Small Business SOS: Is the US Job Market at a Tipping Point?

The U.S. labor market is at a critical inflection point, a change that will not only affect economic trends, but will also have a profound impact on monetary policy and asset pricing.

Labor market status: clear signs of inflection point

Latest data reflect cooling labor market

Nonfarm payrolls increased by 206,000 in June, higher than the expected 190,000

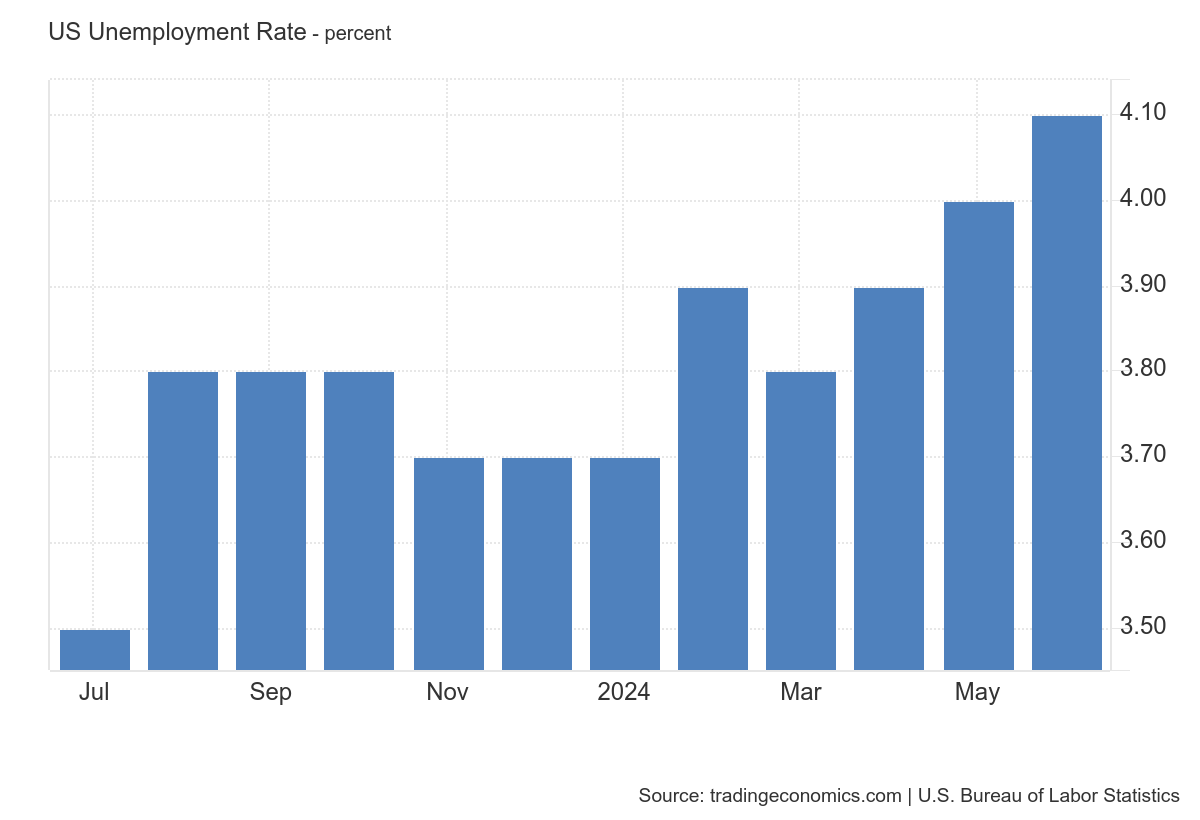

The unemployment rate rose from 4.0% to 4.1%, higher than market expectations of 4.0

Average hourly earnings rose by 3.9% year-on-year, with the rate of growth continuing to slow down

This data is somewhat contradictory. The job market is relatively strong but the unemployment rate is rising, although lower market expectations amid weaker-than-expected employment data in April and May are also key factors and therefore add to the signs of a cooling U.S. labor market.

On the other hand, the supply-demand imbalance is improving

Labor supply has basically recovered to the pre-epidemic trend line

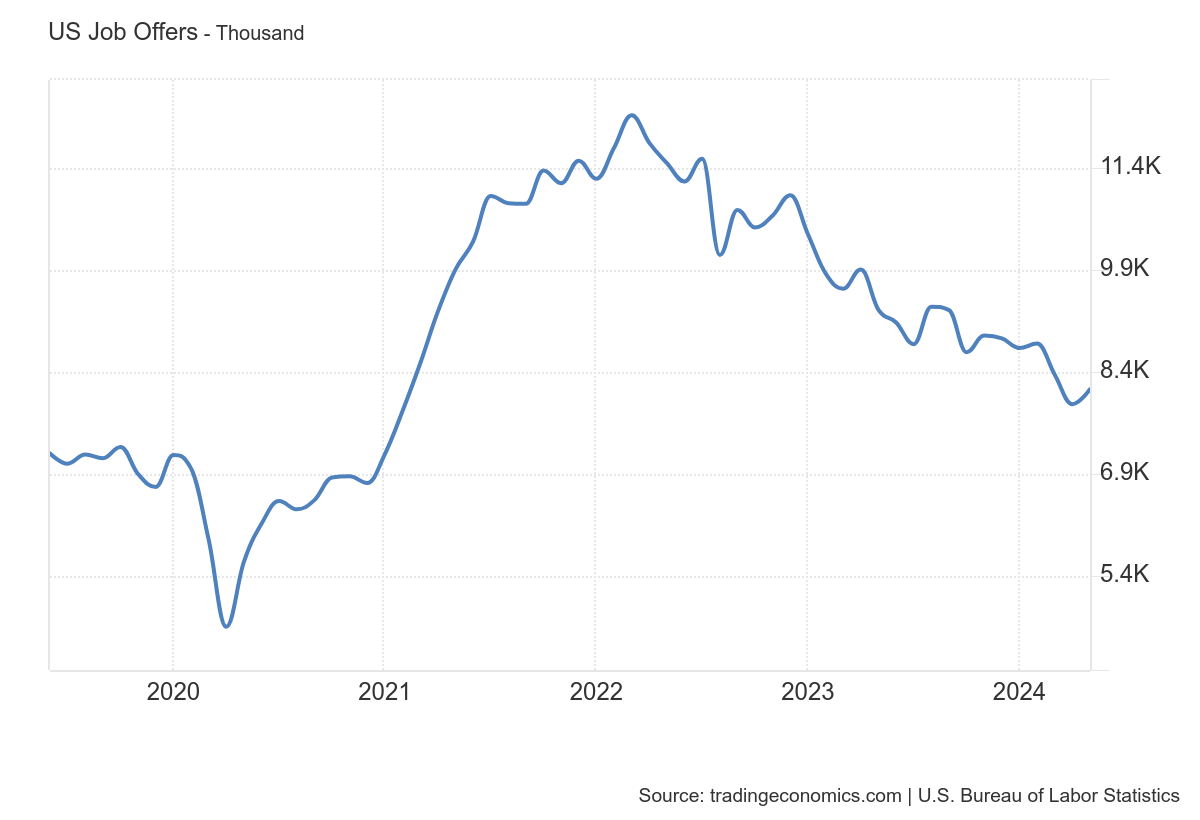

Aggregate labor demand has peaked and declined, and the gap between supply and demand has narrowed significantly

Both the separation rate and the job vacancy rate have fallen back to pre-pandemic levels

As a result, market expectations for a Fed rate cut have risen again

The ChiNext FedWatch tool shows that the likelihood of a 25 basis point rate cut in September has increased from 66.5% to 71.1%, the likelihood of the first rate cut in November has also risen, and the likelihood of a second rate cut in December has risen to 46.5%, with investors fully expecting two Fed rate cuts by the end of the year.

Small Businesses and Interest Rate Sensitive Industries: Key Factors in the Cooling Economy

Small Businesses Under Pressure

Small businesses with fewer than 50 employees account for 43 percent of total U.S. hiring, and small business hiring gains have largely stalled recently

Micro-businesses with less than 10 employees have lost 500,000 jobs this year

Small businesses are more reliant on bank loans to finance their operations, and over the past year, interest rates on small business loans have remained in the 9%-10% range, tied to the policy rate, and this high interest rate environment has put greater pressure on small business operations.

Looking at current economic indicators: small businesses' willingness to hire is trending lower and willingness to add inventory is slipping, in tandem with the decline in manufacturing new orders

Interest rate-sensitive industries lead job market cooling

White-collar, high-paying industries such as finance, law, and technology have seen a sharp turnaround in hiring fervor, accounting for about 22% of total nonfarm payroll employment

Catering, entertainment and other basic services and healthcare industries are relatively resilient, although the medical industry has high skill entry barriers, cross-industry mobility is difficult, and the main changes remain in catering and entertainment

The relative resilience of the service and healthcare industries is difficult to fully hedge against the employment depression in the financial/legal/technology industries.

The increased likelihood of a Fed rate cut is demonstrated by

There will be a shift to focus on employment rather than inflation

Separation rate, job openings have fallen back to pre-epidemic levels

If the decline continues, it could be accompanied by an increase in the unemployment rate

Preventing a further slowdown in the job market triggers non-linear changes, and in the context of the election, monetary policy faces uncertainty

The bottom line of the U.S. economic resilience has not faded. Preventive "shallow interest rate cuts" may be initiated during the year or even before the election. The recent restart of broad fiscal is expected to continue to support the resilience of demand, and fiscal policy may be in line with monetary policy, together to support the economy

Asset Allocation

Pro-cyclical sectors Interest rate cuts + fiscal re-enforcement are expected to bring allocation opportunities in raw materials, real estate, consumer durables and other sectors $Energy Select Sector SPDR Fund(XLE)$ $Real Estate Select Sector SPDR Fund(XLRE)$ $Materials Select Sector SPDR Fund(XLB)$ $Technology Select Sector SPDR Fund(XLK)$

U.S. bonds 10-year interest rates may fluctuate in the range of 4.2%-4.4% $iShares 20+ Year Treasury Bond ETF(TLT)$ $US20Y(US20Y.BOND)$ $US10Y(US10Y.BOND)$

$S&P 500(.SPX)$ $SPDR S&P 500 ETF Trust(SPY)$ $Invesco QQQ(QQQ)$ $NASDAQ(.IXIC)$

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.

- NinaEmmie·07-08Great analysisLikeReport