Palantir surge on AI faith

$Palantir Technologies Inc.(PLTR)$ announced yet another upward revision to its annual estimates in its Nov. 4 after-hours earnings report, with shares up more than 12% after hitting an all-time high.The company's shares have risen more than 140% since the beginning of the year.

Palantir's performance has been particularly impressive against the backdrop of a general market rebound, largely due to its continued innovation in artificial intelligence (AI) and strong support from government spending.

Financial performance

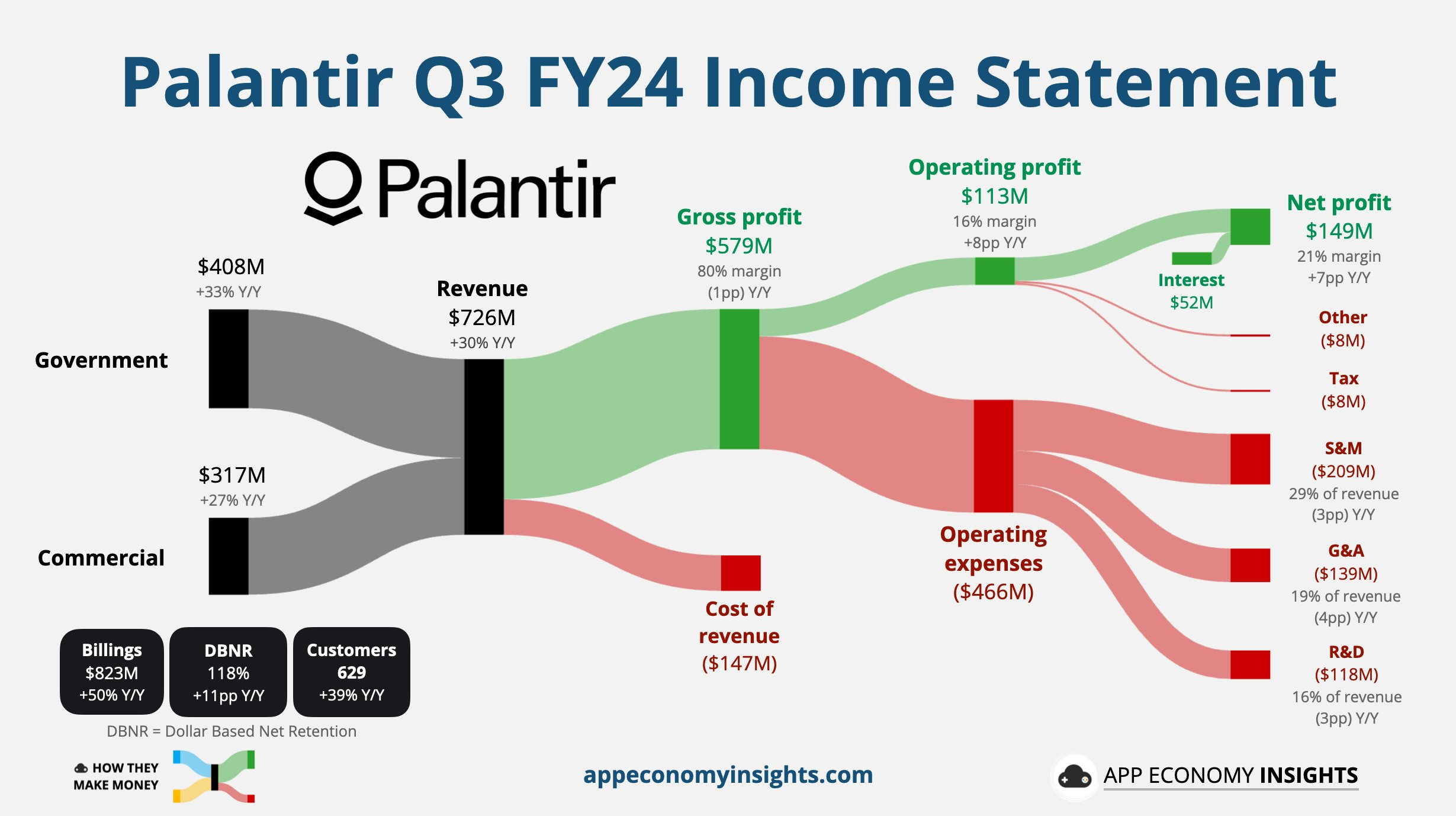

Q3 revenue of $726 million was up 30% year-on-year, beating market expectations of $704 million, with growth continuing to pull up sequentially from the previous quarter.Government revenue continued to rebound with 32.5% year-over-year growth, while commercial revenue grew at a 26% year-over-year rate, mainly dragged down by international markets.

While Palantir is expanding globally, the U.S. market remains its revenue "base," with the U.S. region accounting for 69% of total revenue in the third quarter, and the U.S. government (Department of Defense) accounting for 75% of its total government revenue.

A key highlight of the Q3 results was the 54% growth in its U.S. commercial revenues, marking a shift toward greater private sector engagement, an expansion that suggests Palantir's AI offerings are resonating with U.S. businesses, diversifying its revenue base beyond government contracts.

Additionally, the cost side went through an optimization cycle and is currently re-expanding. gross margin declined in Q3, primarily due to new inputs from AI changes, but overall capex did not rise significantly.

Overheads grew relatively slowly, mainly benefiting from the optimization of personnel costs.Selling and R&D expenses are increasing at a faster pace to support business growth, and future margin improvement is likely to rely more on "open-sourcing" than on "cost-cutting".

Drivers

Palantir's growth was driven by multiple factors:

Government Spending: the company's revenue from the U.S. government, primarily the Department of Defense, grew 40% year-over-year in the third quarter and accounted for 44% of total sales.This indicates that government customers continue to be an important source of revenue for Palantir.

Growth in commercial customers: while Palantir's revenue is still largely dependent on government, its commercial sales business is expected to overtake the government business in the next year.This shift is driven by growing interest in generative AI technologies, with more organizations seeking Palantir's AI platform to test and evaluate AI-related scenarios.

Successful rollout of the AI platform: the AIP platform launched by Palantir has excelled in driving commercial revenue growth.Despite the slowdown in international markets, growth in the U.S. region remained stable at around 54%.

Upgraded Guidance and Future Outlook

Palantir raised its 2024 revenue forecast to $2.805 billion to $2.809 billion, up from $2.742 billion to $2.750 billion previously, with annual growth expected to reach 28%.

In addition, full-year profit expectations have been raised to $1.05 billion to $1.06 billion.CFO David Glazer noted that increased demand for AI is effectively translating into profits.

Looking ahead, Palantir's challenges include how to effectively scale its product offerings globally and how to continue to attract new customers.

The company's management has indicated that going forward, it will focus more on metrics related to new contract additions, such as total contract value (TCV), residual non-cancelable contract amount (RPO) and number of customers, to gauge its medium- and long-term growth potential.

Valuation

Palantir's performance has been smooth sailing, industry scarcity coupled with the company's own competitiveness advantage, investors rarely have systematic worries, so the valuation is higher, 28-32 times the PS is really high among all the growth software companies.

Previously in the SaaS hottest period, $ Snowflake (SNOW)$ also had more than a hundred times the PS, but later were pulled back.So from a valuation perspective, PLTR really isn't very competitive.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.

- frostiix·11-05Incredible growth and insights! 🚀 [WOW]LikeReport

- AuntieAaA·11-05GoodLikeReport