BIG TECH WEEKLY | All Eyes On NVDA Earnings' Surprise?

Big-Tech’s Performance

This week, the U.S. stock market saw-sawed against the "Trump 2.0" era, with digital currency concepts in particular, fluctuating wildly up and down.Technology companies also began to experience a lot of early expectations, including Tesla once surged to $340, once again among the U.S. stock "Top 6", and Nvidia is also hovering in the former high.

At the same time, the U.S. dollar $Invesco DB US Dollar Index Bullish Fund(UUP)$ again extreme strength, non-U.S. currencies fell across the board, but also responded to the rise of risk aversion, the current market on the re-emergence of inflation, the suspension of interest rate cuts, the growing concern.

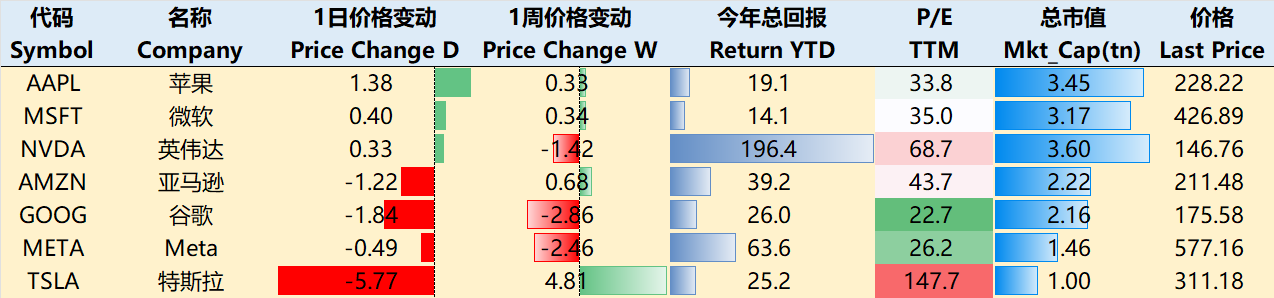

By the close of trading on November 15, the big tech companies were mixed over the past week, with $Apple(AAPL)$ +0.33%, $NVIDIA Corp(NVDA)$ -1.42%, $Microsoft(MSFT)$ +0.34%, $Amazon.com(AMZN)$ +0.68%, $Alphabet(GOOG)$ $Alphabet(GOOGL)$ -2.86%, $Meta Platforms, Inc.(META)$ -2.46%, $Tesla Motors(TSLA)$ +4.81%.

Big-Tech’s Key Strategy

What to do about NVIDIA's overflowing earnings expectations?

November 20 after-hours, the impact of the whole market NVIDIA earnings report will be announced.The biggest highlight of the Q3 earnings report of this 25th fiscal year is how many miracles NVIDIA can still create when it is about to enter the Blackwell era.

In terms of fundamentals

Stabilized market dominance.NVDA's "dominant positioning" in the AI gas pedal market is a key factor in stabilizing its position in the market, as the demand for high-performance computing power is known to be increasing, and the number of GPUs and power consumption required to train a large AI model on a Blackwell GPU has decreased dramatically.Widespread adoption of the Hopper and Blackwell family of products in AI and data center applications will again drive significant revenue growth.

The total addressable market for AI gas pedals is expected to grow by about $70 billion by 2025, and Nvidia will eat the lion's share of this growth, with $Broadcom(AVGO)$ as the only competitor likely to continue to make inroads into the AI gas pedal market, but overall Nvidia still holds a clear advantage. $Advanced Micro Devices(AMD)$ $Intel(INTC)$ There is still a technology generation gap.

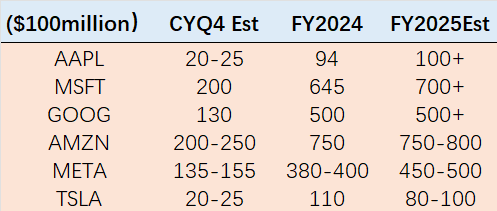

Downstream tech companies' capex trends continue unabated.Microsoft, Google, Amazon and Meta capital expenditures of about $ 54 / 510 / 75 / 40 billion, excluding Amazon inventory centers part of the four combined total of about $ 200 billion.Not only the "Mag 6" capital expenditure, other small and medium-sized cloud vendors have more or less increased the trend remains positive.

Blackwell production is on schedule, and the previous yield difficulties have been overcome.Despite previous design flaws, production is now back to normal and demand is very strong. $Taiwan Semiconductor Manufacturing(TSM)$ a key partner of Nvidia, played a key role in resolving the yield issue.In addition, demand for Hopper continues to grow and has expanded beyond hyperscale customers.

Focus of attention for this earnings report

The magnitude of exceeding expectations.Market expectations for Q3 have been revised upward, with consensus expectations of $33.2 billion and the company guiding for $32.5 billion, and the stock is equivalently priced at $33.2 billion.Of course the market's confidence in beating earnings expectations has always been strong.

Margin Controversy.Expect Q3 gross margins to be down a bit due to yields and somewhat higher costs for the Hopper and Blackwell lines, with market consensus for Q3 gross margins at 75%, next lower than the last few quarterly highs of 78%, and Q4 gross margins likely to fall further to 73%.But gross margins could also recover a bit if and when yields are resolved.Investors may be pondering whether NVIDIA has reached peak margins and growth rates.

High valuations vs. high expectations.At the stock level, current valuations already factor in expectations of around 30x in 2026, but the problem is that 2025 could be a turnaround year, dictated by the current investor cycle for tech companies.And it's not uncommon for the current market to have high expectations for NVIDIA's continued high growth, making it more difficult for the company to surprise investors when it reports earnings.

Big-Tech Weekly Options Watcher

This week we are watching:

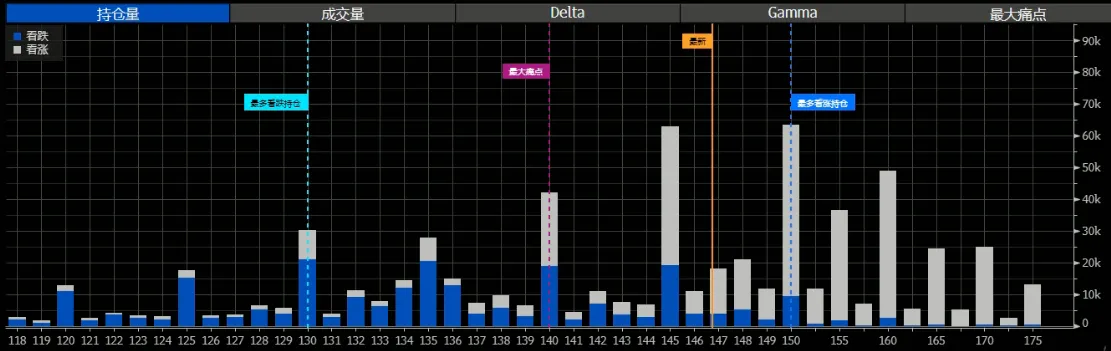

NVDA: Next week's earnings report, this week, although in a new high position, but a sharp contraction, and very little volatility, obviously waiting for earnings information, and further give the direction of the upside / downside.From the options state of view, the focus of 150 for, as well as 160 have the largest number of Call orders ambush, on the contrary, 170 above is not too much of a game of single, from the former dissimilar Call large orders concentrated in the forward (December and next year) above 180, you can see that the market is still willing to take the time to verify.

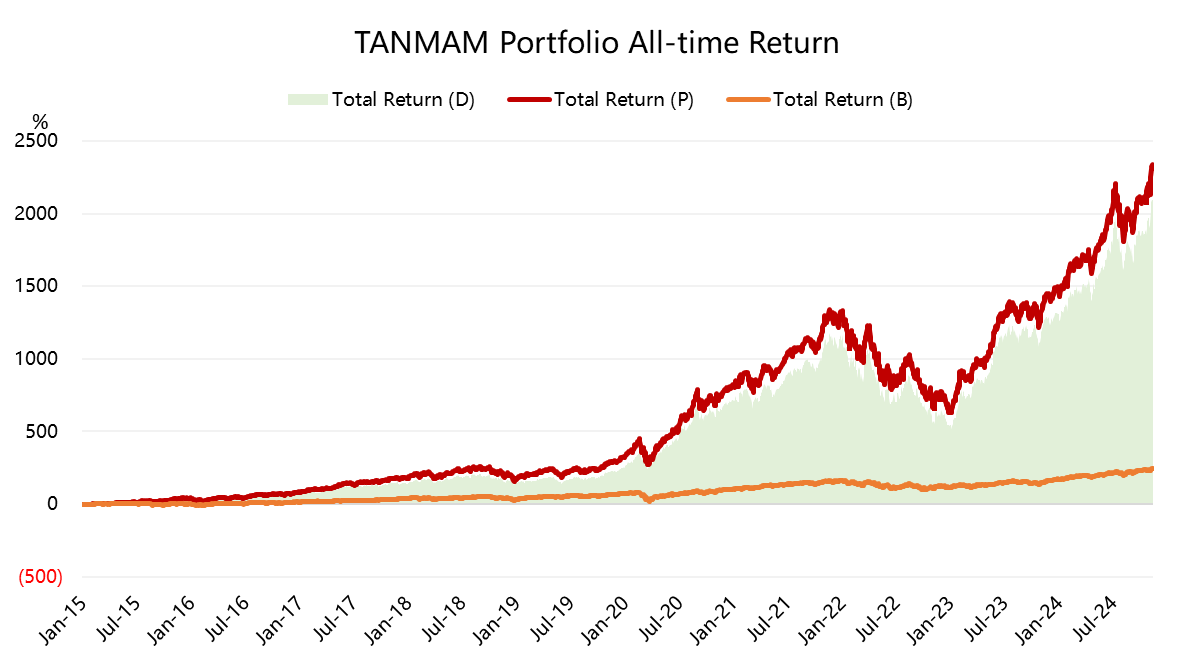

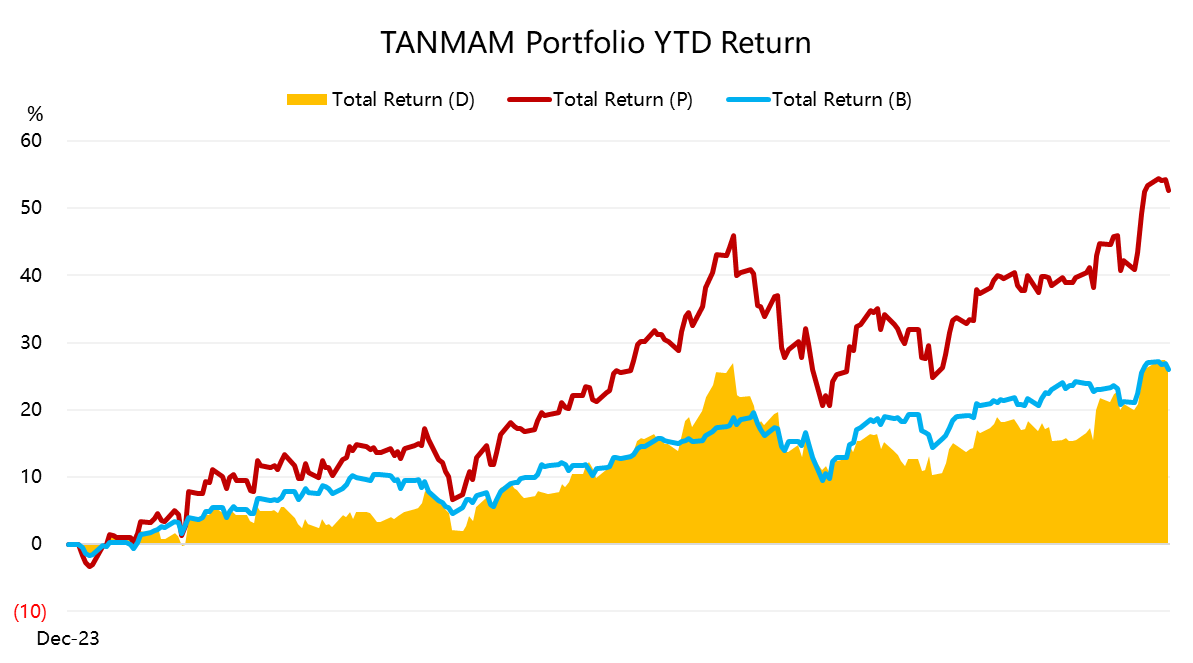

Give a reason to hold positions in large technology stocks - why "TANMAMG" portfolio always outperform the market?

The Magnificent Seven form a portfolio (the "TANMAMG" portfolio) that is equally weighted and reweighted quarterly.The backtest results are far outperforming $.SPX(.SPX)$ since 2015, with a total return of 2,315.03%, while $SPDR S&P 500 ETF Trust(SPY)$ has returned 242.77% over the same time period, once again pulling ahead with an excess return of2702.26%.

The portfolio's Sharpe Ratio over the past year has rallied to 2.9, the SPY is 2.75, and the portfolio's Information Ratio is 1.52.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.

- skippix·2024-11-15The mixed performance is concerning, but the long-term outlook for big tech remains strong.LikeReport