A commentary on FOMC day option flows

DLTR: Smart institutions know to avoid controversy in an election year.

Wednesday's opening flows are difficult to decipher, as shown in the chart - there's essentially only one trade type: stock + $NVDA 20241220 120.0 CALL$ + $NVDA 20241220 120.0 PUT$ across all expirations. For example:

Stock

$NVDA 20241220 120.0 CALL$

$NVDA 20241220 120.0 PUT$

We also saw stock + October straddles, November straddles, January straddles, February straddles, March straddles, and June straddles.

The December flows show as sell put + buy call, but could actually be buy put + buy call.

While the traded prices skew towards the offer side, the $NVDA 20241220 120.0 PUT$ had just a $0.10 bid/ask spread, implying a traded range of $14.30-14.40. The massive size likely swept the entire bid stack, causing the $14.35 print to be labeled as buyer-initiated when it may have been seller-initiated.

Unclear flows require multiple data points for confirmation, as I've mentioned before.

If we assume December was a straddle purchase, is it possible the other expirations were straddles too? In theory, these were likely from the same institutional buyer, so the strategy should be consistent.

However, Wednesday's option volumes only showed significant opening interest in the December expiry. The other months had muted volumes or unclear direction.

So there's also a possibility that some of the other expirations were simply closing trades.

Discussing all possibilities, let's first examine the most straightforward interpretation of this strategy.

If we assume they were buying monthly straddles, the institution is essentially hedging their stock position out to June 2023 through long volatility plays.

There are issues with this simplistic view, so it may be best to continue monitoring for now. The intended strategy could become clearer in 3 months' time.

By the way, I had expected them to roll their $113 covered calls yesterday given Nvidia's drop - a ruthless move if it held $113. But surprisingly, they didn't roll.

No major flows, just continuing to monitor the $240 resistance level as before.

No notable opening trades, but there was a sizable $AAPL 20241018 250.0 CALL$ covered call closure that stood out.

This $250 call was sold on 8/22 for $1.20 - theoretically they could have held until expiration, so why close it out over a month early? Perhaps worried about it getting called away on an upswing?

Scanning other data sources, I noticed an explosive SPY flow hitting just before 11:52am ET yesterday, right ahead of the FOMC statement:

Buying $SPY 20251219 700.0 CALL$ for $3m (10,000 contracts)

Buying $SPY 20251219 740.0 CALL$ for $2.9m (24,000 contracts)

Direction is unclear as both strikes traded closer to the offer side. But in the context of such aggressive strike prices, direction matters less.

Even if those were sell calls, the $700 strike implies massively bullish upside for the S&P 500 by late 2025.

However, given the unequal sizing between the two calls, it's more likely a bull $700 call vs bear $740 call spread. Highly speculative though, craftily structured as a full hedge with no upfront debit.

We saw a similar QQQ flow mirroring Nvidia's Dec $470 straddle:

$QQQ 20241220 470.0 CALL$

$QQQ 20241220 470.0 PUT$

I'd interpret this as likely a parallel hedging strategy to Nvidia's.

$20+ Year Treasury Bond ETF (TLT)$

Theoretically, rate cuts should favor put selling in bond funds like TLT. But interestingly, we saw call selling instead:

Closing $TLT 20250117 105.0 CALL$

Rolling out and selling $TLT 20250117 107.0 CALL$

Last year's regional bank issues highlighted how ruthlessly the bigger fish can treat the smaller ones in finance. So XLF has been a prime bearish target.

I had mentioned previously that if tech didn't shoulder the broad market pullback, financials could take on some of that burden. And we did see some put buying initially.

But after yesterday's FOMC, a different view seems to have emerged:

Selling the $XLF 20241115 45.0 PUT$ for 40,000 contracts

Why the sudden shift away from outright bearish put buying? What's holding them back from aggressive shorting now?

Simple bullish flow here:

Buying the $XBI 20241220 110.0 CALL$

Not much to add - straightforward upside call buying.

Another bullish trade:

Buying the $KWEB 20241101 26.0 CALL$ for 20,000 contracts

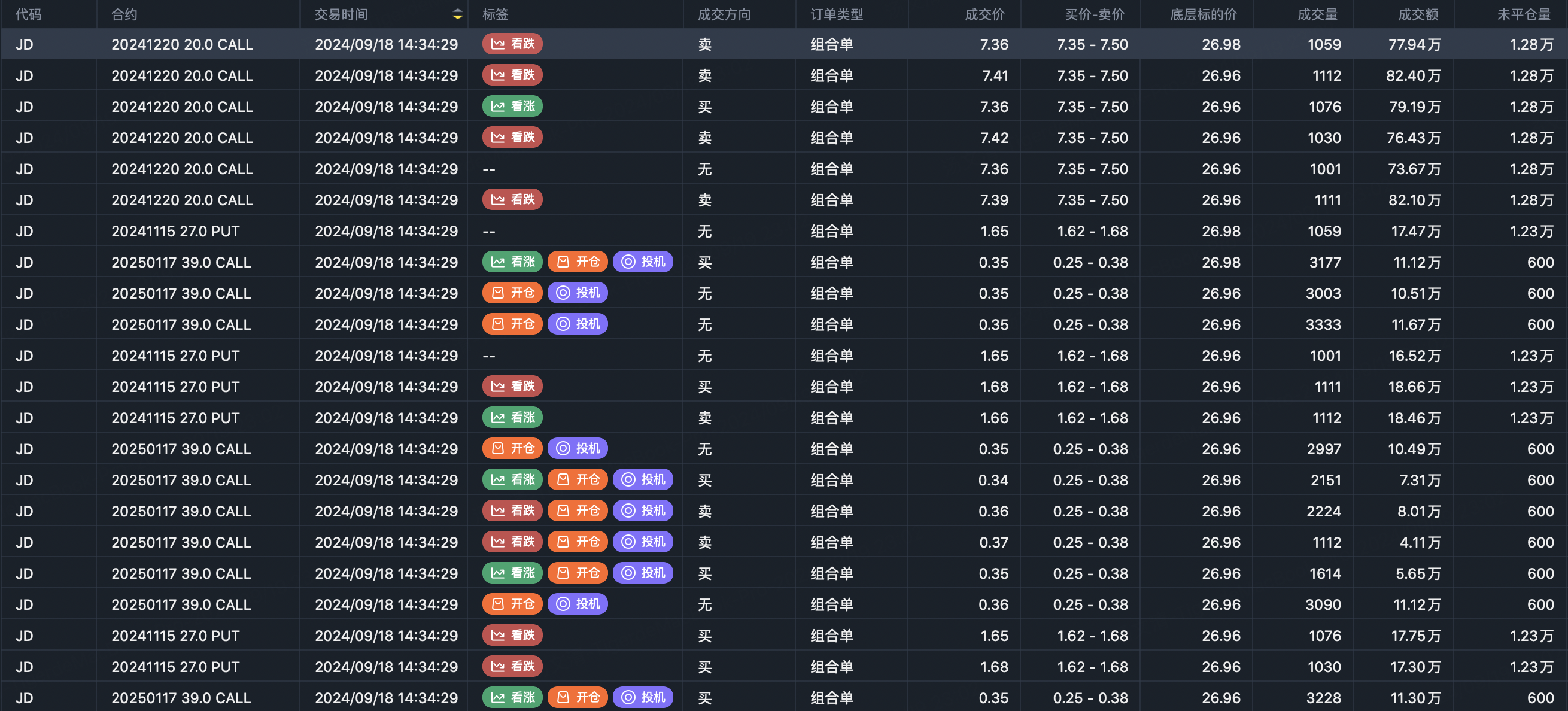

Good news is I have exposure, bad news is my covered calls were called away. But no problem, I'll just sell some new puts to re-establish.

With the China internet ETF bid, it makes sense for single names like JD to rally too. The image shows closing a $27 put and $20 call, while opening a new $JD 20250117 39.0 CALL$ upside position.

Just an endorsement of the broader bullish CNY trend. Selling puts in a liquid mega-cap like Tencent may be a more prudent approach.

Finally, some post-FOMC meeting observations:

The key issue Powell failed to convincingly explain was the specific urgency behind a 50bps hike rather than 25bps. Even when directly questioned by reporters, he didn't provide clarity. Employment remains a key consideration, explicitly re-emphasized in the statement.

But if employment was truly such an acute concern, Powell would have addressed it head-on instead of deflecting. One plausible, if cynical, explanation could be election year politics.

By delivering a more aggressive 50bps "medication" upfront, the Fed could prioritize preserving robust employment ahead of midterms without having to make controversial policy moves closer to the elections. As for inflation rebounding, who's to say they can't just re-hike if needed?

Of course, this rationale is too bureaucratic and contrived to ever be officially stated. But it provides some amusement as a thought experiment.

Nevertheless, it's quite unusual for institutions to avoid any major positioning ahead of such a critical first-hike FOMC meeting. They typically love to market-make around these events and pin any volatility on the Fed.

But this time, at least on the surface, there was very muted activity. Could the upcoming elections also be influencing their trading behavior? Just a thought.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.

- KSR·08:35👍LikeReport