially stumbled upon free money.

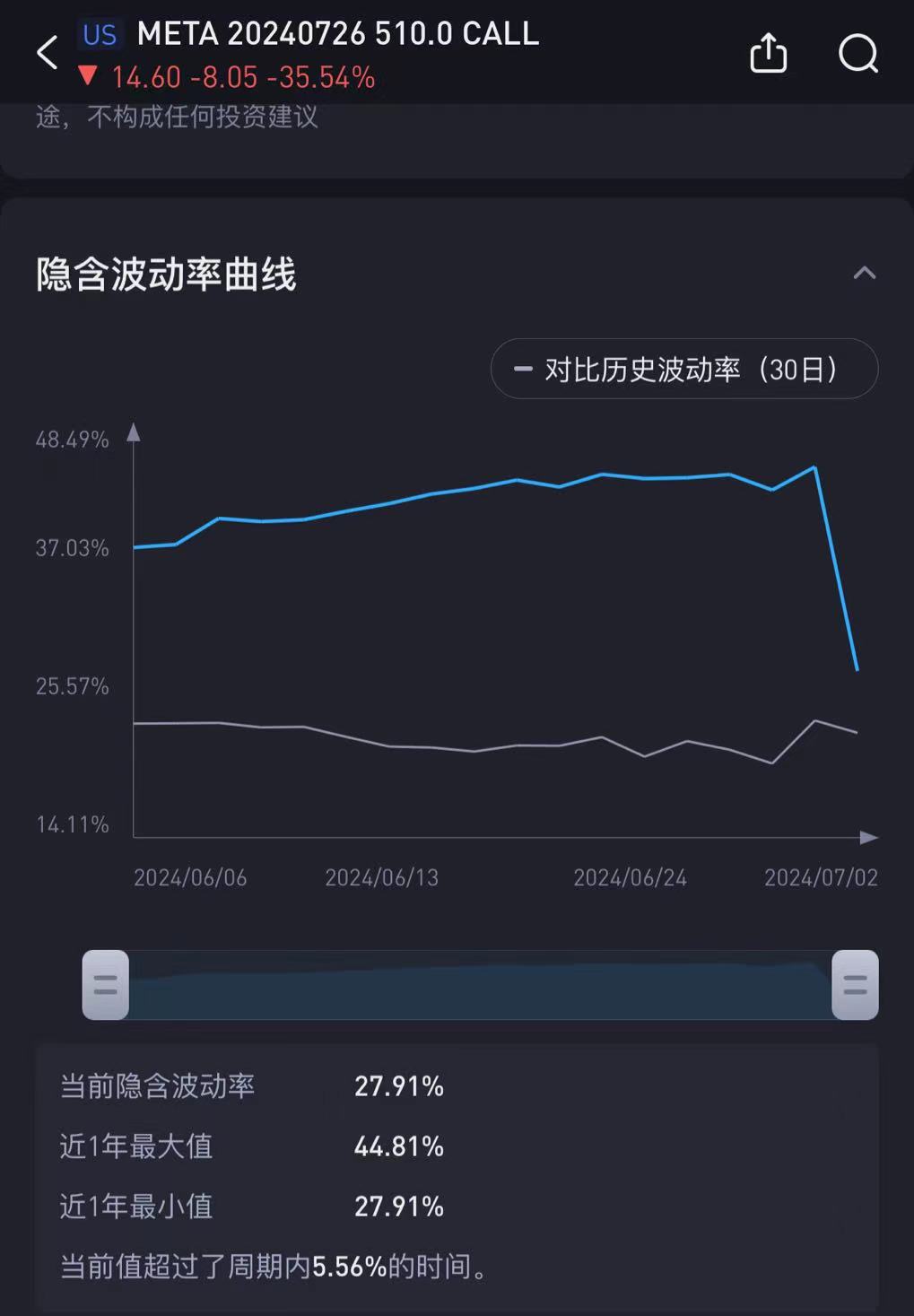

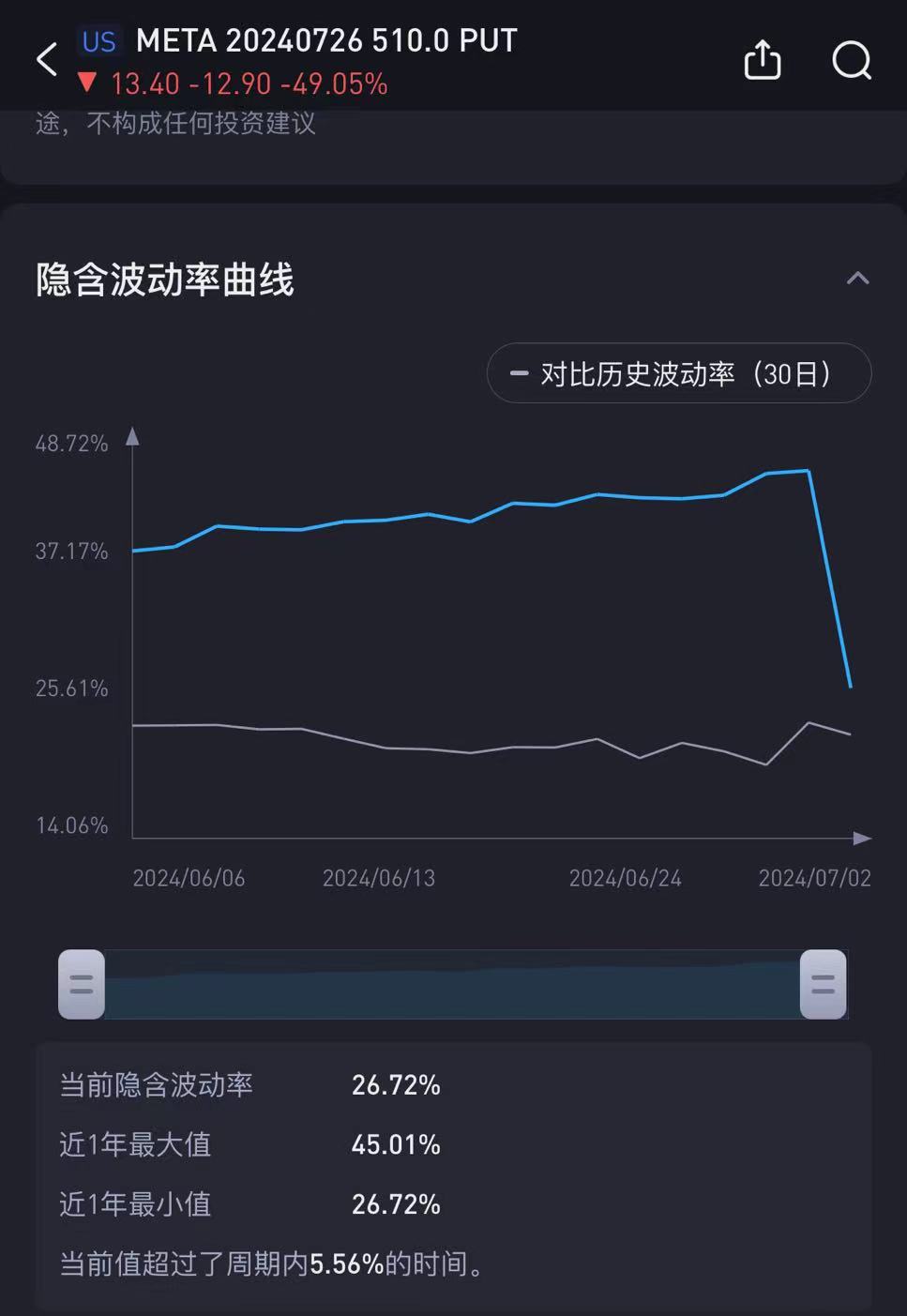

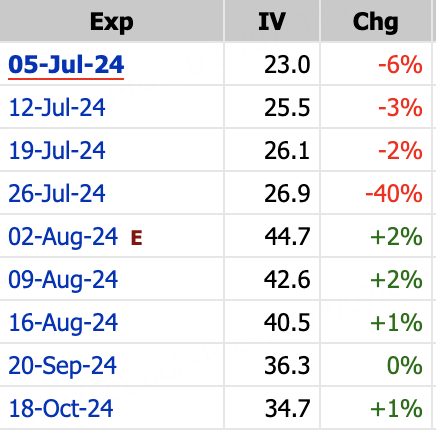

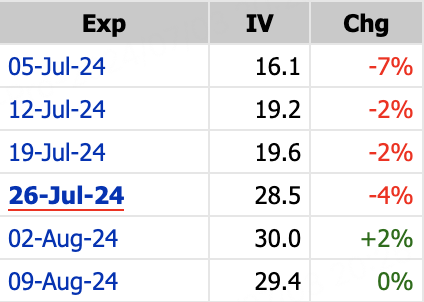

On July 3rd, $Meta Platforms, Inc.(META)$ pre-announced their earnings release date of July 31st after the close. Upon this news, all META options for the current July 26th weekly expiration, both calls and puts, crashed around 40%.

How did the other expirations fare?

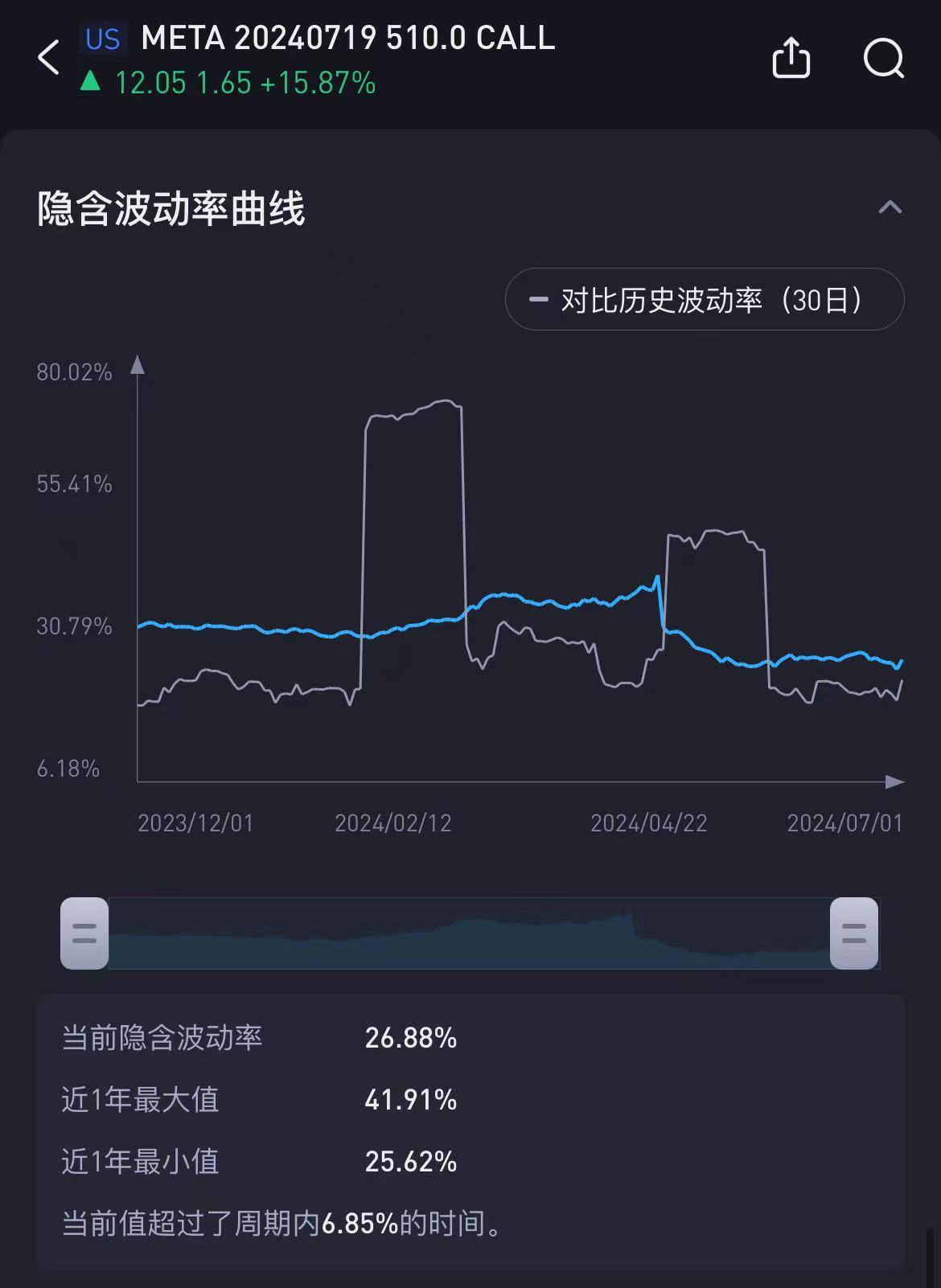

On that day, META opened low but rallied, closing up 0.96%. The July 29th weekly at-the-money calls were up 15.87%, while puts were down 21.15%.

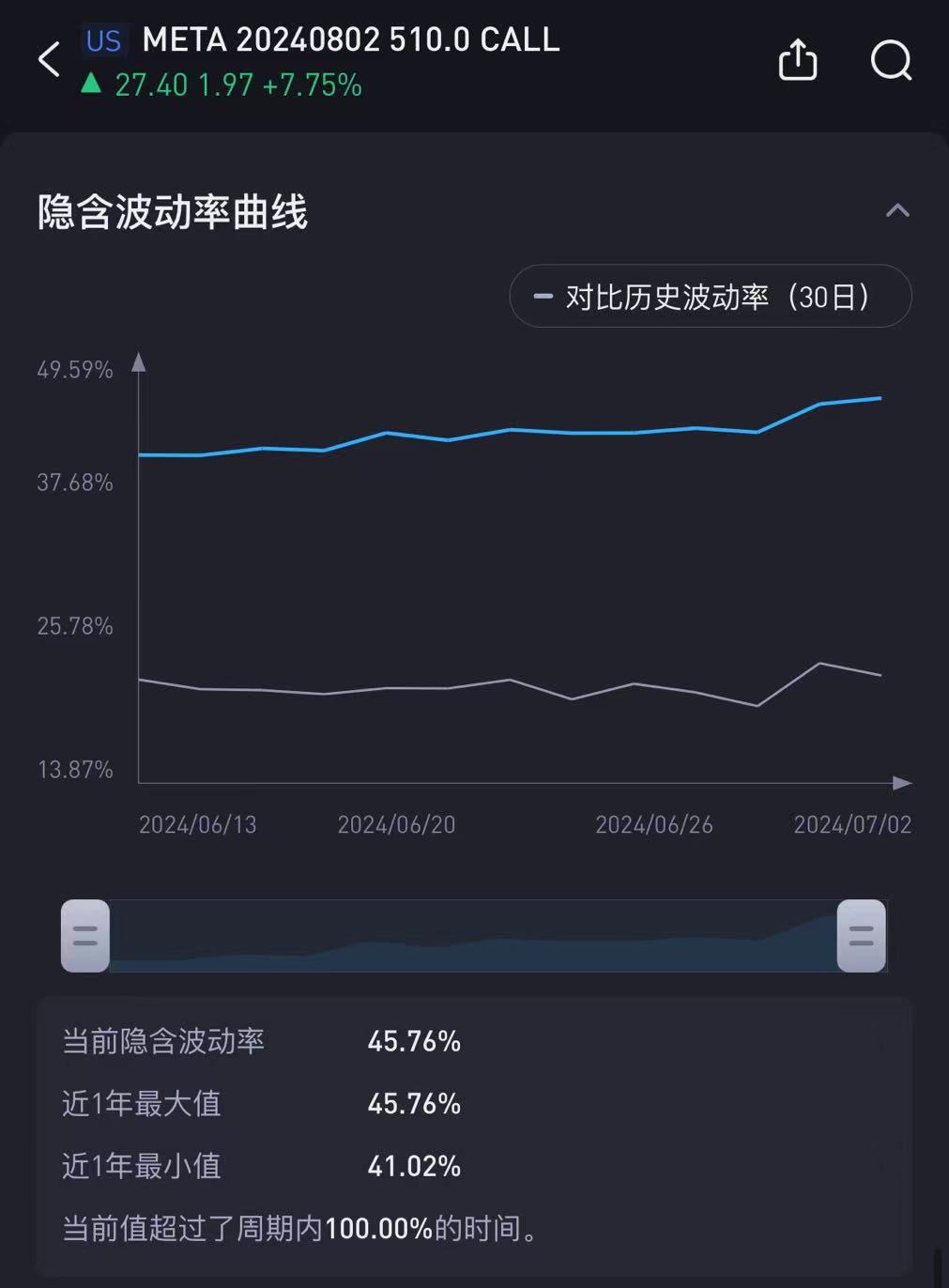

The August 2nd 510 calls gained 7.75%, puts lost 10%.

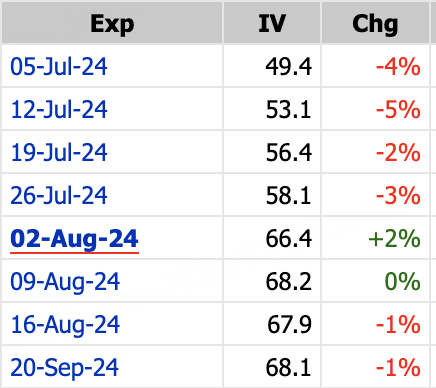

What was the culprit? Checking the July 26th weekly option implied volatilities (IV), both calls and puts saw their IVs cut in half from around 44% down to 27% compared to the prior day:

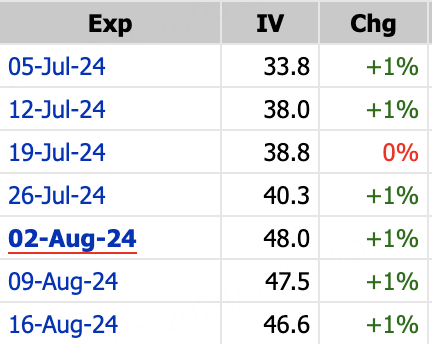

In contrast, the August 2nd earnings week IV held steady at 45.7%:

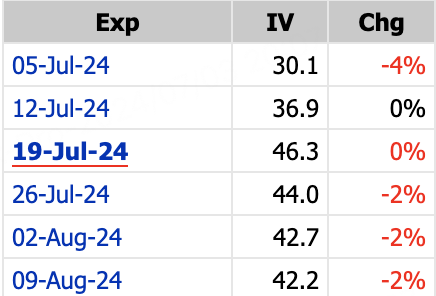

And July 19th weekly IVs had been sitting steadily around 27%:

The conclusion is that the earnings date release triggered an IV crash specifically for the July 26th weekly options, with IVs getting cut in half - tanking prices for both calls and puts.

META has historically reported in late July, so seasoned traders likely recall many tech giants reporting around July 25th/26th. Any traders looking to position early saw market makers pre-emptively jack up those weekly IVs - taking that edge away.

The evidence is in the option chain IVs, with expirations after the earnings release maintaining elevated IVs. Only the September 20th expiration saw IVs start to drift below 40%.

This likely has you wondering - are there other stocks at risk of a similar IV crash event?

Tech Stock Volatility Review

Ever the diligent one, I surveyed the IVs across MSFT, NVDA, AAPL, TSLA, COIN, AMD, TSM, AMZN, GOOG, and NFLX to assess potential opportunities.

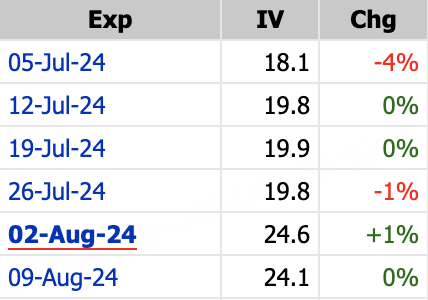

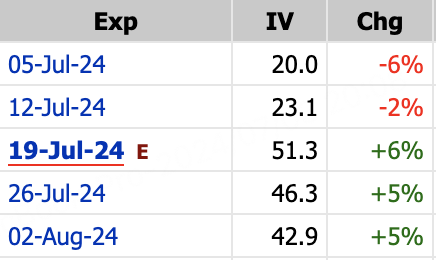

First up, Microsoft hasn't announced their earnings date yet. The July 19th options show 15% IVs, while July 26th is at 22% - so markets are currently pricing in an earnings release that week.

Don't be fooled by the low IVs. I calculated that an IV crush on the puts could mean a $3 drop in pricing - quite significant.

Nvidia is expected to report later, likely after August 16th. Without any August 31st listed yet, the September 51.8% IVs are running about 6 points higher than the 45% August averages.

If stock prices remain rangebound, overall IVs could drift lower still.

For Apple, markets are pricing in an August 2nd earnings week, with 24.6% IVs running about 5 points above prior weeks.

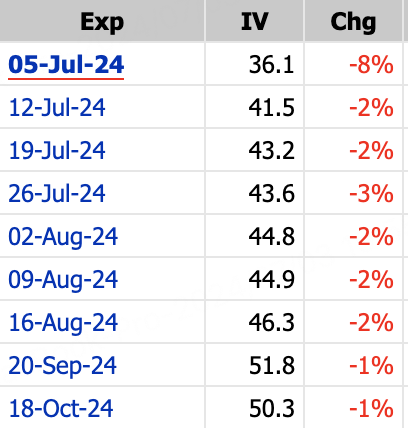

Tesla has pre-announced July 23rd, and July 26th weeklies are sporting 60% IVs, a massive 12.1 point premium to prior weeks.

Intriguingly, despite a 10% gap up overnight, front week IVs have still compressed compared to the post-earnings expirations holding volatility premia.

Coinbase is expected around the August 2nd week, with an 8 point IV differential.

AMD is projected for the August 2nd week as well, also carrying an 8 point IV skew.

For TSM, markets are pricing in the July 19th week, with a 10 point spike in IVs.

Attentive readers may have noticed the semis space like TSM and Nvidia had seen volatilities come in from the prior frenzy.

Google's earnings seem to be priced into the July 26th week, with a 9 point IV gap.

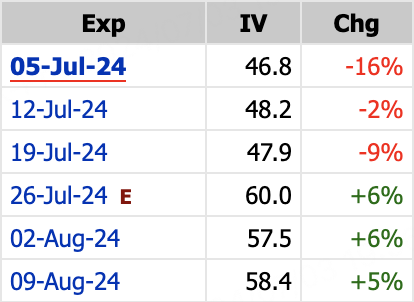

Finally, for Netflix which pre-released their July 18th earnings date, the IV difference is quite stark at a 28 point premium to the prior week.

Why are META and NFLX being treated so distinctly? Consider their drastic stock reactions to last quarter's results for a hint.

In summary:

Earnings releases tend to drive volatility, so option IVs into that event week often see premiums.

The magnitude of that IV skew reflects historical price reactions. High beta movers like NFLX and META carry wider IV differentials.

Traders can't arb the elevated IVs by trading a month out. Earnings volatility gets priced in early.

If markets are caught wrongfooted on the earnings date, mistimed options see debilitating IV crashes - a nightmare for buyers.

Option buyers looking to play upside into earnings should consider expirations after the release to avoid IV crush risk and benefit from elevated volatility premia.

For bullish option sellers into earnings, selling front week or earlier expirations can be fruitful plays as IVs bleed off, with the added chance of cashing in on an IV crush windfallif markets re-price the earnings date expectation.

There are always exceptions like the semis volatility retracement. But given current tech trends, many names seem ripe for selling pre-earnings upside via put sales.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.