Whether a 50bps or 25bps rate hike, it's immaterial for Nvidia's near-term trading.

A bold claim: Nvidia's trading dynamics will remain essentially unchanged after the September FOMC decision, be it a 25bps or 50bps rate hike.

Coming out of the Mid-Autumn Festival break, rate hike expectations abruptly shifted, with 50bps becoming the higher probability scenario over 25bps. Historically, a 50bps hike was viewed as a negative catalyst that could drive Nvidia down towards $90.

But the options market seems to disagree this time around.

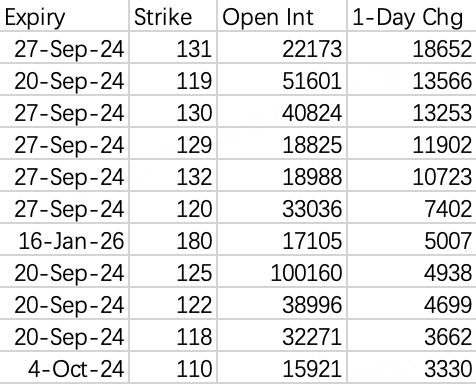

Looking at the three trading days since last Friday, including Monday and Tuesday this week, there haven't been any glaring shifts in Nvidia's open interest profiles that would align with a hawkish 50bps re-pricing.

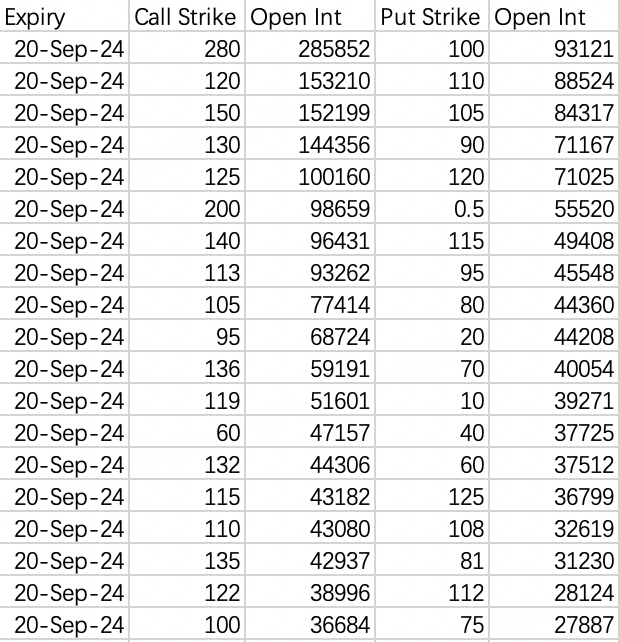

As the chart shows, this week's call open interest remains firmly elevated, with $120 strikes leading after stripping out a few outliers. In fact, the $125 strikes have seen a notable increase in open interest too - the complete opposite of what a bearish repricing would imply.

On the put side, $100 and $110 strikes comprise the largest open interest, with little change in the $90-95 area. This suggests the market is pricing in little chance of a move below $100.

Thus, the expected trading range remains $110-120 for this week's expiration, or at the extreme ends, perhaps $100-130. Still very much a rangebound, consolidating profile.

Additionally, yesterday's call option volume showed heavy selling in the $NVDA 20240927 131.0 CALL$ for next Friday's expiration. Such aggressive call selling at higher strikes implies the rate decision magnitude holds little significance.

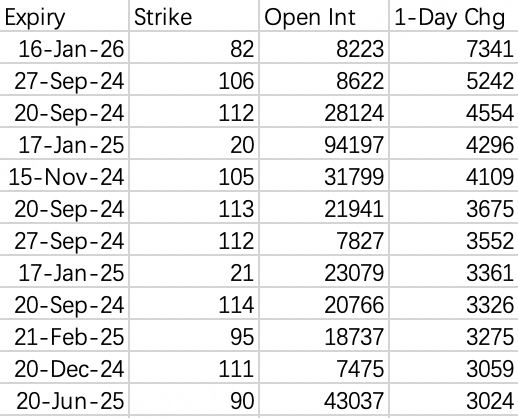

More interesting is the new out-of-the-money put buying we've seen, particularly some of the later-dated contracts like $80-90$ strikes expiring after 2024.

But upon closer inspection, these appear to be more risk-reversal or leverage enhancement strategies rather than outright bearish bets:

Selling $NVDA 20260116 82.0 PUT$

Buying $NVDA 20260116 180.0 CALL$

This lazy approach simply uses the put sale to offset potential losses on the upside call purchase. Rolling the put sale weekly could offer a higher probability levered bullish strategy over time.

We see a similar structure in:

Selling $NVDA 20250117 100.0 PUT$

Buying $NVDA 20250117 145.0 CALL$

Of course, there are still some more defensive call buyers too, like the $NVDA 20241220 100.0 CALL$ purchased on 8/22 for around $13.40 which has already gained 50% in just a few days. That said, unhedged leverage in this environment can certainly be psychologically challenging.

It makes sense for Nvidia to shrug off rate concerns - a recession arguably benefits companies driving productive technological disruption like AI, as capital scrambles to align with the new frontiers of economic output.

In summary, whether we get a 25bps or 50bps rate hike in September is largely immaterial for Nvidia's $100-130 trading range. Option sellers can continue business as usual for now.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.